While economists fret about rising inflation, investors have shrugged off recent CPI readings, driving the S&P 500 Index to a new high.

Inflation has surprised Fed officials. Action in the bond market, however, suggests investors believe that relaxed restrictions and pent-up demand are the primary reasons behind the elevated CPI numbers, and the Fed’s transitory inflation theme is the most likely outcome.

With the June meeting at the top of the calendar, investors don’t expect the Fed to blink in the face of recent inflation readings. It leaves stocks priced for a rosy scenario.

1. Inflation continues to outpace expectations

- Economists have struggled to forecast monthly data over the last year.

- Few expected the sharp acceleration in the economy.

- Few expected inflation to surge over the last two months.

| Table 1: Inflation Quickly Heats Up |

| |

Monthly change |

Analyst forecasts |

| CPI May |

0.6% |

0.4% |

| Core CPI May |

0.7% |

0.4% |

| CPI April |

0.8% |

0.2% |

| Core CPI April |

0.9% |

0.3% |

Source: U.S. BLS, IBD

- At the wholesale level, inflation has been worse, averaging 0.8% per month over the last five months.

- In 2019, the average monthly change in the Producer Price Index was 0.1%.

- Past inflation scares have proved to be temporary, but recent increases far outpace prior upticks.

- April and May’s monthly readings in the core CPI were the highest in nearly 40 years.

- Some increases were headline grabbing. For example:

- Auto rental rose 12.1% in May following a 16.2% rise in April

- Airline fares increased 7% after a 10.2% rise in April

- Used cars rose 7.3%, which was on top of a 10.0% increase

- Furniture jumped 2.1%

- New cars surged 1.6%

- Apparel rose 1.2%

- While notable, these categories account for just 10.1% of the CPI per the U.S. BLS.

- Services, which account for 62% of the CPI, rose a more moderate 0.4%. The category has recently firmed.

- Shelter (33% of the CPI), a subcomponent of services, rose 0.3%.

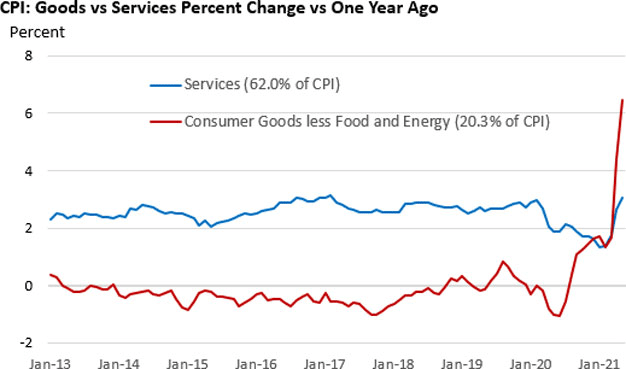

- Figure 1 highlights the recent jump in consumer goods, which had been in a deflationary trend over the last decade.

Figure 1: Pinpointing Inflation

Source: St. Louis Federal Reserve May 2021

- Spending has rebounded, and supply constraints are pushing up prices in some industries.

- Rental car prices are up 110% versus a year ago.

- As Table 2 illustrates, air fares, hotels, and apparel are playing catch-up. Supply constraints are having a much greater impact on autos.

| Table 2: Headline-Grabbing CPI Categories |

| Year |

Jan 2020 peak to trough change in price |

Jan 2020 to May 2021 change |

| Air fares |

-28.6% |

-11.6% |

| Hotels |

-10.8% |

-3.0% |

| Apparel |

-7.2% |

-2.1% |

| New cars and trucks |

-0.1% |

3.5% |

| Used cars and trucks |

-0.3% |

29.4% |

Source: U.S. BLS

Powell’s thinking

- The economy achieved full employment in the last cycle without generating inflation. Moreover, the Fed failed to attain its two percent inflation target.

- Low rates and QE earlier in the decade failed to create destabilizing bubbles.

- Wage hikes were absorbed through margins and productivity gains rather than price hikes.

- Commodity inflation was not a problem.

- Therefore, the Fed believes it has the freedom to pursue a super easy policy, as it tries to quickly coax the economy back to full employment.

- However, today’s recovery is unlike anything we’ve seen before and far different from the last cycle.

- Massive fiscal stimulus, coupled with reopenings and relaxed distancing restrictions, has spurred huge gains in spending that are running up against production constraints.

- Powell is gambling recent increases are temporary and tied to the reopenings.

- The risk: The Fed falls behind the curve as a new cycle of inflation gets underway, forcing the Fed to raise rates sharply, which ends in a hard landing, i.e., a recession.

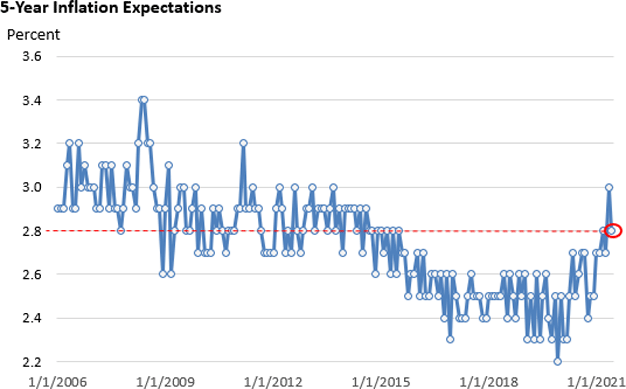

2. Market and survey-based inflation expectations

- After closing at 1.74% on March 19 and March 31, the yield on the 10-year Treasury eased to 1.45% as of June 11.

- Expectations the Fed won’t start tapping the brakes and the belief the spike in inflation is transitory are leading to relative tranquility in the Treasury bond market.

- After hitting a triple-peak of 2.54% in May, the 10-year break-even inflation rate (what investors are willing to give up for inflation protection in 10-year Treasury bonds via TIPs), eased to 2.32% as of June 11.

- It also suggests the inflationary surge is transitory.

- The University of Michigan consumer sentiment survey includes a review of inflation expectations.

- The one-year outlook: down from May’s 10-year high of 4.6% to 4.0% at the mid-June reading.

- The Fed follows the five-year outlook more closely. It is down from May’s reading of 3.0% to 2.8%, signaling inflation expectations are well anchored.

Figure 2: Still Behaving

Source: University of Michigan June 2021

- Gold is considered by some to be an inflation hedge. After briefly peaking above $2,000 per ounce last year, gold is hovering near $1,900 today.

- While gold is influenced by several variables, if you watch gold for inflation signals, price action is not suggesting a more permanent rise in prices.

3. Past cycles and today

- Going back to the Volcker days of the 1980s, the Fed has launched pre-emptive strikes on inflation by hiking interest rates.

- Before inflation hit 2%, the Powell Fed raised rates during the last cycle.

- It’s a new world today: no more pre-emptive strikes.

- The Fed insists it won’t raise interest rates until the economy reaches:

- Maximum employment, and

- inflation has reached 2%, and

- inflation is expected to remain above 2% for some time.

- It’s a high hurdle for raising rates.

- It suggests inflation alone isn’t enough to raise rates if the economy isn’t back to full employment.

- It suggests the Fed is confident inflation won’t become a problem.

- Tapering $80 billion in monthly Treasury bond buys and $40 billion in mortgage-backed security buys:

- The Fed wants to see that “substantial further progress has been made” toward its maximum employment and its price stability goals.

- The economy has recovered 14.7 million of the 22.4 million jobs lost in the pandemic per nonfarm payroll data. This includes 559k jobs in May.

- Though economic growth has been very strong, the Fed’s own commentary suggests more improvement is needed.

Bottom line

- The Powell Fed is doing everything in its power to get the economy back to full employment and is willing to tolerate some inflation.

- Despite today’s fast growth rate, labor shortages, and the inability of some businesses to meet demand, the Fed continues to purchase massive amounts of bonds.

- A robust argument can be made for the transitory case and the more worrisome case.

- Are hefty bond buys still needed against the backdrop of strong economic growth?

- Might the Fed blink and shift its stance?

- An abrupt tapering would likely bring about volatility in fixed income assets and stocks, but the Fed has said tapering will be well telegraphed.

- In June 2013, the S&P 500 shed 5% in four days following former Fed Chief Bernanke’s taper roadmap.

- It was a very brief dip in stock prices.

- After the S&P 500 bottomed in late June at 1,573, the index doubled before the bull market ended in 2020.

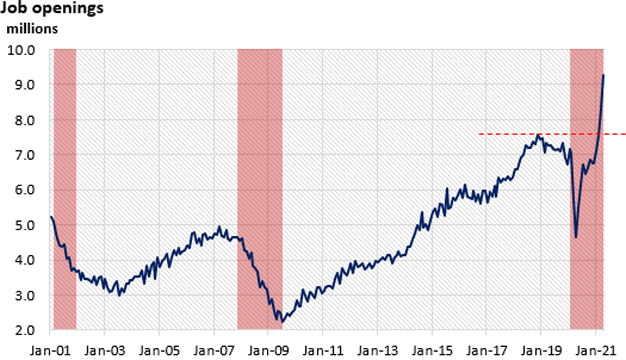

4. Job openings soar

- Since December 2020, job openings have surged 38% to a record 9.3 million as of April—see Figure 3.

Figure 3: We’re Hiring

Source: U.S. BLS, NBER: Shaded areas mark recessions April 2021

- The NFIB said, “A record-high 48% of small business owners in May reported unfilled job openings.”

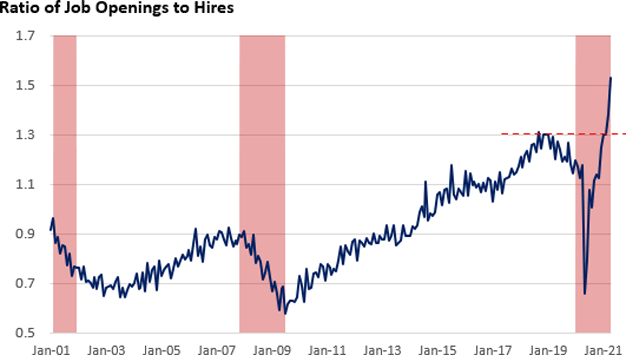

- Openings have far outstripped the pace of hiring—see Figure 4.

Figure 4: Employers Get Squeezed

Source: U.S. BLS, NBER: Shaded areas mark recessions April 2021

- Economists cite a wide variety of reasons, from generous jobless benefits to early retirements.

- Notably, the labor force participation rate for those 55 and older, which rose during the Great Recession, has failed to bounce off the bottom.

- That’s not the case with the 25–54 year-old crowd (though the level remains below the pre-pandemic peak).

- The hard-hit leisure & hospitality (L&H) sector is now having trouble filling open positions.

- A record 17.1% of openings are in L&H as of April per the U.S. BLS.

- That’s up from 10.4% in January.

- 20-year average: 12.6%

- Economists fret that labor shortages threaten to slow the recovery and lift inflation, as higher wages get tacked on to retail prices.

- It’s unclear when shortages may ease.

5. A peek ahead

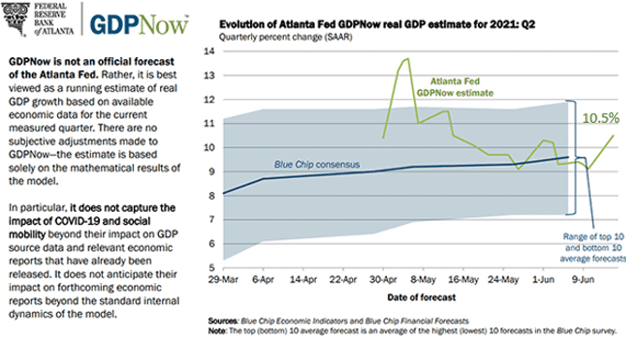

I. Q2 GDP tracking above 10%

- As social distancing restrictions are eased and fear of Covid wanes, Q2 is shaping up to be a blockbuster quarter.

- The less volatile Blue Chip consensus is in an upward trend.

Figure 5: A Blowout Quarter

Source: As of 6/15/2021; the model incorporates data as released. June data are not yet available.

- Q2 GDP will be released near the end of July.