Editor’s note: In an earlier article we examined the “winners” in the One Big Beautiful Bill.

Signed into law on July 4, the One Big Beautiful Bill Act (OBBBA) enacts sweeping tax cuts and entitlement reforms with far-reaching consequences. While some Americans gain significant tax advantages, others are set to bear the cost of the legislation’s $4–$6 trillion price tag.

From cuts to public health funding and student loan aid to tighter eligibility for social benefits, here’s a look at the key groups on the losing side of the OBBBA.

1. Americans relying on social safety nets may receive less benefits

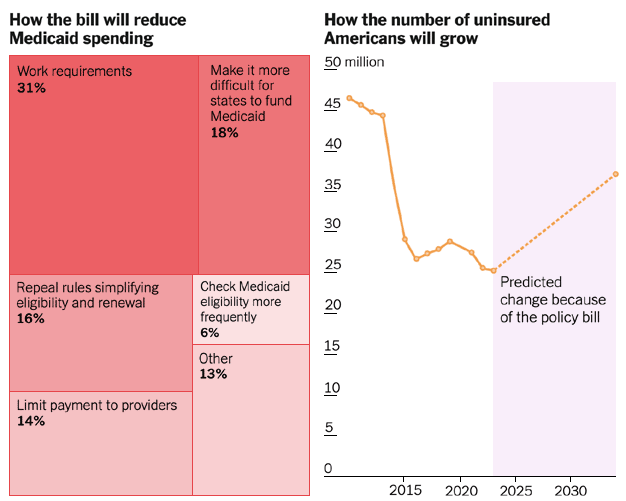

The OBBBA tightens eligibility and imposes new verification rules for Medicaid and SNAP (food stamps), while shifting more administrative costs onto states. States also face new restrictions on how they raise their share of Medicaid funding, potentially reducing services. As a result, millions are expected to lose coverage. The Congressional Budget Office (CBO) projects nearly 12 million more uninsured Americans by 2034. An earlier CBO estimate put the number at 16 million.

The new verification requirements include pre-enrollment verification of income, immigration status, health coverage, residence, and family size before coverage begins, with states required to repeat eligibility checks monthly for some enrollees and every six months for Medicaid expansion adults starting in 2026. Additionally, the Act imposes work requirements mandating that able-bodied adults prove they work, engage in community service, or receive training for at least 80 hours per month to maintain Medicaid eligibility.

The Act also ends an Affordable Care Act (ACA) tax credit boost, making health insurance more expensive for many low-income Americans. Medicaid is also the country’s biggest payer for long-term care including nursing homes, according to the AARP. Tighter funding may have implications on nursing home access and staffing levels. Though the administration argues the changes target “waste, fraud, and abuse,” they’re likely to cut access for vulnerable populations, including older adults reliant on Medicaid-funded long-term care.

This graph from The New York Times shows the projected increase in the number of uninsured Americans due to the One Big Beautiful Bill Act, with 12 million people expected to lose coverage by 2034, reversing years of progress since the ACA.

Figure 1: Millions Lose Access to Medicaid

Sources: Sources: KFF; C.B.O.

Note: Minor changes at the end of the Senate process may result in a slightly smaller increase in uninsured. Projections do not include other potential changes in the number of uninsured.

2. Deficit hawks are unhappy, along with borrowers

The Act raises the federal debt ceiling by $5 trillion and is projected to add between $4–$6 trillion to the deficit over the next decade, coming at a time when national debt exceeds $36 trillion. Bond markets have taken notice: Growing deficits may raise Treasury yields, which in turn can increase interest rates on mortgages, auto loans, and other forms of consumer debt.

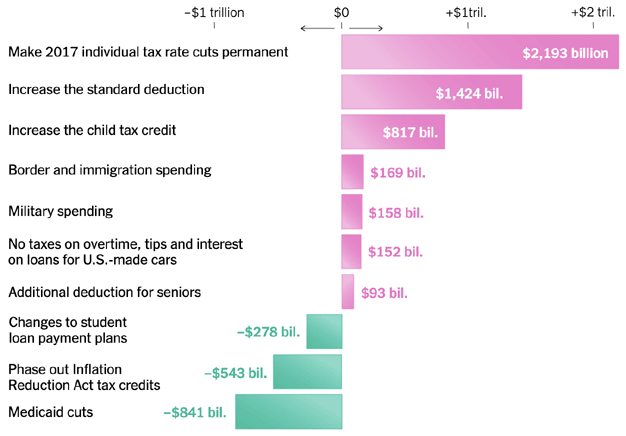

The largest deficit driver is making the 2017 individual tax rate cuts permanent, adding $2.193 trillion over 10 years, followed by increasing the standard deduction ($1.424 trillion) and expanding the child tax credit ($817 billion). Additional spending includes $169 billion for border and immigration enforcement and $158 billion for military spending.

These deficit increases are partially offset by spending reductions totaling $1.662 trillion over the decade. Medicaid cuts generate the largest savings at $841 billion, while phasing out Inflation Reduction Act tax credits saves $543 billion and changes to student loan payment plans reduce costs by $278 billion. Despite these offsets, the net fiscal impact represents a massive increase in federal borrowing.

At $3.0 trillion in new costs as written (potentially rising to $3.7 trillion if provisions are made permanent), the One Big Beautiful Bill Act represents the largest domestic policy expenditure in recent history, dwarfing the American Rescue Plan Act’s $1.8 trillion price tag and the 2017 Tax Cuts and Jobs Act’s $1.5 trillion cost.

This chart from the NYT illustrates how major provisions in the One Big Beautiful Bill Act will impact the federal deficit over 10 years, with the extension of the 2017 tax cuts contributing the largest increase and Medicaid cuts generating the largest savings.

Figure 2: Impact on the Deficit Over 10 years

Sources: The Washington Post; Joint Committee on Taxation; C.B.O.

3. Electric vehicle buyers and clean energy are dealt a setback

The OBBB Act deals a significant setback to electric vehicle (EV) buyers and the broader clean energy transition. It abruptly ends the $7,500 credit for new EVs and the $4,000 credit for used ones after September 30, 2025, impacting both consumers and automakers amid already sluggish EV adoption. Additionally, tax credits for solar panels, wind projects, and home EV chargers are being repealed or sharply curtailed, with deadlines ranging from December 2025 to June 2026. These changes affect homeowners, drivers, and developers who were previously incentivized to make energy-efficient upgrades.

By scaling back many of the clean energy tax incentives introduced in the Inflation Reduction Act, the legislation shifts the U.S. policy focus away from renewables and toward fossil fuels. Credits for clean vehicle purchases (IRC Sections 30D and 25E), home EV chargers (IRC Section 30C), and residential energy improvements (IRC Sections 25C and 25D) are all ending within the next 18 months.

Without these federal supports, individuals and businesses may find clean energy investments less affordable or attractive, potentially weakening domestic production and undermining progress on emissions reduction.

4. Student loan borrowers may pay more and lose flexibility

The OBBBA overhauls the student loan system by capping how much graduate students and parents can borrow, reducing access for part-time students, and eliminating many repayment and forgiveness options introduced in recent years. Deferment and forbearance will be harder to obtain, and repayment will be simplified into two stricter plans.

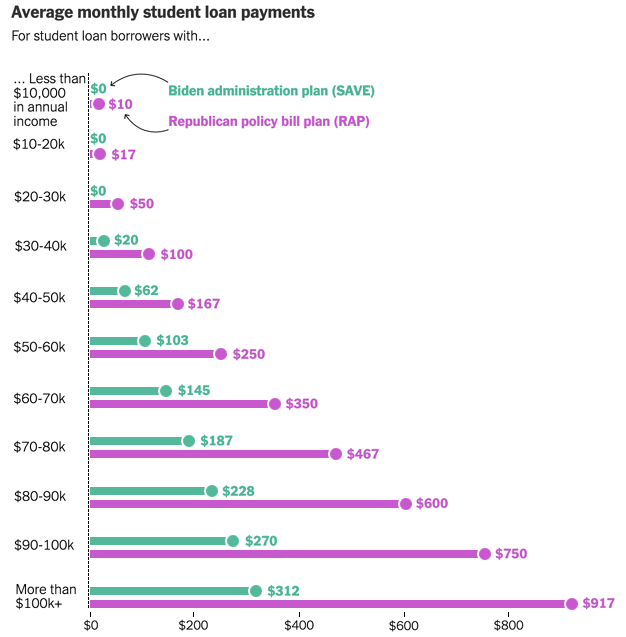

The Act eliminates most existing income-driven repayment (IDR) plans and caps new borrowing after July 2026 at $100,000 for graduate programs and $200,000 for professional degrees. Parent PLUS and graduate borrowers will no longer have access to multiple repayment and forgiveness options introduced in recent years. Borrowers who take out loans after July 2026 will primarily be placed into a new Repayment Assistance Plan (RAP), which requires payments of 10% of discretionary income for up to 30 years, longer than the current New Income-Based Repayment (IBR) 20- or 25-year term.

For borrowers currently on plans like Pay As You Earn (PAYE) or IBR, those plans will remain for now, but all new borrowers will be funneled into RAP or the standard 10-year plan. While the Act does make permanent a tax break for employers who contribute up to $5,250 annually toward loan repayment, many borrowers will face fewer protections and higher burdens.

This graphic from The New York Times shows how monthly student loan payments will rise under the Republican policy plan compared to the Biden administration’s SAVE plan, with middle- and high-income borrowers facing the largest increases in repayment amounts.

Figure 3: The Cost of College Will Soar

Source: Student Borrower Protection Center

5. Immigrants may no longer qualify for assistance

The law narrows eligibility for public programs—including SNAP, Medicaid, and ACA subsidies—for many noncitizens. Previously protected groups such as refugees, asylees, and victims of trafficking may no longer qualify for assistance. The bill also raises fees for immigration-related applications, including asylum, work permits, and court filings, creating more financial hurdles for those seeking legal status.

6. Private universities with large endowments will lose

Top-tier private universities are facing a steep tax hike. The OBBBA increases the excise tax on endowment income from a flat 1.4% to a progressive structure topping out at 8% for schools with more than $2 million per student. The biggest losers are expected to be Harvard, Yale, Princeton, Stanford and the Massachusetts Institute of Technology, which are expected to pay 8%, potentially impacting research funding and student financial aid.

Smaller institutions with fewer than 3,000 tuition-paying students are exempt from the hike. Overall, this significantly shrinks the number of schools paying an endowment tax.

7. Hospitals dependent on Medicaid matching funds will be hit

In many states, hospitals are taxed to unlock additional federal Medicaid funds, a system that benefits both the state and the hospitals themselves. The Act limits states’ ability to increase Medicaid payments to hospitals by restricting how they can use provider taxes.

The new law limits this practice by reducing the maximum allowable provider tax rate from 6% to 3.5% in states that expanded Medicaid under the ACA. Non-expansion states are locked into current levels. Health care leaders warn that this change could reduce hospital revenues and impact staffing or service delivery, especially in rural or low-income areas.

In conclusion…

The One Big Beautiful Bill Act may deliver long-term tax relief for some, but it also imposes significant costs on others, particularly low-income families, immigrants, students, clean energy consumers, and institutions that rely heavily on federal funding.

With major cuts to safety net programs, student loan reforms that raise repayment burdens, and rollbacks on clean energy incentives, the Act shifts the balance of government support in ways that could widen economic disparities and limit opportunity for many Americans.

As the national debt climbs and key public programs face stricter funding constraints, these changes may have lasting ripple effects on affordability, access, and economic mobility. Financial advisors and policy observers alike must pay close attention to how these provisions play out, particularly as temporary elements expire and economic conditions evolve.

Sources

- MarketWatch. “Tax Breaks and Spending Cuts: Here Are the Winners and Losers in Trump’s Big Bill.” July 4, 2025.

- USA TODAY. “The Winners (and Losers) in Trump’s ‘Big Beautiful’ Tax Bill—Now Law.” July 3, 2025.

- The Wall Street Journal. “Hospitals May See Medicaid Payments Shrink Under GOP Tax Plan.” July 4, 2025.

- NBC News. “Legislative Impact Summary: What the GOP Tax Overhaul Means.” June 30, 2025.

- Forbes. “Estate Planning and the Final OBBBA: Key Changes High-Net-Worth Individuals Must Know.” July 3, 2025.

- The Wall Street Journal. “Fossil Fuels and the Energy Sector: Quiet Winners in Trump’s Tax Law.” July 4, 2025.

- Tax Foundation. “One Big Beautiful Bill Act Tax Policies: Details and Analysis.” July 3, 2025.

- KFF. “Potential Impacts of Medicaid Changes in the OBBBA.” July 2025.

- AARP. “Medicaid’s Role in Long-Term Care and the Effects of New Federal Reforms.” July 2025.

- The New York Times. “Opinion: What’s in the Domestic Policy Bill? These 12 Charts Explain.” July 3, 2025.

- LPL Financial. “Bond Market Braces for Long-Term Impact of OBBBA.” July 2025.

- American Council on Education. “Endowment Tax Hike Could Harm Students, Research.” July 2025.

- Student Loan Planner. “Top 10 Changes for Student Loan Borrowers Under the One Big Beautiful Bill Act.” July 7, 2025.