“My, how times have changed!” This phrase has no doubt been proclaimed endless times throughout the history of civilization. The fact is, times never stop changing. Our world is constantly evolving—and with it, so is our industry.

In the past several years, it has become apparent that today’s clients are offered more choice and more opportunity than ever before in deciding how they want their wealth managed. And the profession needs to adjust accordingly by offering more flexible fee options that are better aligned with the value of the services offered.

We are just starting to deal with the realization that the traditional asset-based fee model that our industry has been accustomed to for so many years may not work as well anymore, particularly for prospects. In short, clients need choice and we need to be more flexible in how we charge them.

Charging clients in only one way—simply based on assets under management (AUM)—may limit the growth of your wealth management firm. With an AUM fee structure, you may be turning away clients who may never come back. But a flexible fee structure allows you to bring on younger clients, or clients who need services and don’t have the assets just yet (think a young doctor or entrepreneur), but someday will.

Maybe you disagree, but a recently released research report by the global consulting firm of Simon-Kucher & Partners may convince you otherwise. The 71-page report speaks loud and clear, and at Taylor Financial, we’re listening! In fact, although we had already started including alternative fee arrangements for our clients on our website, once we read this report, we immediately updated our website’s fees and services page to include many more financial planning and fee options than ever before. We suggest you consider doing the same, or you might get left behind.

Transparent fees are important

Too many financial advisor websites have zero to little information about the fees they charge. We were guilty of this, too, until earlier this year. But this bothered me even before I had come across the Simon-Kucher report.

One day, almost a year ago, while I was researching contractors on the Internet, I became more and more frustrated. Why? I couldn’t find any explanation of fees or services. Nothing. And I thought to myself, how irritating and annoying! What are they trying to hide?

Then it dawned on me that my very own website was just as bad. But what was worse, in my opinion, was the fact that I’m a financial advisor who prides herself on transparency. There is no good reason why someone who is considering hiring me shouldn’t have a clear understanding of what and how they will be paying me. After all, what am I afraid of?

You’re probably wondering why it took me another 10 months to do something about it. The short answer is that I wasn’t sure how to approach it all. It felt difficult to create a fee structure beyond the typical AUM-based structure. Frankly, I hadn’t really charged any other way, except a few times under unique circumstances.

So, I wasn’t even sure what I was supposed to charge for financial planning if it wasn’t tied to a percentage of AUM. And there wasn’t much talk of fee options in the industry yet, at least not to the extent that there was a clear-cut way of breaking it down. I basically brainstormed with my team for months, often we thought we had it figured out only to realize our plan may cause issues with compliance or otherwise.

And, even when we initially took the plunge a few months ago and listed some basic financial planning fees on our website, we quickly realized we were severely undercharging. It was a struggle to figure it all out, to say the least. That’s why I was so grateful when I came across Simon-Kutcher’s report. It brought a sense of clarity and a clear structure around an otherwise complicated and uncharted territory.

Comprehensive explanations are necessary, too

Although we have our fees clearly laid out, we didn’t want to leave prospects and clients wondering and speculating about what they were getting or which options they should choose. We knew we had to explain how the fees aligned with the services. So, we took the time to build out our fees page in great detail, so that visitors may completely understand the services they get and where their money will go.

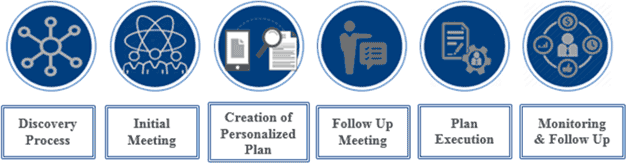

For instance, we explain what the initial one-hour consultation fee of $250 covers. We also explain our Six-Step Process (see Figure 1) for creating a financial plan, so prospects know what to expect from the moment we begin gathering information through the monitoring and maintenance of their plan.

Figure 1: Taylor Financial Group Six-Step Process

Source: Taylor Financial Group

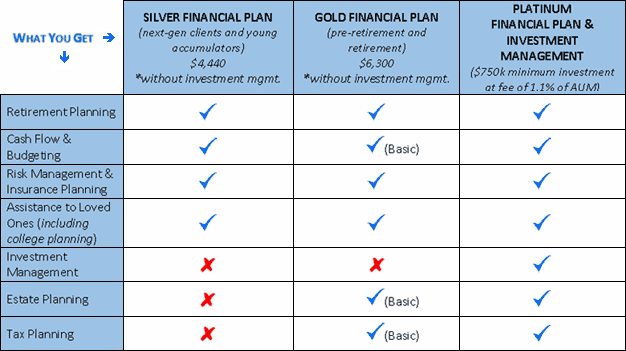

But we don’t stop there! We also created a comprehensive menu of services to make it easy for prospects and clients to see what they get with each of our financial planning packages. As you can see in Figure 2, the menu chart is so easy to follow, it leaves very little room for questions or confusion.

Figure 2: Taylor Financial Group Financial Planning Packages

Source: Taylor Financial Group

Honestly, we know that our work isn’t done in this area. We may end up rethinking and revising our options several times over before we find the place we’re comfortable with and that we know our clients are happy with. But we’re OK with that.

We are prepared to do whatever it takes to give people what they’re looking for in a financial advisor, because that’s what it’s all about. Our goal as financial advisors and fiduciaries should always be to do what’s best for the client, and that includes finding ways to meet their needs and help them pursue their goals in a way that works for their lifestyle and their pocket. It’s not about what works for us—it never should’ve been.

So, I encourage you to take a really good and honest look at the way you’re charging your clients and consider what you can do to offer more options. Stay tuned for an upcoming article, where we will discuss our thinking behind the new services we offer and how they can cater to all types of clients and situations. And, remember, in the end, you’re still opening the door to new business and new revenue for your firm—probably more than before. Even more important, you’re securing your place in this changing industry.