In a recent article, we talked about the importance of being more flexible with how we charge clients and being transparent by posting our fees on our website. We have come to realize that offering additional services beyond investment management and providing additional fee options will create a vital opportunity for growth, and we anticipate that the significance of fees will only grow greater. Charging clients according to the “old-fashioned” asset-based model just isn’t working as well as it once did. Why? Because fees based solely on a percentage of assets under management (AUM) assume that everyone is a high-net-worth delegator when they walk in the door. Meanwhile, it neglects so many other investor types.

What about the do-it-yourselfer who doesn’t want to give you all of his assets but needs a financial plan, or the young doctor who is still building assets but has big potential for future wealth, or the hardworking married couple nearing retirement who has hardly any assets but has 401(k) accounts with almost $1 million invested? We have had each of these prospects come to us in the last month and yet, in the old days, we would have turned them away as they would have been considered unprofitable and a bad fit for our model.

As financial advisors who have traditionally catered to high-net-worth clients, we would’ve discounted these smaller-asset investors because we were only charging fees based on AUM. We just didn’t see the value in spending significant time servicing clients whose AUM would not produce meaningful income for the firm.

Now we realize that we need to change the way we do business. If we offer a diverse set of services that cater to all types of investors’ needs, then we can also charge fees that align with those services, giving clients the option to pay only for what they need, and allowing us to get paid based on the work we do. Our thinking has evolved and we’re sharing our thoughts with you.

Initial consultation and hourly fees

Years ago, most of our prospects came from client referrals. As a result, we didn’t typically charge a consultation fee for prospect meetings. In our experience, almost all referrals became clients, so our initial meetings were completely complimentary and we didn’t give it a second thought.

However, for the past year or so, we have been working much harder for our prospects, as most of them are coming from our workshops or advertisements. This means that, to some extent, proving ourselves is a much bigger task because we don’t have the weight of a recommendation from a current client to help us. In short, we are no longer dealing with warm prospects these days.

After a while, it became clear that we could not continue giving away initial consultations, especially considering the time and effort that goes into preparing for those meetings. Now, we charge $250 as an initial consultation fee, but we let prospects know that if they become clients, that $250 gets rolled into their overall fee, making their initial consultation complimentary after all.

We have also added an hourly fee option that we call the “pay-as-you-go” option, which allows clients to pay for additional planning matters and professional support, without being obligated to any other service. This works well in instances when a new prospect just wants some advice or assistance with a specific matter. This also works well for someone who doesn’t meet the $750,000 minimum. For clients who meet our minimum of $750,000 in investable assets, all additional planning services are complimentary, so the hourly fee doesn’t really affect them.

But, for clients who are not interested in investment management, our hourly rates give us the ability to help them with more complex planning matters (such as divorce support, college planning, stock option planning, and pension analysis), as well as with advanced tax and estate planning. We are also often called upon to meet and work with our clients’ other advisors (CPAs, attorneys, etc.) to provide analysis or discuss best options for a specific situation. For example, we just took on a client who is getting divorced and all of her assets are tied up in company plans. Although she doesn’t have investable assets yet, we have billed over $5,000 in consulting services and we are making a difference in her life.

While our regular hourly fee varies from $280 per hour (for support staff) to $400 per hour (for our principal—that’s me—and our chief operating officer), we also offer clients the option to pay in advance for future hours at a blended rate of $300 per hour. This is a great way to give clients an incentive to purchase hourly packages while securing extra income for your firm.

Financial planning packages

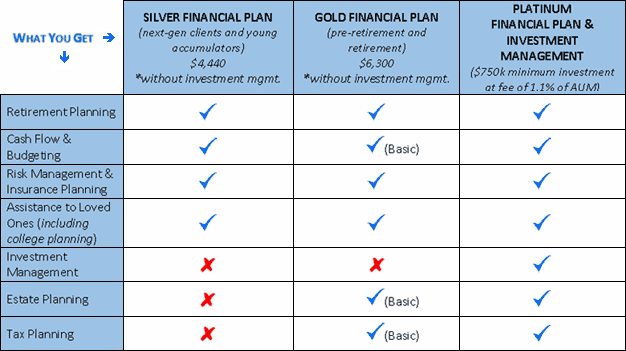

One of the biggest changes we’ve made to our services and fees has been the addition of a service menu that lays out our three new financial planning packages. Each of the packages is aligned with the different services outlined on our Financial Future Planning Chart.

The Silver Package is our most basic financial planning package, targeting the younger investors who are still in the accumulation phase of their life. They could be in their 20s, 30s or 40s, and at various stages in their career, but they are looking to pay down debt and/or start saving and planning for the future. This package provides retirement planning, basic cash flow and budgeting, risk management and insurance planning, and assistance to loved ones. While it does not include investment management, it’s a great option for those who want a plan, but don’t need or can’t yet afford the extra stuff.

The Gold Package is our mid-grade package that includes everything in the Silver Package, but offers additional planning too, like estate and tax planning, albeit at a basic level. This package targets those who are approaching retirement or are already in retirement. They are typically somewhere in their 50s or 60s, and they have some complex matters to consider, like multiple sources of compensation, stock options, pension options, and so forth. They would likely be seeking extensive advice on estate and tax planning to help them avoid the potential for future penalties or other issues. This package doesn’t include investment management either, but it works well for those who have money tied up in other places that could someday become investable assets.

The Platinum Package is fully loaded with all the bells and whistles, including investment management! For that reason, it’s the only package that is charged based on AUM, and it makes sense to do so. This package aims to meet the needs of high-complexity planning clients. As they say, “more money, more problems!” With this package, clients can have peace of mind knowing that all of their goals and concerns are being addressed, and they don’t have to worry about paying any additional fees for additional services. It’s all inclusive, which is what these clients need, and they love it!

Taylor Financial Group Financial Planning Packages

Source: Taylor Financial Group

We realize that this new proposed fee structure may not make sense for existing clients, which is why we are already undergoing an analysis on where and how the fees and options could make sense for existing clients going forward. Nonetheless, we are excited that we’ve come to a place where we can feel confident about the services we offer and the fees we charge for all kinds of people with all kinds of needs.

Adapting for a robust future

We know it may feel overwhelming to build out a new fee structure for your firm, but consider the benefits. By offering a variety of service options and fees, you will help build relationships with clients you might have shut the door on in the past. These clients may not bring you a ton of income now, but the investment you’re making in the new relationships could pay off big in the future.

The hardworking married couple who has grown to trust you will finally retire and could decide to roll over their 401(k) accounts into a portfolio with your firm. The young doctor whose practice has matured and expanded thanks to your help will likely look to you for investment advice and retirement planning. The do-it-yourselfer who has seen the fruits of the financial plan you created for him may become tired of doing it all himself and trust you to do it for him. You will be the trusted advisor they turn to!

These clients are basically your investments and, as with any investment, there are some risks involved. For instance, you may not see the same profits per client as compared to a traditional client billed by AUM. But, by opening your firm to those who were previously cut off from your services, you are going to experience a world of opportunity now—and more importantly, in the future.