“Clearly we are not in total control right now—we’re going in the wrong direction.”

—Dr. Anthony Fauci, National Institute of Allergy and Infectious Diseases, June 30, 2020

Key takeaways

- U.S. stocks wrapped up their best quarter in more than two decades. In the second quarter, the S&P 500 was up +20% (best quarter since 1998), the DJIA was up +18% (best quarter since 1987), and the Nasdaq was up +31% (best quarter since 1999).

- According to Fed Chair Powell, “the path forward for the economy is extraordinarily uncertain and will depend in large part on our success in containing the virus.” (CNBC)

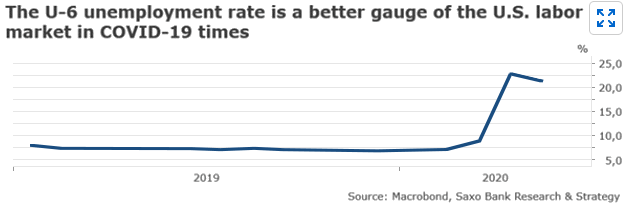

- Nonfarm payrolls increased by 4.8 million in June while the unemployment rate fell to 11.1%. However, a broader measure of unemployment known as the U6 suggests the “real” unemployment rate was 18% in June. (CNBC, MarketWatch)

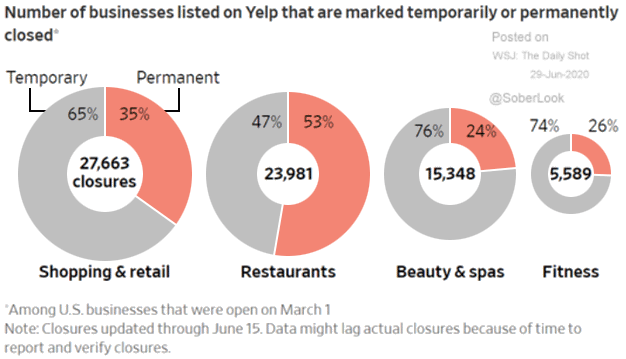

- According to the Wall Street Journal, more than half (53%) of the 23,981 restaurant closures in the U.S. are permanent. 35% of the 27,663 shopping and retail closures are permanent, 24% of the 15,348 beauty and spa closures are permanent, and 25% of the 5,589 fitness center closures are permanent.

- Dr. Anthony Fauci, one of the nation’s top infectious disease experts, told Congress he “would not be surprised if we go up to 100,000 [cases] a day if this does not turn around.” (CBS News)

- Fourteen (14) states have either paused or reversed their reopening efforts as of Wednesday, July 1, 2020. (NYT)

Stocks wrap up best quarter over 2 decades

| U.S. Stock Market Data |

| 7/2/2020 Close |

Week |

YTD |

1-year |

| S&P 500 |

3,130.01 |

1.50% |

-3.12% |

4.48% |

| NASDAQ |

10,207.63 |

1.90% |

13.76% |

24.94% |

| DJIA |

25,827.36 |

0.32% |

-9.50% |

-4.22% |

Source: MarketWatch

1. Market update

U.S. stocks wrapped up their best quarter in more than 20 years, a remarkable rally after the coronavirus pandemic brought business around the world to a virtual standstill.

Just three months ago, investors were lamenting the end of the bull market—and the longest economic expansion on record—after major U.S. stock indexes lost about 35% of their value in less than six weeks. The subsequent rebound has been nearly as brisk.

Partly thanks to an unprecedented $1.6 trillion stimulus package from the Federal Reserve and Congress and a surge in trading among individual investors, the rally has lifted everything from beaten-down energy stocks to apparel retailers to big technology firms.

The S&P 500 finished the second quarter up 515.70 points, or 20%, to 3100.29, its biggest percentage gain since the last three months of 1998. The Dow Jones Industrial Average added 3895.72 points, or 18%, to 25812.88, its best quarter since 1987.

The Nasdaq Composite, which is heavily weighted toward big technology stocks including Apple and Microsoft, has fared even better as it was up 31% in the second quarter and is +12% for the year.

- More than 40% of the companies in the S&P 500 have pulled their guidance. Many companies cite the overall uncertainty of the pandemic for their tentativeness, but some point to the likelihood of additional outbreaks, evolving consumer habits and levers such as the need to boost pay for frontline workers. (WSJ)

- The gap between the top and bottom S&P 500 valuation quintiles is the largest since the tech bubble. The average valuation of the top quintile is 29x, and the average valuation of the bottom quintile is 10x (traditionally, the average was 19x P/E and 10x P/E, respectively). (WSJ)

- The Nasdaq Composite hit a record high on Thursday, July 2, 2020 when it ticked above 10,221.85.

- Gold climbed above $1,800 for the first time since 2011 on Tuesday, June 30, 2020.

- The year 2020 is halfway over, which means the third quarter is upon us. Historically, the third quarter has been the weakest quarter of the year. Since 1950, returns in Q1 are 2.4%, Q2 are 1.8%, Q3 are 0.6%, and Q4 are 3.9%. (LPL Financial)

2. COVID-19 summary

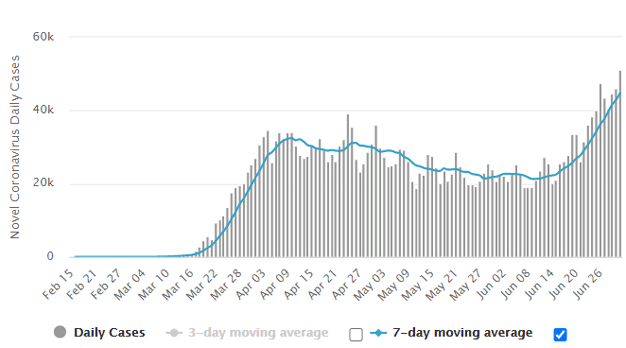

Figure 1: Daily New Cases in the U.S.

Source: Worldometers&v=adwegcfudh3zto0rkez42wex

- As of July 2, 2020, there were more than 2.69 million COVID-19 cases and over 128,000 deaths in the United States. Worldwide, there have been more than 10.7 million cases and over 517,000 deaths. (Johns Hopkins University)

- Johns Hopkins University reported more than 50,000 new coronavirus cases were confirmed in the U.S. on Wednesday, July 1, 2020. This was a single-day record. New daily cases in the U.S. rose 27% week-over-week. According to a concerned Dr. Fauci, “the numbers speak for themselves.” (COVID-19 Tracking Project)

- Dr. Fauci said that he “would not be surprised” to see the number of daily new coronavirus cases balloon to 100,000 per day if the country does not take action to stop the spread of new infections. (CBS News)

- On June 29, 2020, the World Health Organization warned that “the worst has yet to come” with COVID-19. WHO Director-General, Tedros Adhanom Ghebreyesus, said that the COVID-19 crisis is “far from over” and that a divided world “is helping the virus to spread.” (PNO)

- Economists at Goldman Sachs find a national mask mandate would increase usage substantially and cut the daily growth rate of confirmed COVID-19 cases by 1%, to 0.6%. Weighted against other potential actions to reduce the infection rate, Goldman concludes: “A face mask mandate could potentially substitute for lockdowns that would otherwise subtract nearly 5% from GDP.” (WSJ)

- An experimental COVID-19 vaccine being developed by the drug giant Pfizer and the biotech firm BioNTech spurred immune responses in healthy patients, but also caused fever and other side effects, especially at higher doses. (STAT)

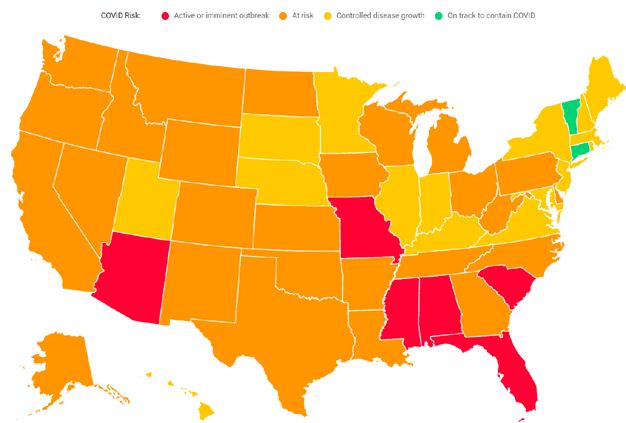

- As of July 2, 2020, only four states are on track to contain COVID-19. On the other hand, there are active or imminent outbreaks in six states, and 24 states are at risk. (covidactnow.org)

Figure 2: States With Outbreaks and at Risk as of July 6

Source: Covid Act Now&v=adwegcfudh3zto0rkez42wex

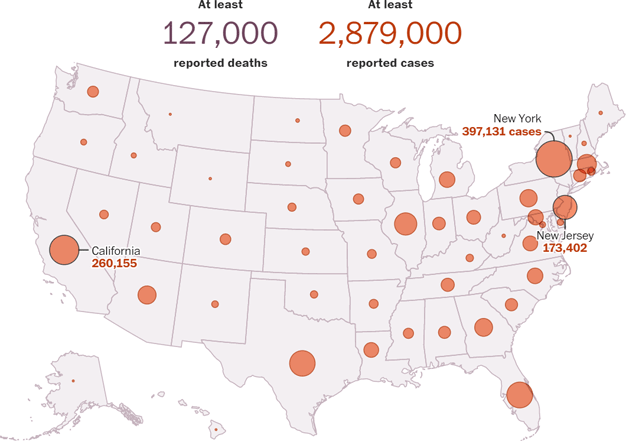

Figure 3: COVID-19 Cases and Death in the U.S. Updated June 6, 12:45 a.m.

Source: Washington Post

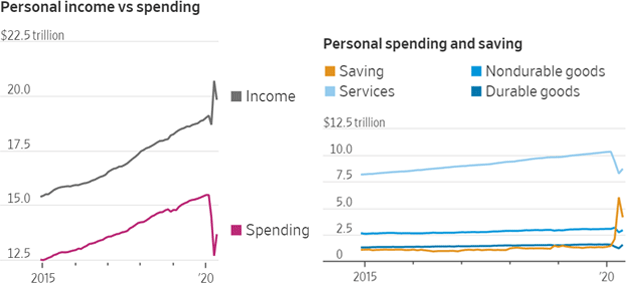

3. Spending and income swings

Americans are cautiously beginning to spend more, helping the economy slowly dig out from a severe recession.

Household spending on goods and services rose a record +8.2% in May. This was more than double the prior all-time high on records dating back to 1959. The report boosted hopes that a good portion of consumers are eager and able to spend despite historically high unemployment.

However, it also shows just how far the economy has to go to recover from this deep recession as consumer spending remained down 12% from pre-lockdown levels.

Spending in May rose but remained below pre-coronavirus pandemic levels. Income remained high after surging thanks to government stimulus.

Figure 4: Personal Income, Spending and Saving

Source: Commerce Department, Wall Street Journal

4. The economy right now

- According to Fed Chair Powell, “the path forward for the economy is extraordinarily uncertain and will depend in large part on our success in containing the virus.” Powell added that “a full recovery is unlikely until people are confident that it is safe to reengage in a broad range of activities.” (CNBC)

- According to the Wall Street Journal, more than half (53%) of the 23,981 restaurant closures in the U.S. are permanent. Of the 27,663 shopping and retail closures 35% are permanent; 24% of the 15,348 beauty and spa closures are permanent; and 25% of the 5,589 fitness center closures are permanent.

Figure 5: U.S. Businesses Are Shuttering

Source: Wall Street Journal

- The ISM manufacturing activity index jumped by +9.5 points in June to 52.6—the largest monthly increase since August 1980 and back into expansion territory. Readings above 50 indicate expansion and mark a milestone turnaround after just two months ago when the measure slid to an 11-year low of 41.5. (Cetera Investment Management)

- The biggest U.S. banks could be saddled with as much as $700 billion in loan losses in a prolonged downturn according to the Federal Reserve. Being that banks cannot tell who is creditworthy so easily anymore, they have pulled back sharply on lending to U.S. consumers during this pandemic. (WSJ)

- The central bank opened its $500 billion lending program to support issuance of new debt by large corporations. This explains why there have been fewer corporate failures than expected. (WSJ)

- Pending home sales notched a record-setting 44.3% monthly increase in May, which is an incredibly positive sign for the U.S. economy. “The housing market is likely benefiting from low mortgage rates, stronger demand for larger spaces as more and more people work from home and a desire to move away from crowded cities to avoid exposure to the coronavirus,” said economist Rubeela Farooqi of High Frequency Economics. (WSJ)

- Consumer confidence partially rebounded in June as it increased to 98.1, beating survey estimates of 91.5. Although it increased substantially since its 85.9 reading in May, it remains well below pre-pandemic levels of 101.0. (Advisor Perspectives)

- After recovering rapidly from mid-April through mid-June, the economy has shown signs of sputtering in the past two weeks. Multiple data sources show that after an initial V-shaped plunge and partial rebound, activity has since flatlined, resembling the reverse image of the square-root symbol (√). (WSJ)

- IHS Markit, an economic-analysis firm, sees a 20% chance that a second wave of infections could result in a W-shaped recovery. “Official backtracking on the relaxation of restrictions as well as voluntary pullback on the part of consumers could cause spending to weaken again sharply, throwing the economy back into a brief two-quarter recession,” it said. (WSJ)

- Fourteen (14) states have either paused or reversed their reopening efforts as of Wednesday, July 1, 2020. (NYT)

- Over 40% of the population has seen reopening either halted or reversed as of Wednesday, July 1, 2020. (WSJ)

- China’s official manufacturing purchasing managers index climbed to a three-month high of 50.9 in June, from 50.6 in May. Although China’s growth is picking up, the world’s second-largest economy remains far from a full recovery. (WSJ)

5. Unemployment

- Nonfarm payrolls increased by 4.8 million in June while the unemployment rate fell to 11.1%. However, a broader measure of unemployment known as the U6 suggests the “real” unemployment rate was 18% in June. (CNBC, MarketWatch)

Figure 6: A Better Gauge of Unemployment

Source: Wall Street Journal

- Initial jobless claims rose by 1.427 million, marking the 15th straight week in which initial claims remained above 1 million. (The Labor Department)

- Continuing jobless claims rose to 19.3 million, an increase of about 60,000 from the week prior. (CNBC)

- About half of the U.S. population is jobless, according to the U.S. employment-to-population ratio. While the unemployment rate (11.1% in June) measures those who are actively looking for and available to work, this metric measures the employment of the entire adult population. Approximately 52.8% of the adult population is employed while 47.2% of adults in the U.S. are not currently working. (WSJ)

- Dr. David Kelly of JPMorgan Chase says that it should be “noted that classification errors appear to be artificially suppressing the measured unemployment rate. The impact of these errors should fade even as employment slowly rises, leaving the unemployment rate in double digits well into 2021.”

- According to Fed Chair Powell, “a second outbreak would force government and people to withdraw again from economic activity.” (Yahoo Finance)

6. Bullish thinking

- Chief Global Strategist at JPMorgan, Dr. David Kelly, said that “it is important to acknowledge that many countries in Europe and particularly in East Asia have been more successful than the U.S. in taming the virus and should consequently experience shallower recessions and quicker rebounds.”

- JPMorgan believes that the “U.S. will remain the relative regional outperformer and that the style leadership will firmly return to tech and defensive, post the tactical value rally seen in [second half] of May and [first half] of June.” (MarketWatch)

- Investors looking for income should consider dividend income from equities in sectors that appear less vulnerable to a long pandemic. (JPMorgan)

- For fixed income investors, mortgage-backed securities remains one of LPL Financials preferred areas for diversification in portfolios. (LPL Financial)

- Of the top 10 best quarters since 1950, the S&P 500 Index has climbed every time in the next quarter with an average 8% jump. SunTrust Advisory chief market strategist, Keith Lerner, said that while history is “only a guide,” he expects it to be repeated with the onset of a bull market and the S&P 500 higher in a year’s time. He expects an uneven path for the Index as the economy reopens in “fits and starts,” but one with a positive trajectory. (MarketWatch)

- Adam Kobeissi, founder and editor-in-chief of the Kobeissi Letter, said that over the short-to-medium term, the path of least resistance for stocks appears to be higher, with the technical picture suggesting a move to 3,150, which marks the high from June 15 to June 23, and a break above that would send the index to 3,275. (MarketWatch)

7. Bearish thinking

- Dr. Kelly believes that “from an economic perspective, this rolling-wave pandemic likely eliminates hopes for a full V-shaped recovery in advance of a vaccine. The basic problem is that there are many businesses that cannot reopen in a way that is profitable or sustainable, while still assuring consumers and workers that they are not putting their health in jeopardy. These businesses include a multitude of firms in the travel, accommodation, food services, personal services, entertainment, sports and retail industries.”

- Janet Yellen predicts a GDP and an employment gap through 2022, with too much debt and restrained spending and the Fed unable to “achieve distributional objectives.”

- According to Rick Rieder, Director of Fixed Income at BlackRock, markets are “jumpy,” with a 4% equity risk premium, and low interest rates making certain parts of the market uninvestable.

- According to the Wall Street Journal, a Democratic sweep of the White House and Congress looms as a potential risk to the stock market in the months ahead. Many analysts believe that a Democratic-controlled government would likely roll back the tax cuts Congress enacted in 2017, constraining corporate profit margins.

- For now, investors should position their assets not just for the hope of an early cure but the more likely path of a long struggle with a rolling-wave pandemic. (JPMorgan)