“We have all done the best that we can do to tackle this virus and the reality is that it’s brought this nation to its knees.”

—Dr. Robert Redfield, Centers for Disease Control and Prevention, June 23, 2020

“The next couple of weeks are going to be critical to address those surges we’re seeing.”

—Anthony Fauci, National Institute of Allergy and Infectious Diseases, June 23, 2020

Key takeaways

- Florida, Texas, California and Arizona have all seen spikes in new cases. On Thursday, June 25, 2020, new COVID-19 cases hit a daily record of nearly 40,000 in the U.S. as Florida recorded 8,942 new cases and Texas recorded 5,996 cases. The Texas governor ordered bars to close and put restrictions on outdoor gatherings. (Johns Hopkins University, WSJ)

- New York, New Jersey and Connecticut imposed quarantines for incoming travelers from hotspot states, while several states have paused re-openings, tightened social distancing restrictions, and added mask requirements. Hospital capacity is garnering increased concern. (COVID-19 Tracking Project)

- As of June 26, 2020, there were more than 2.43 million cases and over 124,000 deaths in the United States. Worldwide, there have been more than 9.65 million cases and over 490,000 deaths. The United States has double the cases than the next country, Brazil, with 1.2 million. (Johns Hopkins University)

- The five largest mega-cap stocks in the S&P 500 have increased +90% since the beginning of 2018 versus +16% for the broader market. (Bloomberg)

- The International Monetary Fund cut its 2020 estimate of global economic output from -3.0% to -4.9%, according to the latest World Economic Outlook.

- Dr. Anthony Fauci, director of the National Institute of Allergy and Infectious Diseases, said that it’s possible to have a viable COVID-19 vaccine within a year of the coronavirus first coming to the attention of the U.S. government. The Trump administration has said they aim to have a vaccine by January 2021 as part of Operation Warp Speed. (MarketWatch)

- The office of the U.S. Trade Representative said it is considering additional tariffs on $3.1 billion worth of products from France, Germany, Spain and the U.K. The products under consideration include olives, coffee, chocolate, beer, gin, trucks and machinery. (CNBC)

- There were 13 bankruptcy filings last week, the most in a week since May 2009. (Bloomberg)

S&P, Dow down to lowest level since June 11 slide

| U.S. Stock Market Data |

| 6/26/2020 Close |

Week |

YTD |

1-year |

| S&P 500 |

3,009.05 |

-2.86% |

-6.86% |

+2.29% |

| NASDAQ |

9,757.22 |

-1.90% |

+8.74% |

+21.87% |

| DJIA |

25,015.55 |

-3.31% |

-12.34% |

-5.96% |

Source: MarketWatch

1. Market update

The divergence in the performance of the major U.S. stock indexes this year is the widest in more than a decade. A surge in big technology stocks has helped the Nasdaq Composite rally 8.74% in 2020, while the Dow Jones Industrial Average is down -12.34%. The benchmark S&P 500 is hovering in between them, off -6.86%.

The Nasdaq’s dominance over the Dow and S&P 500 is the biggest since 1983. The gap between the S&P 500 and the Dow is the widest since 2002, when the Dow was ahead.

One explanation for the gap in returns: A handful of growth stocks that have surged this year have an outsize influence on the Nasdaq and the S&P 500. Apple, Microsoft, Amazon, Google parent Alphabet and Facebook together account for about 40% of the Nasdaq and around 20% of the S&P. Of those stocks, only Apple and Microsoft are in the Dow. With that being said, it is no surprise that the equal-weighted S&P 500 Index is lagging again. Since the COVID-19 recovery remains uncertain, investors continue to bet on the tech mega-caps—the new “safe-haven” asset class.

- Price-to-earnings ratios remain elevated at 21.4x. The last time it was near this mark was during the tech bubble, when it was around 24x.

- The five largest mega-cap stocks in the S&P 500 have increased +90% since the beginning of 2018 versus +16% for the broader market. (Bloomberg)

- According to the Wall Street Journal, three sectors of the S&P 500 are in positive territory for the year: information technology (Microsoft and Apple), consumer discretionary (Amazon), and communication services (Alphabet and Facebook). The energy, financial, industrial and utility sectors are down by double digits for the year.

- Only eight of the DJIA 30 constituents are positive on the year. Most of the Dow’s gains have been wiped out by the slide of Boeing. The aerospace company’s shares have tumbled about -40% this year due to the slump in air travel prompted by the pandemic and the grounding of its 737 MAX jet. (Wall Street Journal)

- The Nasdaq has beat the S&P 500 by almost 20% over the past 12 months. As of Friday, June 26, 2020, the S&P 500 is +3.8% year-over-year while the Nasdaq is +23.2% year-over-year.

- The outperformance of growth stocks versus value stocks continues to widen. As of Friday, June 26, 2020, the SPDR S&P 500 Growth ETF is +17.8% year-over-year while the S&P 500 Value ETF is -3.9% year-over-year.

2. COVID-19 summary

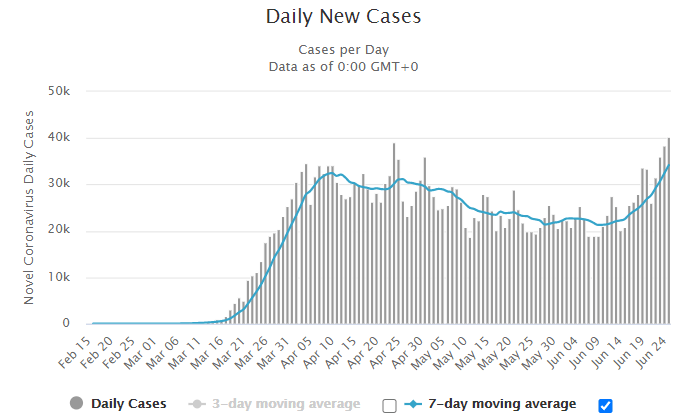

Figure 1: Daily New COVID-19 Casesin U.S.

Source: worldometers.info, June 26, 2020

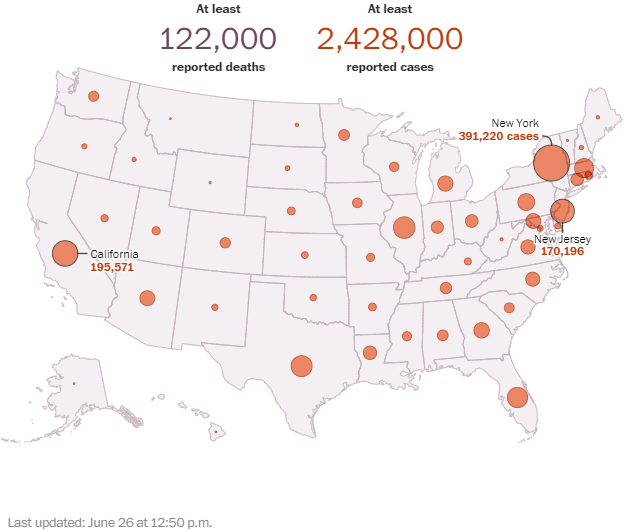

- As of June 26, 2020, there were more than 2.43 million cases and over 124,000 deaths in the United States. Worldwide, there have been more than 9.65 million cases and over 490,000 deaths. The United States has double the cases than the next country, Brazil, with 1.2 million. (Johns Hopkins University)

- Florida, Texas, California and Arizona have all seen spikes in new cases. On Thursday, June 25, 2020, new COVID-19 cases hit a daily record of nearly 40,000 in the U.S. as Florida recorded 8,942 new cases and Texas recorded 5,996 cases. The Texas governor ordered bars to close and put restrictions on outdoor gatherings. (Johns Hopkins University and Wall Street Journal)

- New York, New Jersey and Connecticut imposed quarantines for incoming travelers from hotspot states, while several states have paused re-openings, tightened social distancing restrictions, and added mask requirements. Hospital capacity is garnering increased attention. (COVID-19 Tracking Project)

- According to the Wall Street Journal, Latin America is emerging as the new center of the coronavirus pandemic. There have been more than two million people infected and over 100,000 deaths. The region has 8% of the world’s population but has accounted for 47% of coronavirus deaths over the past two weeks.

- Dr. Anthony Fauci, director of the National Institute of Allergy and Infectious Diseases, said that it’s possible to have a viable COVID-19 vaccine within a year of the coronavirus first coming to the attention of the U.S. government. The Trump administration has said they aim to have a vaccine by January 2021 as part of Operation Warp Speed. (MarketWatch)

Figure 2: Cases Across the U.S. as of June 26

Source: Washington Post

3. PMIs improve, but are still below 50

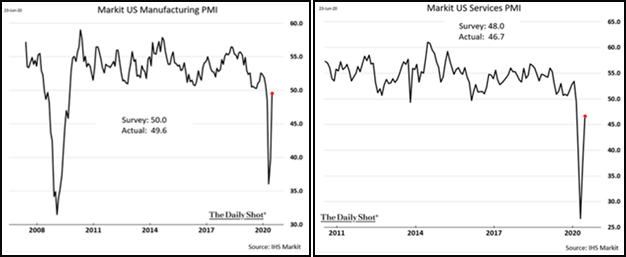

Both the IHS Markit Flash manufacturing and services PMIs improved from the prior month but are still below 50 and thus in contraction. The U.S. manufacturing PMI was 49.6 while the U.S. services PMI was 46.7. They both missed expectations, but the improvements are a good sign for the economy.

Figure 3: Purchasing Managers’ Index

Source: IHS Markit

4. What else is going on in the economy right now?

- The office of the U.S. Trade Representative said it is considering additional tariffs on $3.1 billion worth of products from France, Germany, Spain and the U.K. The products under consideration include olives, coffee, chocolate, beer, gin, trucks and machinery. (CNBC)

- The International Monetary Fund (IMF) cut its 2020 estimate of global economic output from -3.0% to -4.9%, according to the latest World Economic Outlook.

- Sales of existing homes declined by -9.7% in May to an annualized pace of 3.91 million, missing expectations for 4.09 million. The May decline is the third straight monthly decline, dropping in all four U.S. regions. The pullback is greatest in the condo and co-op market.

- May consumer spending rose a record +8.2%, a sign the U.S. economy is growing again, but a rise in new virus infections threatens the nascent recovery. (Wall Street Journal)

- Corporate credit in advanced economies have hit a record high as a percentage of GDP. Oxford Economics estimates that it could surge 10% this year, to around 95% of GDP. The recent trends in bank lending and bond issuance (plus declining GDP) are set to push up the corporate debt ratio sharply in advanced economies. This level risks being a drag on economic growth. (Oxford Economics)

- There were 13 bankruptcy filings last week, the most in a week since May 2009. (Bloomberg)

- Gold prices approached a new seven-and-a half-year high as front-month gold futures for delivery in June rose +0.6% to $1,756.70. Prices are +16% for the year, boosted by coronavirus-related economic uncertainty, and expectations for more stimulus spending and low interest rates. (Wall Street Journal)

- U.S. personal savings rates are at almost 35%, a rate not ever seen. To put it in perspective, the rate didn’t reach 10% during the 2008–09 crisis. The accumulation of savings will undoubtedly slow sharply as purchases that were simply impossible during full lockdowns are completed. But, only a fraction would have to remain to keep savings at historic highs. That now seems likely to have long-lasting effects on financial markets and depressing interest rates for years to come. (Wall Street Journal)

5. Unemployment

- Initial claims for unemployment benefits totaled 1.5 million last week with a smaller-than-expected decline of 60,000 from the prior week’s revised tally. This is the third week in a row at roughly this level.

- Although new jobless claims are down for a 12th week, the COVID-19 impact is slowing the pace of weekly declines. This is more evidence that the previous pattern of steadily declining claims has been interrupted. It could mean that businesses are still under stress, and that the level of economic disruption will continue at a high level for a while.

- Continuing claims declined by more than forecast to 19.5 million. They were 20.5 million the week prior.

- While fresh filings for unemployment claims have fallen 12 straight weeks from a peak near seven million in late March, the gradual decline in recent weeks (and still staggering number of unemployed) point to a long road ahead for the U.S. job market to fully recover from the pandemic. (LPL Financial)

- June’s unemployment rate comes out on Thursday, July 2, 2020. The May unemployment rate was 13.3%, more than double the 50-year average of 6.2%. However, economists peg the real unemployment rate to be closer to 19%.

- Aftershocks of deep recessions can continue for years. Claims remained stubbornly high for years after the 2008–09 recession, and their peak claims were much lower at 665,000 jobless claims (now 1.5 million).

6. Bullish thinking

- Byron Wien, Vice Chairman of Blackstone Advisory Partners, believes that “a recovery is underway and we have seen the cycle low for the economy and financial markets.” He expects volatility to continue, however. (Blackstone)

- LPL Financial believes that the IMF’s new forecasts may be overly pessimistic, particularly their expectation for a -4.9% contraction in global GDP this year. However, LPL finds comparing their forecasts across regions instructive: They point to the sharpest declines in Europe and Latin America, and some of the smallest declines in Asia, including potential positive growth in China. Pandemic containment is only part of the story, but these growth forecasts support LPL’s continued preference for Asia over Latin America and emerging markets over developed international. (LPL Financial)

- Bullish options trades on U.S. stocks, gold and silver have become popular as investors parse potential outcomes in the recovery from COVID-19, according to OCBC Securities. (Bloomberg)

7. Bearish thinking

- David Kostin, Head of U.S. Equity Strategy at Goldman Sachs, expects “the potential risk of a viral ‘second wave’ and the fast-approaching U.S. Presidential election will limit a significant increase in equity exposures in the near term.” (CNBC)

- Another wave of COVID-19 cases could bring a further round of economy-devastating lockdowns, and “the Presidential election could see a change in the country’s highest office.” (Business Insider)

- Nick Bunker, Economist at Indeed, said “we’re seeing a slowdown in layoffs, but hiring hasn’t picked up a tremendous amount. The recovery from this is going to potentially be a very long slog if we can’t get the virus under control quickly.” (Wall Street Journal)

- Ryan Detrick, Senior Market Strategist at LPL Financial, said that “as good as the recent economic data has been, we want to make it clear, it could still take years for the economy to fully come back.” During the 10 recessions since 1950, it took an average of 30 months for lost jobs to finally come back. It took four years for the jobs lost during the tech bubble recession of the early 2000s to come back and more than six years for all the jobs lost to come back after the Great Recession. (LPL Financial)