The Health Savings Account (HSA) is unique in the landscape of tax-preferenced investment accounts, as it is the only type that enjoys both the benefit of tax-deductible contributions and tax-free distributions (for medical expenses).

In fact, the unique treatment of the HSA has created a wrinkle in the traditional approach of funding retirement accounts. Given the inevitability of medical expenses in retirement, arguably the best savings account for retirement (or at least for a portion of retirement expenses) is to use an HSA for retirement over “just” an IRA alone.

In other words, for any retiree that is saving for both medical expenses in retirement and also all of their other retirement goals, using a combination of an IRA (for most retirement expenses) supplemented by an HSA as a “retirement health savings account” may be the most tax-preferenced way to save holistically for retirement. In fact, the HSA tax treatment is so good that it can even be superior to funding a 401(k) plan with a small match (for those who haven’t already started a health savings account for retirement)!

Notably, this doesn’t mean that retirees would exclusively fund a health savings account for retirement, as the accounts are both taxable and potentially subject to penalties if used for nonmedical purposes. But for those who already have some retirement accounts, and/or have more than enough dollars overall to achieve their goals, the fact remains that contributing the maximum to an HSA every year has the potential for more beneficial tax treatment than any other type of tax-preferenced account! This makes accumulating in an HSA so desirable that it may even be preferable to pay current medical expenses out of pocket, just to preserve (and keep contributing to) the HSA account balance to be used as a future health retirement account!

Health savings account rules

The HSA was created as a part of the Medicare Prescription Drug, Improvement, and Modernization Act of 2003. The basic concept of the HSA is that it is a savings account to be used for health/medical expenses, with preferential tax treatment.

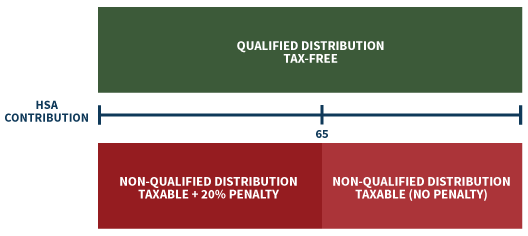

Contributions to the HSA are pretax (either tax-deductible if contributed directly, or excluded from income if contributed by an employer on behalf of an employee). Withdrawals from an HSA for qualified medical expenses are tax-free (although nonqualified withdrawals are taxable as ordinary income plus a 20% penalty tax, with the penalty waived for those over age 65, or who are disabled, or if withdrawn as a nonspouse beneficiary after the death of the HSA owner).

Figure 1: HSA Qualified and Non-Qualified Distribution Rules

Source: Michael Kitces

Qualified medical expenses are generally any expenses that would otherwise be eligible for the medical (and dental) expenses deduction, along with any expenses paid for a doctor-prescribed drug.

Qualified medical expenses also include insurance premiums for health insurance coverage under COBRA, health care coverage while receiving unemployment compensation, Medicare (but not Medigap) premiums, and even long-term care insurance (but only up to the age-based LTC premium limits).

In order to be eligible to participate in (i.e., to contribute to) an HSA, you must be covered under a High-Deductible Health Plan (HDHP), and not be enrolled in Medicare or other health coverage, nor claimed as a dependent on someone else’s tax return. A “high-deductible” health plan must have a minimum deductible of $1,300 for self-only coverage or $2,600 for family coverage (in 2016), and can have a deductible as high as $6,550 for an individual or $13,100 for a family (in 2016).

Notably, while HSAs were intended to help cover medical expenses associated with high-deductible health plans, the contribution limits to an HSA are set lower than the (maximum) limits on deductibles (though a health insurance plan may have a lower deductible to conform to the HSA limits).

In 2016, the maximum contribution limit to an HSA is (only) $3,350 for an individual, or $6,750 for a family, plus a $1,000 “catch-up” contribution for those over age 55 (unlike retirement accounts, where catch-up contributions apply beginning at age 50.)

What if you don’t use your HSA right away? Not a use-it-or-lose-it account!

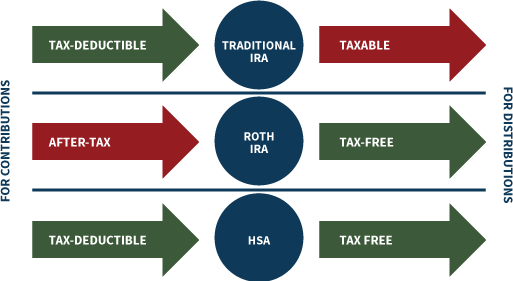

Ultimately, the HSA is unique from the tax perspective, as it is one of the only accounts that permits both a tax deduction upfront for contributions and can produce tax-free distributions for growth later—unlike retirement accounts, which may be pretax up front but taxable later [e.g., a traditional IRA or 401(k)], or are tax-free later but receive no tax deduction up front [e.g., a Roth IRA or 401(k)].

Figure 2: Tax Treatment of Contributions and Distributions to HSA and IRA Accounts

Source: Michael Kitces

And despite this uniquely generous tax treatment for an HSA, there is actually no time limit on when funds in an HSA must be used. An HSA does not have a “use-it-or-lose-it” provision like the Flexible Spending Account (FSA) where anything more than $500 of unused funds are forfeited at the end of the year.

Instead, as long as they were permitted to be contributed into the HSA in the first place (i.e., the HSA owner was covered under an HDHP at the time), HSA funds can remain in the account for an extended period of time (growing on a tax-deferred basis) and be used (tax-free) later.

In turn, the only requirement at the time of distribution for tax-free treatment from an HSA is that the withdrawal either cover a current medical expense, or be used to reimburse a prior one (that was itself paid out of pocket, was not reimbursed from another source, and was not previously claimed as an itemized deduction). This means that medical expenses can occur now and be reimbursed later (even far later) in the future and still be qualified, as long as documentation of the medical expense is maintained and as long as the medical expense occurred after the HSA was originally established.

Alternatively, this means that funds can be contributed now to an HSA, and grow tax-free for years or even decades, before being used (tax-free including all those years of growth) for a distant future medical expense.

Even further extending the favorable deferral period for an HSA, the rules stipulate that if the HSA is not used before death, a surviving spouse can continue the HSA in his/her own name and continue the preferential tax treatment (including future tax-free withdrawals). This form of HSA spousal rollover is similar to that permitted for retirement accounts.

HSA: A supplemental retirement vehicle

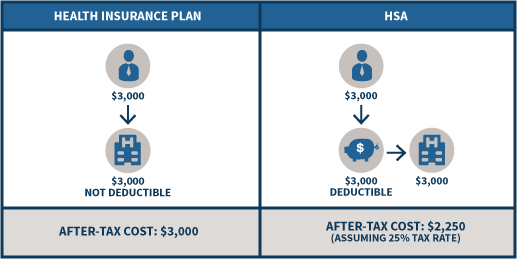

The classic view of an HSA is that it’s an account to hold the money that someone sets aside to cover the deductible for their health insurance. Funds are contributed to the account on a pretax basis, and to the extent they’re subsequently used (typically that year) to cover the unreimbursed expenses associated with the health plan’s deductible, the end result is that health expenses are paid on a pretax basis (with the HSA as the “conduit” to make that happen).

This is often a better tax treatment than paying health care expenses directly from a checking account, where payments are just “normal” medical expenses with a deduction limited to 10% of adjusted gross income (AGI) for those under age 65…which means most or all medical expenses paid out of pocket don’t actually produce a tax benefit.

Figure 3: Tax Treatment of Paying Deductible vs. Using an HSA

Source: Michael Kitces

In addition, to the extent that not all the funds for the HSA are actually used on medical expenses for the current year—for instance, the account owner didn’t actually incur enough medical expenses to use the funds in the first place—the remaining account balance simply “carries over” to be used in a subsequent year.

Other health savings account uses

Because there’s no requirement that HSA funds be used to cover medical expenses in the current year—the HSA can be used in the future—an alternative opportunity emerges: to contribute funds to an HSA, and deliberately not use them as medical expenses are incurred. Instead, medical expenses are paid out of pocket—in addition to the HSA contribution—and the HSA funds are allowed to accrue (tax-free) for future use instead.

Of course, the caveat to this approach is that it’s only helpful if the funds really can be used in the future on a tax-free basis. If it turns out they have to be withdrawn as a nonqualified distribution, inhospitable taxes plus a 20% penalty will apply.

Yet the reality is that for a future retiree, the odds are overwhelming that some medical expenses really will be applicable in retirement. In fact, “typical” retiree expenses on health care are often as much as $500/month (or $1,000/month for a married couple), much of which covers HSA-eligible qualified medical expenses like Medicare premiums and out-of-pocket medical costs (although Medigap coverage doesn’t count).

Cumulatively, Fidelity’s annual “Health Care Cost Estimate” study for retirees estimates that a 65-year-old couple will need a whopping $245,000 to cover health care expenses in retirement.

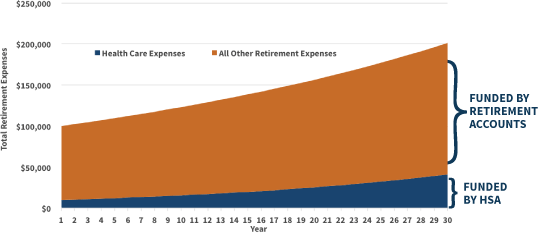

In other words, if we think of expenses in retirement as including both medical and “other” retirement expenses (where “other” includes housing, entertainment, food, lifestyle, and everything else that isn’t medical), then an HSA can be used to save for the medical portion of retirement expenses, and retirement accounts can be used for all other retirement expenses.

In fact, with the virtual certainty of ongoing Medicare premiums, contributing to an HSA now is effectively a form of Medicare Health Savings Account, allowing tax-free growth for future Medicare expenses. This is ultimately a better strategy than “just” using retirement accounts for retirement, given that the HSA has better tax treatment (pretax going in and tax-free coming out) than any type of retirement account (which only gets the tax-deduction up front or tax-free distributions, but not both).

Paying medical expenses out of pocket to defer HSA distributions for Medicare premiums

Given that eligibility to contribute to an HSA starts with being a participant in a high-deductible health plan—which means if a health event happens, there will be significant out-of-pocket medical expenses to cover—the strategy of using an HSA as an accumulation vehicle to supplement retirement effectively means having a high-deductible health plan, funding the HSA, and then not using the HSA for the inevitable health care expenses that occur.

This can place a nontrivial cash flow burden on the household, as it means it’s necessary to have far more cash on hand—enough to cover the pretax contribution to the HSA (as much as $3,350 for an individual and $6,750 for the family), plus the health plan’s actual deductible (which could be as high as $6,550 for an individual and $13,100 for a family!)

And as noted earlier, most of that health insurance deductible will not likely be tax deductible, either. In other words, the household’s cash-flow commitment to health care expenses may be increased by upwards of 50% over what might have been set aside for just the health insurance deductible alone.

Nonetheless, to the extent that a household really does have more than enough to cover the health insurance deductible, the reality is those excess funds were going to be saved somewhere anyway. So the real question is whether to contribute to the HSA and use it for medical expenses (and then save the rest elsewhere), or to contribute to the HSA and use other funds for medical expenses instead.

Contributing to the HSA and using other funds for medical expenses means that the HSA can grow (tax-free) until retirement and then be used to cover Medicare premiums and other retiree health care expenses.

Figure 4: Funding Retirement With HSA and Other Retirement Accounts

Source: Michael Kitces

Paying nondeductible medical expenses while growing an HSA for retirement

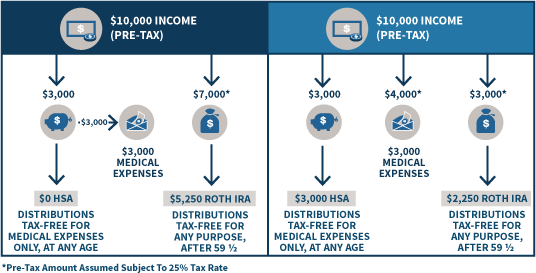

Imagine an individual who has $10,000 of pretax funds available, is in a 25% tax bracket, and has a health insurance plan with a $3,000 deductible.

The first option might be to contribute $3,000 to a health savings account (subsequently paid out to cover the health insurance deductible). This leaves $7,000 of pretax income (after the HSA income), of which $1,750 (which is 25%) will go to taxes and the remaining $5,250 will be contributed to a Roth IRA. The end result is that the medical expenses have been covered (pretax) and the individual finishes with a $5,250 Roth IRA.

The second option is to contribute $3,000 to a HSA (on a pretax basis), and then cover the $3,000 of anticipated medical expenses out of pocket. Since the health care expenses won’t likely be deductible, it will really require $4,000 of pretax income to have $3,000 left over. With the remaining $3,000 of pretax income, the individual can again pay the 25% tax rate, have $2,250 left over, and contribute that $2,250 to a Roth IRA. The end result is $3,000 in an HSA and $2,250 in a Roth IRA.

Figure 5: Using an HSA for Medical Expenses vs. Supplementing Roth IRA Contributions

Source: Michael Kitces

Notably, the outcome of this scenario is that when medical expenses paid out of pocket will not be deductible, the individual ends with the same amount of total dollars in tax-preferenced accounts. It’s either $5,250 in a Roth, or $5,250 split between a Roth and an HSA.

Arguably, in this scenario the HSA is not necessarily materially better, nor is it materially worse. Both accounts will be eligible for tax-free distributions for their respective purposes in retirement. The only difference is that distributions from the Roth IRA cannot be tax-free under age 59½, while earlier distributions from the HSA could be tax-free for medical needs (in exchange for the fact that over 59½ they’re still only for medical expenses).

Deductible medical expenses above the AGI limits and an HSA contribution

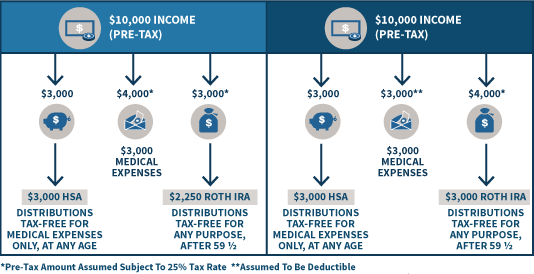

For those whose medical expenses actually will be deductible—perhaps because income is low and the threshold can be reached, or because there are other medical expenses (e.g., for other family members) that together will add up to or exceed the 10%-of-AGI threshold, the situation is different.

Continuing the prior example, now the individual contributes $3,000 to a health savings account, and only needs $3,000 of pretax income to cover actual medical expenses (since they are assumed to be deductible). He thus has $4,000 of pretax income left over, yielding $3,000 as a Roth IRA contribution after 25% (or $1,000) is held aside for taxes. The end result—in this case, there’s $3,000 in the HSA and also $3,000 in a Roth IRA.

Figure 6: Funding an HSA While Paying Medical Expenses Out of Pocket (Deductible or Not)

Source: Michael Kitces

In other words, to the extent that medical expenses actually will be deductible anyway, the tax savings on medical expenses frees up additional dollars to contribute to the Roth IRA. In essence, it’s a double tax deduction opportunity—for the medical expenses now, and for the HSA to fund medical expenses in the future, and the HSA grows tax-free in the meantime.

Again, this assumes the individual has enough free cash flow in order to fund all of these simultaneously—the HSA, the medical expenses out of pocket, and the Roth IRA.

Nonetheless, to the extent there are dollars for all three, whenever the medical expenses are at least partially deductible, more dollars can be placed into tax-preferenced accounts.

HSA contributions for those who maxed out retirement accounts

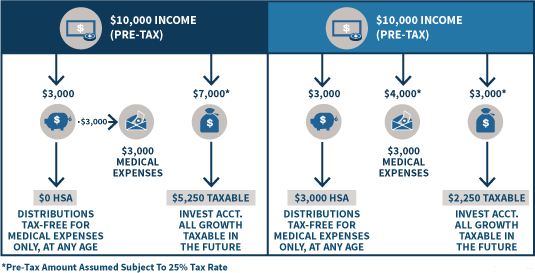

In the scenario where retirement accounts have been fully “maxed out” already (e.g., 401(k) plans, a pretax IRA, or a backdoor Roth IRA, etc., have already been done), contributions to an HSA become even more appealing. Because in this situation, the “excess” dollars that don’t go towards medical expenses will simply end up in a taxable brokerage account, which is clearly less favorable than having dollars in a tax-preferenced health savings account for retirement.

For example, imagine again a scenario with $10,000 of pretax income to allocate, where retirement accounts are not an option because the contribution limits have already been reached. The first option, again, is to contribute $3,000 to the HSA and use those funds for the actual health insurance deductible; the remaining $7,000 of pretax income turns into $5,250 of after-tax dollars, which end up in a taxable investment account.

On the other hand, if the HSA contribution is preserved in the account and the medical expenses are paid out of pocket, the investor finishes with $3,000 in the HSA and $2,250 in the taxable investment account. While the latter scenario still has a total of $5,250 in investment dollars, the difference is that now $3,000 of those funds will grow tax-free for the future!

Figure 7: Superiority of Accumulating With an HSA for Those Who Maxed Out Retirement Accounts

Source: Michael Kitces

When a retirement HSA can beat a traditional retirement account (even with a 401(k) match)

Notably, all of the earlier scenarios have assumed that the individual in question will have medical expenses to pay for in the current year (such that it’s necessary to fund an HSA contribution and pay health expenses out of pocket). However, a unique situation arises when there won’t be any medical expenses to pay (e.g., because the insured is actually healthy and doesn’t anticipate any medical costs). In other words, what if there aren’t any dollars needed for medical expenses at all right now, and it’s just a question of which to contribute to—a retirement account like an IRA or 401(k), or a retirement health savings account instead?

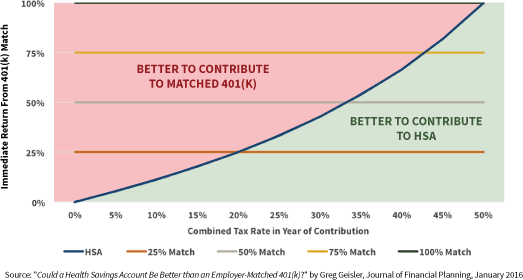

All else being equal, the HSA will be the dominant account in this situation. The simple reason is that, as noted earlier, the HSA is both tax-deductible on contributions and tax-free on (qualified) distributions, while a retirement account is either tax-deductible up front or tax-free for distributions, but never both. In fact, the HSA is so dominant to a retirement account over a head-to-head situation that it can be more profitable in the long run to contribute to an HSA even if the 401(k) has a small match.

For instance, if a contribution to a 401(k) offers a 25% match, but the individual faces a future tax rate of 20%, then $1 contributed to a 401(k) is still only worth $1 in after-tax value (as the match increases it to $1.25 but the taxes decrease it back to $1). Which is exactly the same as simply contributing the $1 of pretax income to an HSA, also worth $1 of after-tax value.

In turn, this means at any tax rate higher than the aforementioned 20%, it’s actually better to contribute to the HSA than to get the match with the 401(k). At combined state-plus-Federal tax rates of 45%+, an HSA can even be superior to a 401(k) with a 75-cents-on-the-dollar match, as shown in the research from a recent Journal of Financial Planning article entitled “Could A Health Savings Account Be Better Than An Employer Matched 401(k)?” by Greg Geisler.

Figure 8: 401(k) Matches Compared to Tax Savings of HSA Contributions

Source: Michael Kitces

Again, as noted earlier, a head-to-head contribution to an HSA over a 401(k) plan with a match only wins in situations where there are not any medical expenses to pay out of pocket. In scenarios where there are, it’s better to get the “double” tax benefits of contributing to the 401(k) and using the HSA to pay medical expenses on a pretax basis as well. But where there won’t be any anticipated medical expenses, the HSA especially shines.

Which arguably means the starting point for anyone should be to contribute to the HSA first (if eligible), see if there are medical expenses later in the year (and whether they can or cannot be deducted if paid out of pocket), and then decide whether to contribute additionally to a 401(k) or IRA.

Either way, the HSA would be the starting point, and for limited dollars, might be the end point as well, given the inevitable combination of a health savings account and Medicare spending in the future!

Ultimately, the HSA is really the best savings account for retirement for those who can afford to contribute to retirement accounts, have an HSA, and have the cash flow or reserves to pay medical expenses out of pocket as well. Presuming, of course, that the HSA dollars will be invested for growth in the long run, and not held in a cash or low-return holding account.

So what do you think?

Do you ever counsel clients to contribute to an HSA before a retirement account? Would you consider doing so in the future? Tell us about it in the conversation box below.