If you have clients who are experiencing adverse financial consequences as a result of Covid-19, taking a loan from an employer-sponsored retirement plan might be one of the solutions to overcoming such challenges. For qualified individuals, the Coronavirus Aid, Relief, and Economic Security (CARES) Act increases the loan amount to the lesser of $100,000 or 100% of the participant’s vested account balance—up from $50,000 or 50%. But stipulations apply and clients should be made aware of these before signing on the dotted line to enter into a plan loan agreement.

Background

A loan from a qualified employer plan is treated as a distribution to the receiving participant, unless the loan meets certain requirements. These include:

- A limitation on the dollar amount—generally up to $50,000 or 50% of the participant’s account balance, whichever is less

- A minimum repayment period of five years

- Level amortized repayments made at least quarterly

A plan loan that does not meet applicable requirements might be treated as a deemed distribution. While loans are excluded from income and therefore nontaxable, a loan that results in a deemed distribution would not benefit from this special income exclusion—and would instead be included in income for the borrowing participant. Any taxable amount would also be subject to a 10% early distribution penalty, if the participant is under age 59½ at the time of the distribution, unless an exception applies.

There are exceptions to these general rules—some of which are provided under the CARES Act. Let’s take a refresher of some of the key loan rules and an overview of the exceptions made under the CARES Act.

1. Employer plans are not required to offer loans

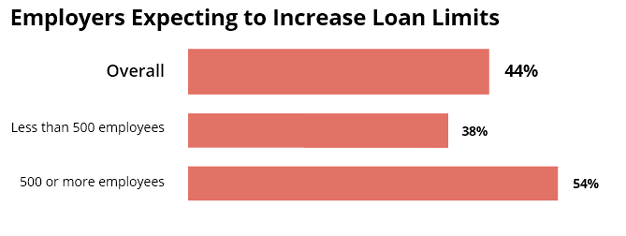

While a loan is an allowable feature of an employer-sponsored qualified retirement plan (employer plan), an employer is not required to offer loans under its employer plan. And even for those that offer loans, amending a plan to include coronavirus-related plan loan provisions is optional. As such, a plan sponsor may choose whether to extend the coronavirus-related plan loan provisions to plan participants. In fact, a recent survey conducted by PLANSPONSOR pulse showed that only 44% of employers were expected to include the coronavirus-related loan provisions under their defined contribution plans.

Figure 1: Limited Adoption of the Coronavirus Provisions

Source: PLANSPONSOR

Clients who want to take advantage of the coronavirus-related loan provisions should contact their employers to determine whether the plan does or will extend these provisions.

2. Only qualified individuals are eligible for coronavirus-related loans

If an employer plan extends the coronavirus-related loan provisions to plan participants, only qualified individuals would be eligible to take advantage of those provisions. A qualified individual, according to IR-2020-124, is anyone who:

- is diagnosed, or whose spouse or dependent is diagnosed, with the virus SARS-CoV-2 or the coronavirus disease 2019 (collectively, “Covid-19”) by a test approved by the Centers for Disease Control and Prevention (including a test authorized under the Federal Food, Drug and Cosmetic Act); or

- experiences adverse financial consequences as a result of the individual, the individual’s spouse, or a member of the individual’s household (that is, someone who shares the individual’s principal residence):

- being quarantined, being furloughed or laid off, or having work hours reduced due to Covid‑19;

- being unable to work due to lack of childcare due to Covid‑19;

- closing or reducing hours of a business that they own or operate due to Covid‑19;

- having pay or self-employment income reduced due to Covid‑19; or

- having a job offer rescinded or start date for a job delayed due to Covid‑19.

An employer may rely on a participant’s certification of “qualified individual” status. IRS Notice 2020-50 includes a sample employee certification that a plan may use for this purpose.

3. Loan limits double under the CARES Act for qualified individuals

The CARES Act doubled the limits for loans made to qualified individuals on or after March 27, 2020 and before September 23, 2020. As a result, a qualified individual who is eligible to take a plan loan may borrow up to the lesser of $100,000 or 100% of that qualified individual’s vested account balance or accrued benefit.

Loans outside of this provision are generally limited to the lesser of $50,000 or 50% of the participant’s vested account balance. In some cases, a loan limit may be up to $10,000, even if that amount is greater than 50% of the vested account balance or accrued benefit.

Reminder: If a participant already has an outstanding loan balance, the plan administrator must take that into consideration when determining the maximum amount for which the participant would be eligible.

4. More time for qualified individuals to repay loans

There are two key rules modified for qualified individuals under the CARES Act:

- Except for any loan that is used to acquire the participant’s principal residence, the repayment period for a plan loan must not exceed five years.

- Repayments must be made in level amortized amounts, at least quarterly, unless an exception applies.

Under the CARES Act, an exception is made for qualified individuals with outstanding loans on or after March 27, 2020. Under this exception:

- Loan repayments that are required to be made from March 27, 2020 to December 31, 2020 may be suspended for one year; and

- When determining whether a loan has been repaid by the end of the five-year maximum period, this delayed period would not be counted.

Qualified individuals who want to take advantage of this provision must consider the following:

- The loan repayments must resume after the suspension period has ended.

- Interest would continue to accrue during the suspension period.

- Interest accrued during the suspension period would be added to the remaining principal.

- When repayments begin, they would be adjusted to reflect the delayed period and any interest accruing during the delayed period.

- To determine the new payment amounts, the remaining loan balance plus the interest accrued during the suspension period would be reamortized for the remaining period, plus the additional year.

The following is an example from the IRS, applying the safe harbor rule (some sentences excluded for brevity), with my commentary.

Example

On April 1, 2020, a participant with a nonforfeitable account balance of $40,000 borrowed $20,000 to be repaid in level monthly installments of $368.33 over five years.

My comment: By my calculations, the interest rate is 4%, which means that the total repayments, including interest, would be $22,099.85.

The participant makes payments for three months, April 2020–June 2020.

My comment: Here, the remaining loan balance would be $19,091.99.

| |

Payment (principal plus interest) growth |

Loan balance |

| |

|

$20,000 |

| April, 2020 |

$368.33 |

$19,698.34 |

| May, 2020 |

$368.33 |

$19,395.67 |

| June, 2020 |

$368.33 |

$19,091.99 |

The participant’s employer takes action to suspend payroll withholding repayments for the period from July 1, 2020–December 31, 2020, for loans to qualified individuals that are outstanding on or after March 27, 2020.

Because the participant is a qualified individual, no further repayments are made on the participant’s loan until January 1, 2021 (when the balance is $19,477).

My comment: By the IRS’s math, the interest accrued during the suspension period is $385.01. I must admit that, after using several online calculators, I came up about $18 short.

At that time, repayments on the loan resume, with the amount of each monthly installment reamortized to be $343.27 in order for the loan to be repaid by March 31, 2026 (which is the date the loan would have originally been fully repaid, plus one year).

Please note: The IRS permits other “reasonable” methods to be used to administer this provision. Qualified individuals should consult with their employer regarding the specific terms of the suspension, repayment schedule and repayment amounts.

Should your client take a coronavirus-related loan?

Even if a client is eligible to take a coronavirus-related loan, consideration should be given to other available options. Factors that should be considered include the cost of the retirement plan loan versus the cost of a loan from another lender, the loss of opportunity for tax-deferred growth on the loan amount until it is repaid, the overall impact on retirement savings, and the fact that missing loan repayments could result in a deemed distribution.

Some of these points of consideration have contributed to the long-standing debate about whether it makes good financial sense to take loans from retirement savings. But, in this time of Covid-19, immediate financial needs likely transcend such a debate. Nevertheless, when advising a client about taking a loan, all the pros and cons should be considered.