As an advisor, you know that segmenting your client list is critical to firm operations. It is especially important if you are looking for sustainable growth, as the segmentation helps you service clients more efficiently as you scale up. Although client segmentation does organize valuable information for each client (AUM, revenue generated and so on), it does not necessarily provide insight into the client’s full financial picture.

Because of this, we have found it beneficial to segment clients further when providing tax planning and estate planning services, taking into consideration several other factors that impact these additional planning areas.

At Taylor Financial Group (TFG), we have built out separate client segmentations to aid us when we are performing Roth conversion analyses and estate plan reviews throughout the year. Below we discuss the specific information we pull and how we organize it for each service.

1. Client segmentation for Roth conversion analyses

At TFG, we typically run Roth conversion analyses throughout the year, culminating in Q4 when we have the best idea of our clients’ tax projection for the year. However, we are currently presented with a unique opportunity to perform Roth conversions at a discount with the market down.

So it is more important than ever to be proactive in identifying clients who should take advantage of this opportunity

before Q4—and before they reach out to us. As a result, we began reviewing our client list in Q1 and performing an analysis for those that we believe should be doing a Roth conversion today. And needless to say, the hope is they will benefit from the tax-free growth when the market bounces back up.

Once you pull your client list, there are several factors to consider that can help you determine who may benefit from performing a Roth conversion today as well as who to target for an analysis. Of course, the most critical factor is the client’s tax-deferred balance, including those traditional retirement accounts that are held away.

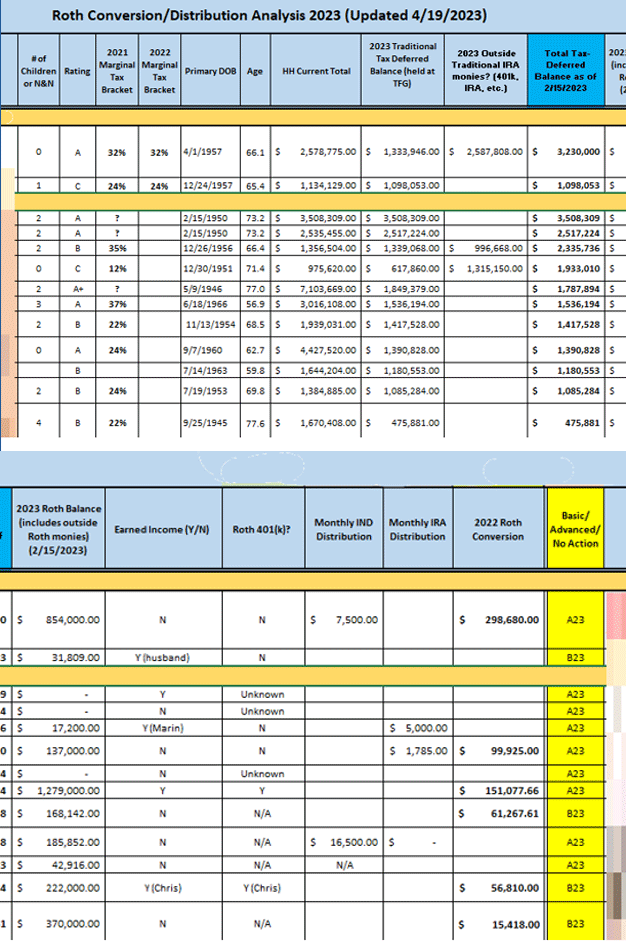

We initially organize the client segmentation by largest tax-deferred balance to smallest. In addition, we look at various other criteria such as the client’s age(s), if they are working, if they are already taking distributions from their accounts, if they have Roth assets already, and if they have any children. See below for a snapshot of the custom spreadsheet we built to track all of this information (the spreadsheet is halved so you can read the print).

Figure 1: Spreadsheet for Evaluating Roth Conversion Analysis

Source: Taylor Financial Group

Based on all of this information, we review each client’s situation individually and determine if we will be doing an advanced, multi-year Roth conversion analysis using Income Solver or a basic, single-year Roth conversion analysis using Holistiplan. As a general rule of thumb, we will perform an advanced analysis for a couple with a tax-deferred balance of $1.5M+ or a single client with $1M+. Those that fall under that minimum will typically get the basic Holistiplan analysis that looks at the current year tax projection only.

Generally, we have found that a client with a $2M+ tax-deferred balance today will see the greatest benefit from doing a Roth conversion today in terms of lifetime tax savings and Roth account growth (allowing for exceptions based on the client’s particular situation). And, if the client has a tax-deferred balance between $1M and $1.5M, we often see that they can fall into a gray area where overall tax savings (and therefore the value of a Roth conversion) is not as compelling. Then the decision becomes more personal for the client.

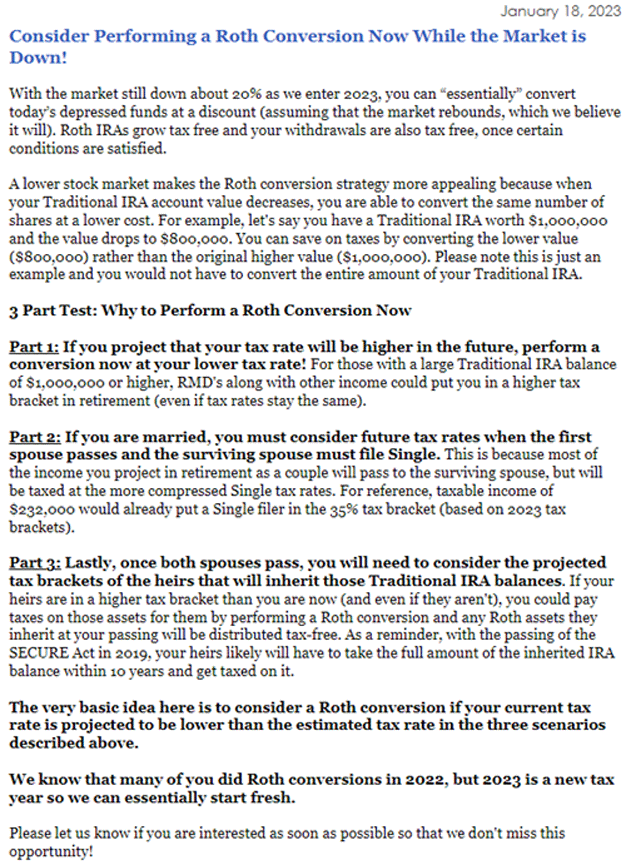

In addition to our own internal review, we also sent out a general announcement in January to all clients with traditional IRA/401(k) balances, should they be interested in performing a Roth conversion with the market down. We decided to send a broad-based announcement (see below) in case clients have personal reasons to do a Roth conversion that we may not have been aware of.

Figure 2: TFG Q1 Roth Conversion Announcement

Source: Taylor Financial Group

2. Client segmentation for estate plan reviews

In 2023, another key planning area we are focusing on at TFG is estate planning. This is an extremely complex area that has very little standardization, which is why many advisors stay away from it. However, we also know that estate planning is extremely important and needs to be addressed, especially for high-net-worth clients.

In this planning area, the most critical item to consider is net worth. You can only put together a meaningful segmentation if you have your client’s full financial picture. As any advisor knows, AUM only tells you part of the story in most cases.

For example, a client may have $1M in investable assets at your firm but have several real estate investments. Or your client of 10 years will let you know one day that they have millions in outside investments they never told you about. Because of these unknowns, it may be best to outline proper expectations and add disclosures in your communications, clarifying that any changes in the assumptions you have used will alter your recommendations and analysis.

To start the segmentation, we pulled the net worth values from our planning software (Money Guide Pro or eMoney) and organized the list from largest to smallest (see Figure 4). Clients with $2M+ would receive an advanced estate plan review and those with less than $2M would get a general estate plan review.

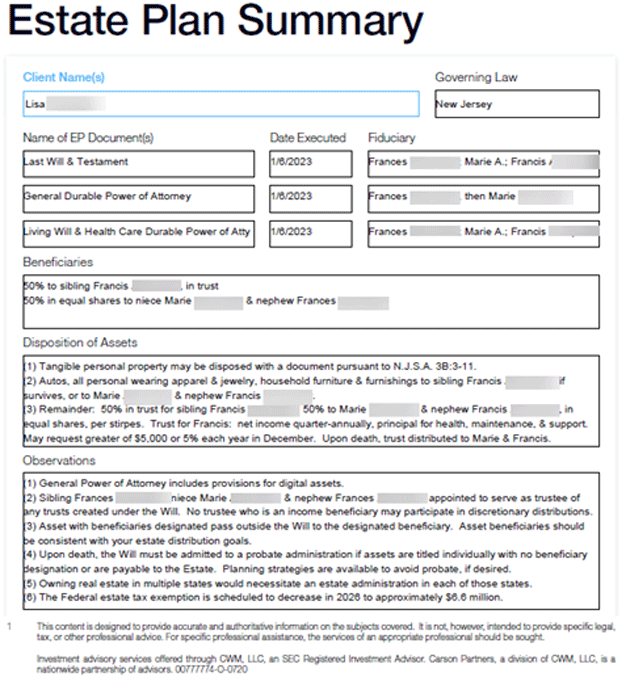

The major difference between the advanced and general review is that we will also put together an asset waterfall for the client as part of the advanced analysis. In contrast, the general review focuses mainly on reviewing the estate planning documents. Figure 3 below shows a sample below of the estate plan summary that we send to clients.

Figure 3: TFG Estate Planning Summary

Source: Taylor Financial Group

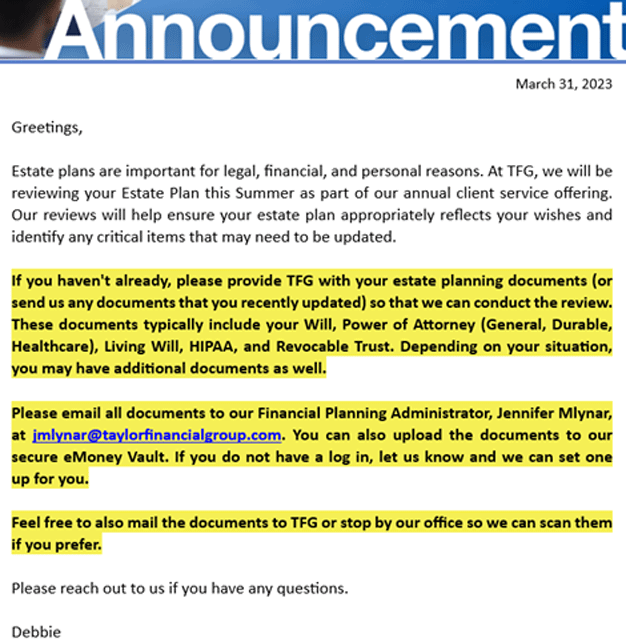

In addition, another critical part of the estate plan review process (for both advanced and general reviews) involves the estate planning documents. Therefore, we sent out an announcement in March (see Figure 5) requesting the clients’ estate planning documents, should we not have them already or if they have been updated.

Figure 5: TFG Estate Planning Document Request

Source: Taylor Financial Group

Taking the time to build out specialized client segmentation spreadsheets for the different services you offer could help to scale up your output and increase organization and efficiency in your firm. Most important, you will be delivering the appropriate services to the right clients. As a result, you will also be able to better serve your clients (which is the ultimate goal)!