The fear of rising health care costs eating away at retirement savings has never been greater. In 2017, estimated health care expenses for retirees had risen to an average of $275,000 per couple (and had the potential to rise as high as $565,142 per couple). This average is expected to continue to grow, and it doesn’t even include long-term care expenses.

Have you thought about how this could affect your clients’ retirement savings? If you’re not preparing your clients for these rising health care costs and how they might impact their retirement plans, you could be setting them up for a big surprise in their future! And I’m not talking about the kind of surprise that will make them feel warm and fuzzy inside.

This is where a health savings account (HSA) can play a major role! Most people, especially up until now, have not considered an HSA much more than a savings account for people who are enrolled in high-deductible health plans. We meet with clients all the time who are completely unaware of the advantages of an HSA. There’s so much more to it. If you really think about it, an HSA is a retirement account too! Here are some key points about HSAs that you should know and share with your clients.

Clients are probably HSA-eligble

If your client is enrolled in a high-deductible health care plan, then she is eligible to open an HSA. These days, most health care plans are high-deductible, otherwise, you’re paying a hefty premium. Typical plans nowadays have a lower monthly premium with higher out-of-pocket expenses. If your client isn’t sure which type of plan she has, advise her to ask her Human Resources Department or call her insurance company directly to confirm. You can also offer to have clients call you, and you can help them take the necessary steps to figure it out. This is what we offered our clients, and many of them did call for help. A quick and easy way to add value to your services by going above and beyond for your clients!

Money contributed can be used tax-free

What sets an HSA account apart from a regular savings account is that an HSA is a tax-advantaged medical savings account. What does this mean? Your client can use HSA funds to pay for deductibles, copays, and other qualified health care expenses—without having to pay federal income taxes. Not to mention, by the way, that the money your client contributes is also tax-free at the time of contribution.

For instance, if your client’s insurance plan does not cover dental or vision services, she can use her HSA to pay for those expenses. The best part is that whatever money your client hasn’t used at the end of the year can be rolled over year after year, which means she never loses what she contributes.

Another cool tax benefit is that HSAs can be transferred from one HSA to another without any tax penalties. So, even if your client is leaving a job and her HSA is employer-sponsored, she need not fret! Just advise her to move her HSA to her next employer-sponsored HSA account or find her own.

Lastly, once your client turns 65, the benefits get better. All HSA distributions after age 65 are penalty-free, even if the funds are not used for qualified health expenses. However, if you take a distribution that is not used for qualified medical expenses, it will be taxable. It’s essentially the same as having an IRA.

Contribution limits

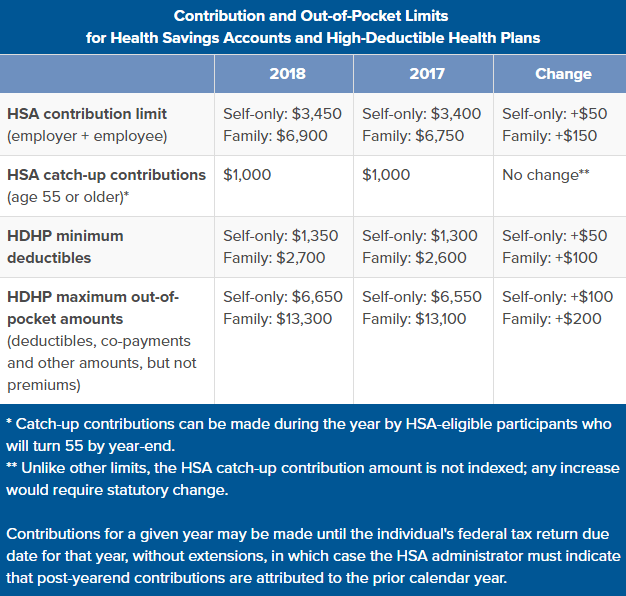

Contributions have increased for 2018. The limit will now be $3,450 per person, and $6,900 for families, with additional contribution options for catch-up contributions, minimum deductibles, and maximum out-of-pocket amounts. The below table outlines the HSA contribution limits for 2018.

Figure 1: 2018 vs. 2017 HSA Contribution Limits

Source: Society for Human Resource Management

A supplemental retirement savings account

For those clients who have maxed out their 401(k) and IRA contributions for the year, an HSA is another tax-deferred way for them to save their money. And, since they can carry the balance over from year to year, in the long term, they could save a whole lot! In fact, CNN Money reported that if a person contributes the max allowed for 40 years (without using any of it for actual health care costs), she could save anywhere from $360,000 to $1.1 million, depending on the rate of return. That’s incredible! Obviously, the point of an HSA is to use it for medical expenses whenever it’s necessary, but this example illustrates what’s possible for those who do not need to tap the money along the way.

As we face the possibility of health care expenses significantly diminishing our clients’ retirement savings, it’s important for us to educate clients and help them plan for these costs. Part of that is setting them up with an HSA—a retirement account specifically set aside to help them pay medical expenses, so that their other retirement savings can be used for all the stuff they’ve always dreamed about. Trust me, they will think of you and thank you when they’re enjoying a relaxing afternoon on the patio of their summer vacation home that they were able to buy with the hard-earned money they saved for retirement.

If you haven’t discussed HSA accounts with your clients yet, now is the time to get started! Help them see the value and advantages that an HSA can provide. And, remember to offer them help to figure it all out. It’s these little gestures that make a big difference and help clients see how much you care.