As we all know, inflation is at the highest level we’ve seen in four decades. June’s inflation of 9.1% over last year marks the highest increase since December 1981 and the fourth straight month for inflation above an 8% rate. Understandably, clients are concerned. Remind them the best way to combat rising inflation is to return to the basics: Know what your income is and what you are spending your money on, have a long-term plan, and consider ways to maximize all of your investments, including your cash.

Here are eight actions you can take on behalf of your clients to limit inflation’s impact in their lives until we come out on the other side of this.

1. Revisit cash flow

Get a handle on your client’s income and expenses. Understand where their income comes from and whether it is “guaranteed and secure” income or not. Also break up expenses into necessary versus discretionary, as this can help the exercise.

On the other side of the ledger, slow down (or stop) withdrawals from investment accounts until the market rehabilitates. And reconsider those discretionary expenses for the time being—Italy will be just as beautiful in 2023 as it is now. And perhaps buying, building or renovating your home makes better sense when prices are more reasonable.

Here’s another scenario that might cause someone to act quick—or just try waiting it out, according to Barron’s. At the end of last year, a 30-year fixed rate mortgage was 3.11%, according to Jacob Channel, LendingTree’s senior economist. A $300,000 loan at that rate would cost $1,283 a month. At 5.23%, that monthly payment is $1,653, Channel said.

And, think twice about drawing from IRAs, which often are taxed at those higher ordinary income tax rates. Instead, delaying expenses can also include delaying that RMD until later in the year when the market recovers. You can explain to them how you will help in this way. In the meantime, encourage clients to draw down some of the idle cash that is likely sitting in their bank accounts.

2. Review the good debt and bad debt

These days, most of your clients have some type of debt. A fixed rate mortgage may still make sense. However, large credit card bills likely don’t make sense, particularly in a rising rate environment. While you are at it, review all of the client’s debt, considering their lines of credit, auto loans, and so on to make sure they are not overpaying when borrowing money.

Are they serious about getting a car or a home? Lock in the rate as soon as possible, experts have said. In the near future, those numbers are just going to go up, according to Barron’s. Auto loans and mortgages don’t have the direct tie to Fed rate hikes that credit cards do, but the rates are influenced by the benchmark rate and the lending environment it creates.

And when evaluating debt, don’t be in a rush to pay off all your debt. A fixed rate mortgage at 3% likely still makes sense for your client, particularly in a high interest rate environment.

3. Open a home equity line of credit

Whether your client needs it or not, this can be a solid Plan B. Look to alternate sources of income, and consider encouraging your client to open a home equity line of credit while low interest rates are still available. Some lenders, like PNC, can offer up to 90% loan to value, allowing your clients to squeeze more cash from their elevated home price. This cash can come in handy down the road when a recession hits, and banks no longer want to lend.

4. Leverage your investment accounts

Most custodians offer collateralized loans based on the value of investment accounts, up to 60%–70%. However, these loans are not available on retirement accounts, just taxable accounts. We have had many clients utilize this option and they think we are geniuses.

They are thankful for not having to cash out accounts due to peculiar timing issues, as they could be locking in a loss (during the bad times) or having to pay capital gains (during the good times), neither of which is palatable. These loans typically only take a few weeks to approve and the interest rates are very attractive, currently at around 3%.

5. Confirm appropriate liquidity and emergency fund

Be sure that clients really do have cash at the ready if needed. A liquidity bucket means different things to different people, but we typically see that this amount is overstated by clients. So, be precise in your approach and take the time to really understand what clients need to feel comfortable. No sense in stashing too much cash away with those negative real rates of returns.

6. Consider working a bit longer

For some clients, this kind of economy might make it sensible to work a year or two longer than planned, especially if your client has been on the fence regarding a firm retirement date. A delayed retirement creates a trifecta of benefits! It delays the need to tap into retirement accounts and allows an extra year or two of contributions to the 401(k). Your client can also add to their Social Security earnings if they are in their peak earning years.

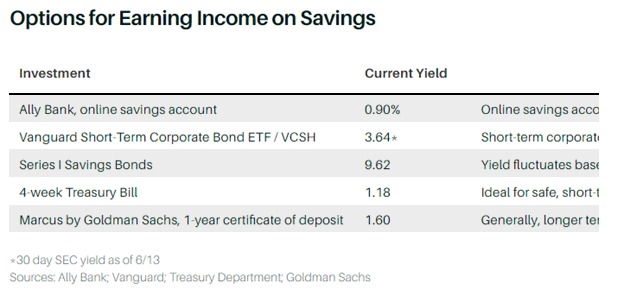

7. Look into I savings bonds

For extra money that’s sitting in your client’s savings account and earning an interest rate that is far below inflation, Series I savings bonds could be a better option. But whether or not this makes sense depends on when you’ll need to access the money. The interest rate for I-bonds shifts along with inflation and currently is at an annual rate of 9.62%. This rate resets (up or down) every six months.

You can purchase up to $10,000 of Series I savings bonds per calendar year and you can use your tax refund to invest another $5,000. You have to own these bonds for a full year before you can sell and if you cash out before holding them for five years, then you’ll forfeit the previous three months of interest.

For other income options, see the chart below.

Figure 1: Other Income Options…

Source: Taylor Financial Group

8. Remember your client’s financial plan.

When all else seems to fail, remind clients “We have planned for downturns like this. Your financial plan has a long-term outlook, factoring in bear and bull markets along the way.” Remind your client that you continuously review and update inflation assumptions based on the current environment and stress test your plan by incorporating additional expenses and high inflation.

Make sure to update their financial plan at least once a year or any time your client is preparing for a major life event. And perhaps consider sending out mid-year plan updates so that your clients can better understand how their plan is performing, given current market conditions.

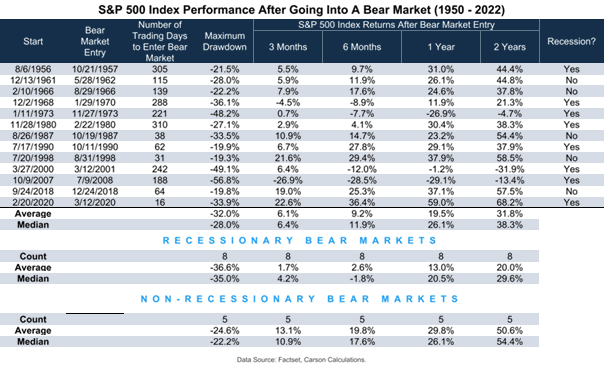

And while we are talking about cash management…

Speak to your clients about investing cash that is sitting on the sidelines. We will only know after the fact whether the bottom is here, but there is definitely a bottoming process going on, so perhaps consider dollar-cost averaging into the market for any cash your client has on hand. Data shows that the median market return 12 months from the start of a bear market is 20%–24%. That’s a pretty good number to start with.

Figure 2: Good Time to Get Cash Off the Sidelines?

Source: Taylor Financial Group

As the saying goes, nothing in life is guaranteed except for death and taxes. But, as you can see from the above, chances are very strong that one year from now, markets will be significantly higher. This may be the best thing that you ever do for your client. Help them get over their paralysis and create a plan for moving some of that money off the sidelines. Five years and 10 years from now (and probably even just one year from now), they will remember you and thank you.