If there is anything that advisors can agree on, it’s that this past pandemic year has transformed the way we communicate with our prospects and clients. With the help of technology and the willingness to pivot, at Taylor Financial Group (TGF) we have been able to provide a seamless discovery and onboarding process in one of our busiest and most unusual years ever.

The first few interactions with a new client are vitally important to building a successful relationship. Otherwise the client may feel buyer’s remorse, or that they were “closed,” and that is no way to start things off. Indeed, we see the first 45 days as absolutely critical to the start of a lifelong journey with our clients. Below we describe five strategies that shape our onboarding approach.

1. Standardize the onboarding process

It is critical to outline expectations for each individual client with your team before onboarding and create a repeatable process for that person. We hold a weekly meeting with our team (called the MOM meeting, for Meeting of the Minds), solely to discuss new client onboarding. We track all interactions and set clear deadlines and expectations for our team.

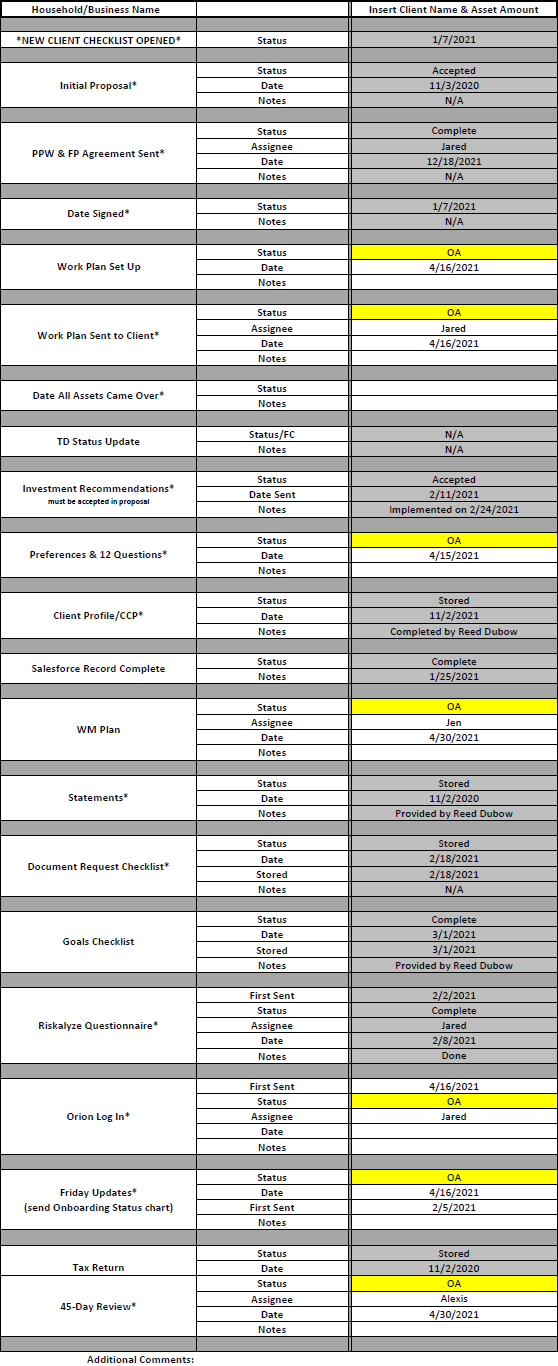

Below is a sample of our new client info-tracking sheet, which we review three times a week as a team. It includes all of the critical steps in the onboarding process, along with expected completion date and person responsible.

Figure 1: TGF Client Info-Tracking Sheet

Source: Taylor Financial Group

Establishing communication preferences is a key aspect of the onboarding process. Maybe a given client is going to require a weekly phone call or perhaps they only want to have virtual meetings because of their busy schedule. Whatever has been agreed upon, make sure your team is well aware of the expectations set for this client.

You will get a feel for the client from the first few calls and meetings you have while onboarding, so take good notes and ideally have a team member sitting in on those calls with you. We ask our new clients about service preferences as well as some questions about their personal tastes, so we can better understand not only their financial goals, but their idiosyncracies and what they enjoy doing in their free time.

For example, among our questions, we may ask:

- What types of entertainment do you enjoy?

- What type of reading (or books) do you prefer?

- How often would you like us to review your portfolio?

- Which birthday item would you prefer to receive: A birthday cake or healthy birthday gift? (Imagine shipping a diabetic client a seven-layer chocolate cake—yikes!)

Asking these kinds of questions in the beginning shows that you are thinking about all of the details and are willing to take the extra time to accommodate their needs.

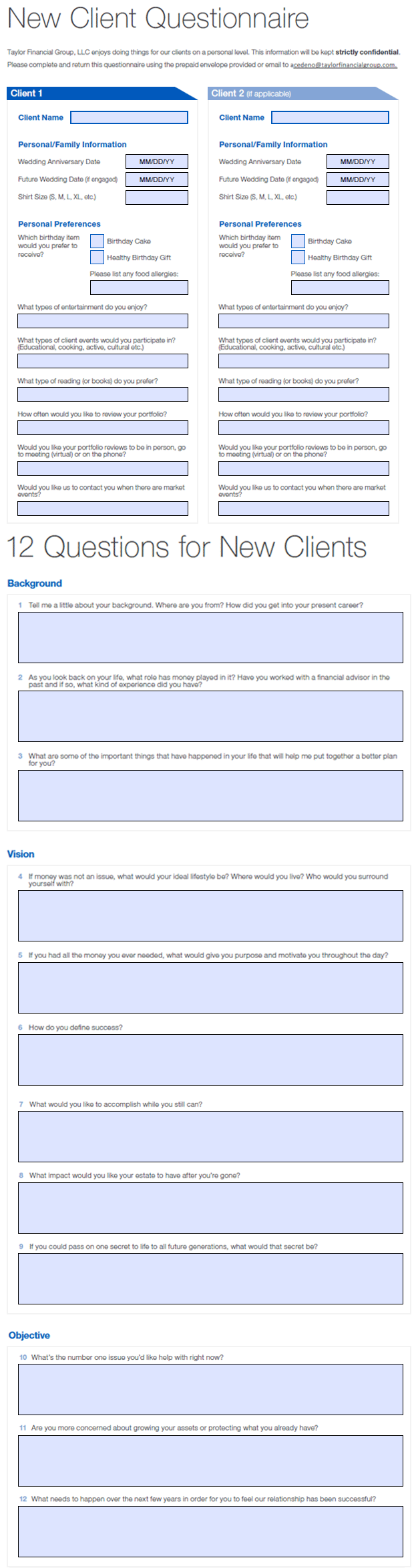

Of course, not every client is so open about their lives within the first few conversations. To accommodate those who are more reticent, we developed our New Client Questionnaire and 12 Questions Document (shown in Figure 2 below). This is sent out digitally (and can be completed online) three days after new clients have signed onboarding paperwork, and it helps us to gather additional information that isn’t always revealed within the first few conversations. We are able to use this information to guide our service model and it comes up in review meetings and other servicing areas.

Figure 2: TGF Digital New Client Questionnaire and 12 Questions Doc

Source: Taylor Financial Group

2. Provide easy and secure document storage

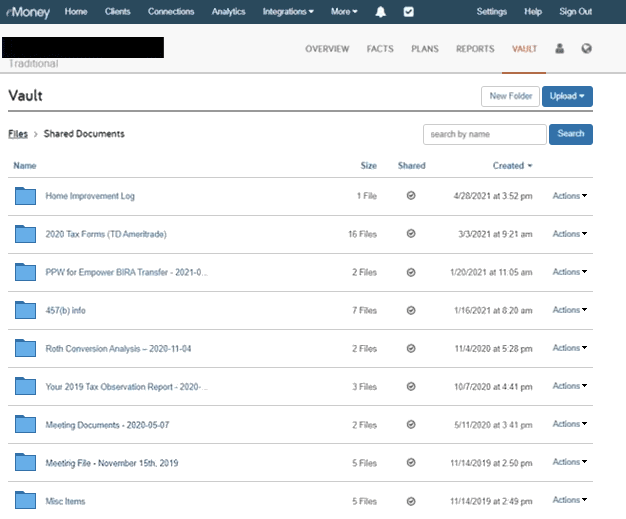

Many clients do not feel comfortable sending sensitive documents via email. That is why we use eMoney, which provides a secure vault for storing and sharing documents. The vault allows clients to upload their sensitive documents (such as tax returns), which can then easily be shared with the team. All of the important information we need to develop a client’s financial plan is centrally located in the eMoney vault for ease of access from either side. Below in Figure 3 you can take a look at a sample vault, as seen from the client’s perspective.

Figure 3: Client View of an eMoney Info Vault

Source: Taylor Financial Group

3. Consistent and timely communications are vital

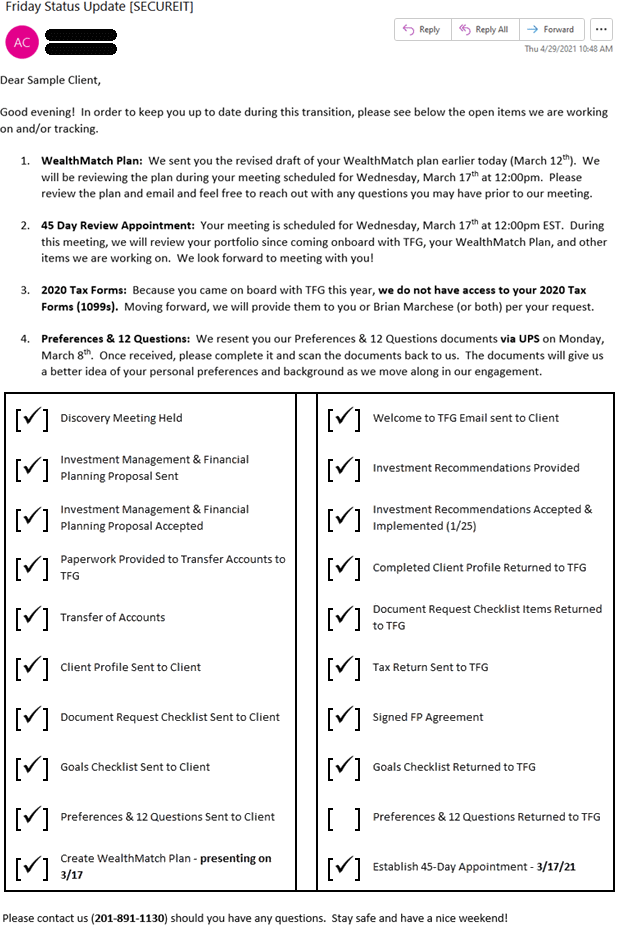

The first impression your firm gives to a client can make or break the relationship. If a client is left wondering early on why they haven’t heard from your team, they may feel less valued. We provide new clients with weekly updates via email every Friday.

This email also includes an onboarding checklist so the clients can clearly see the progress we are making on their behalf. This lets our clients know that we are on top of the work. We normally send these emails during the first six weeks after a client signs on with us. Figure 4 shows a sample of our Friday update email.

Figure 4: Onboarding With Care: TGF Friday Update Email for New Clients

Source: Taylor Financial Group

While these Friday updates are an important part of the initial client interaction, they don’t replace the attention your team pays to the clients as they onboard. Personal attention needs to extend throughout the relationship.

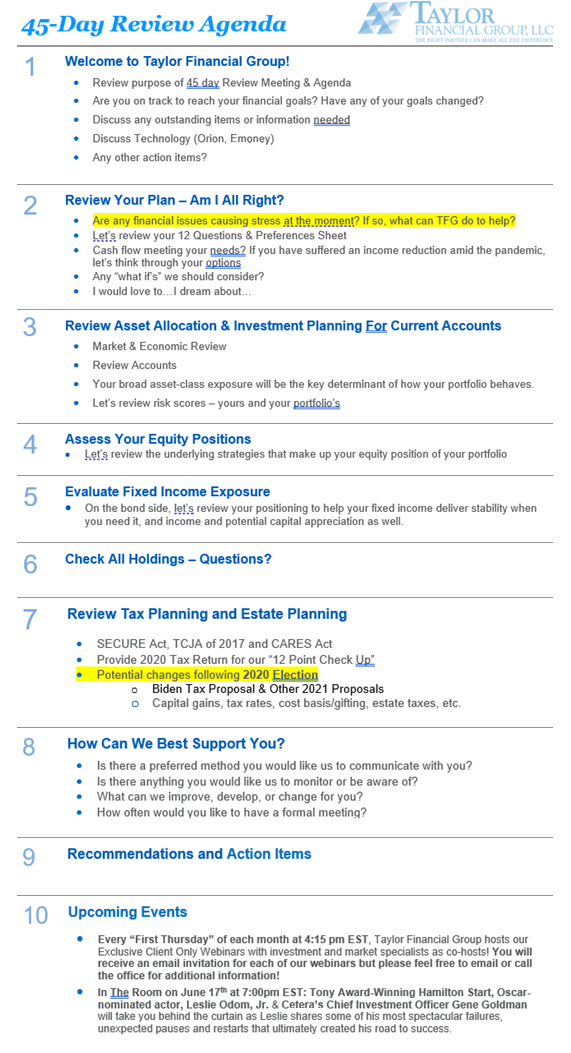

4. Provide a 45-day review appointment

Consider scheduling a 45-day review meeting for each new client that comes onboard. The 45-day review meeting should be the time you fully review the estate and financial plan with your clients, and to also identify your quick wins. (See our agenda for the 45-day review in Figure 5 below.) It also provides another opportunity to gain a deeper understanding of their needs for moving forward.

Discuss pain points during the review meeting—taxes being one of the biggest—and listen to your clients closely to ensure you are developing a plan that addresses all of their concerns. At the end of the meeting, clearly outline next steps for the client and when they can expect each item to be resolved.

Figure 5: TGF Agenda for the 45-Day Review

Source: Taylor Financial Group

5. Integrate new clients—treat them like family

Nothing builds trust like making someone feel like family. This may be where going beyond the requirement to what is “nice to have” really adds value to a relationship and goes a long way to engender trust.

I have older clients whom I see regularly and they often visit our offices for printing and scanning help. Of course, like most of our older community, they appreciate stopping in and sharing the details on their day. We will often drop documents off or hand-deliver paperwork for clients if that is their preference.

Within this older community of clients, there are those clients who aren’t tech savvy and require step-by-step instruction on a variety of issues. This may include anything from setting up a new email, to going to their homes to prepare their computers for a webinar or virtual review meeting, to hand-delivering wine for our virtual wine events! The way I look at it is: You can’t be trusted with the big things if you can’t help on the little things. All of this matters in creating a solid relationship.

Needless to say, this attention to detail requires organization and commitment from both you and your team. But, once that relationship is off to a great start, it will be difficult to lose your client’s respect. Following these five steps can help ensure a smooth onboarding process and lay the groundwork for a successful relationship for years (and decades) to come.