Losing a spouse is a difficult passage enough, but it can be more difficult for your clients if the proper financial steps are not taken in the year their spouse passes. Too often time passes and before you know it, some of the critical tax and planning strategies (that could save your widowed clients millions of dollars) are no longer available. Sometimes, even a few months can make the difference.

Below we highlight the top four actions that advisors need to immediately take when a client is widowed (as well as other considerations), with helpful tips and practice points.

1. Review step-up in basis of inherited assets

Spouses who are the beneficiaries of financial accounts (and other types of assets) are entitled to have their share of the account cost basis “stepped up” once the owner passes. This means that the current market value of the account becomes the new basis for the beneficiary, so they would not pay any taxes on gains if they immediately sell the assets in the account.

In the case of jointly owned accounts, 50% of the assets in that account would be stepped up. This often overlooked aspect of financial planning could save a widow thousands of dollars in future taxes.

It is important to note that the basis of assets in financial accounts is not always stepped up automatically, especially if spouses have different last names or the proper documentation is not provided to the client’s broker. As the advisor, it is your duty to review the cost basis of inherited assets and ensure that they are correctly stepped up.

-

Practice pointer: Don’t assume that this critical work has been done when onboarding new clients who happen to be widowed. Suppose you are working with a widow who is a current client or is coming from another advisor or broker. In that case, you must take immediate steps to request that the cost basis of any inherited accounts be stepped up accordingly. At Taylor Financial Group (TFG), this is one of the first items we address once a client becomes widowed.

Often, custodians require that the client sign a physical form before the assets are stepped up. Depending on how attentive the custodian is, it may take many follow-up emails and phone calls to get this done in a timely fashion.

2. File Form 706 and elect portability

And don’t forget state inheritance and estate taxes

When a spouse passes away, the surviving spouse can add the unused portion of the deceased’s estate tax exclusion amount to their own. The election to transfer a DSUE (deceased spousal unused exclusion) amount to a surviving spouse is known as the portability election. This can provide significant estate tax savings, especially if a couple’s combined estate is over $5 million.

In order to ensure that clients are taking advantage of this portability, it is crucial that you make them aware of the need to file an estate tax return (Form 706) if they wish to port their spouse’s exemption amount. It is crucial that this is done in a timely manner, as the deadline for filing form 706 is nine months after the decedent’s date of death. And while you are at it, confirm that state inheritance and estate taxes have been paid.

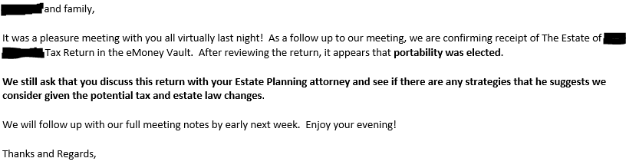

- Practice pointer: At TFG, we work closely with our widowed clients and their estate planning attorneys in order to ensure that Form 706 is filed and that portability is properly elected. Below is an example of an email we send to a widowed client after a review meeting confirming their portability selection and requesting that they follow up with their attorney:

Figure 1: TFG Email to Client Regarding Portability

Source: Taylor Financial Group

3. Widow must take deceased spouse’s RMD before year end

If an IRA owner dies after age 72, it is the responsibility of their surviving spouse to take their deceased spouse’s required minimum distribution (RMD) in the year of their death. Failing to do so results in a penalty of 50% of the RMD amount which should have been taken. It is important to note that if the widow is RMD age, they are required to take their own RMD as well, which can further add to the tax burden.

Of course, if both spouses are above RMD age and the widow decides to roll the IRA into her own accounts, it is important that she adjust the RMD amount to be based on her own life expectancy if she is younger. However, if the deceased spouse was younger, it would make sense for the widow to stay at their lower RMD rate.

A widow who is 70½ or older may also want to consider taking her own RMD as a QCD if she is charitably inclined. Depending on the client’s tax situation and deductions, she may be able to do a QCD of up to $100,000. These must go directly from an IRA to a qualified charitable organization. Performing a QCD will reduce the widow’s taxable income and save thousands of dollars, especially if she will be responsible for a large RMD from her deceased spouse.

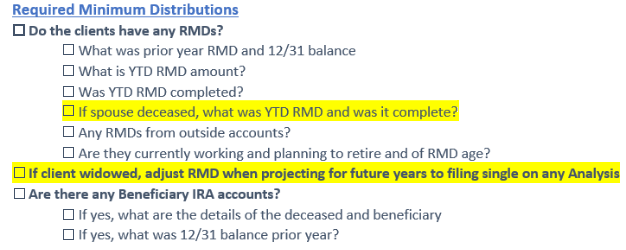

- Practice pointer: At TFG we use several checklists in order to make sure no steps are missed when clients need to take RMDs. These checklists also include specific bullets for widowed clients, as there are extra details that need to be addressed if their spouse did not take their RMD. Below is an example of a checklist we use frequently when working with widows.

Figure 2: TFG Checklist for Widows Regarding RMDs

Source: Taylor Financial Group

4. Notify Social Security

And review the impact of changing Social Security benefits

There are several changes to Social Security benefits that could impact a widow once their spouse passes. Many probably will not know this but any Social Security checks received for the month of the spouse’s death or afterward must be returned to the IRS, even if their death was on the last day of the month. To reiterate, the decedent must be alive for the entire month in order to keep the check. Additionally, a widow cannot collect both her and her spouse’s benefits. Therefore, once the spouse passes, the widow must notify the Social Security Administration and she will receive the higher of the two benefits.

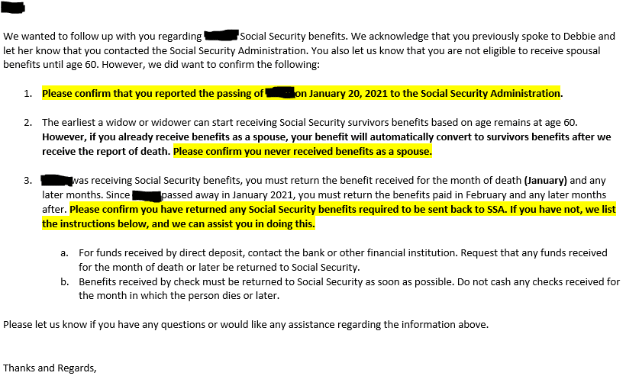

- Practice pointer: At TFG we provide our widowed clients with clear instructions regarding the rules for Social Security benefits after their spouse passes. In this example email below, we reiterate the actions that the client needs to take to ensure they properly report the passing of their spouse to SSA and return any spousal benefits back to them. It is crucial that you understand these rules as an advisor and make the client aware of them as soon as possible.

Figure 3: TFG Email to Clients Regarding Social Security issues

Source: Taylor Financial Group

Taking immediate action on these items will help ensure your newly widowed client is set up for the next phase of their financial life.