It is undeniable that inflation, which is at its highest rate in four decades, is showing up practically everywhere today, from wages to food to automobiles. The question is, however, whether inflation will be sticky and just represent a temporary phase for the economy, or whether advisors should be thinking differently and preparing portfolios and clients for a new normal. And if one chooses the latter, what are the best courses of action?

According to Barron’s, “for a generation of investors who rarely had to worry about inflation eroding their wealth, the past year’s spike marks a major change—and ought to prompt a reevaluation.” Here at Taylor Financial Group (TFG), we couldn’t agree more.

Here are some key moves to consider making now in your client portfolios.

1. Look for alternatives to core fixed income

If you haven’t already, now is the time to reassess any core bond holdings within client portfolios. Core bonds have already posted huge year-to-date losses, with many broad-based bond ETFs down 7%–8% so far this year.

And with rates continuing to increase, we believe these core bond funds will be under continued pressure moving forward. We moved clients out of core fixed income about a year ago in favor of a multisector approach that includes allocations to rate-sensitive sectors of fixed income such as bank loans, asset-back securities and short-duration bonds.

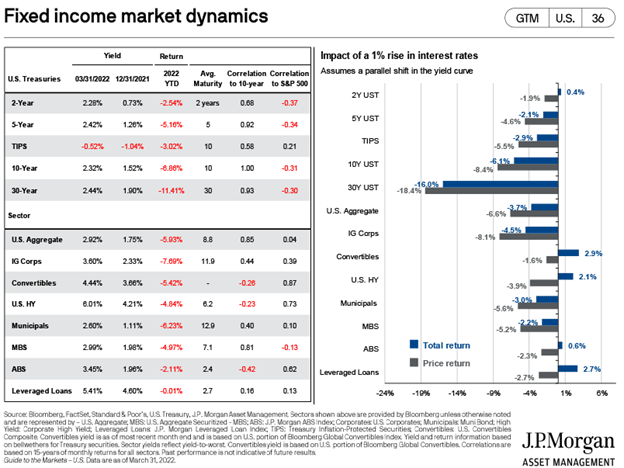

While you’re at it, we also recommend reviewing your municipal bond holdings and anything else with interest rate sensitivity. Figure 1, from JPMorgan Chase, demonstrates the loss to bond holdings when there is just a 1% increase in interest rates. Let that be your guide.

Figure 1: How 1% Increase in Interest Rate Affects Bond Holdings

Source: JPMorgan Chase

Is the 60/40 equity/fixed income portfolio dead?

Perhaps not entirely, but it certainly seems to be on life support. And for those clients who can withstand the volatility, the budget formerly committed to fixed income may be better allocated elsewhere. And for those who are still interested in bonds, it’s time to get creative. Consider inflation-protected, high-yield bonds or floating rate bonds.

We have used the Lord Abbett Credit Opportunities Fund (ticker: LCRDX) extensively within client portfolios to bring down duration and also provide active management, and we are thrilled with the returns and its approach. The fund invests in a broad range of fixed income and credit securities and has a duration of less than one year. So far this year, the fund has returned -1.8%. In contrast, the Barclays Aggregate Bond Index has a current duration of over 6.5 years and the index has returned -7.8% year to date.

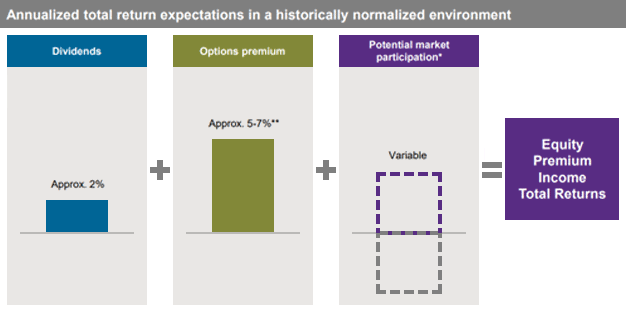

For clients who are searching for income, there are other possibilities, such as equity-based alternatives like the JPMorgan Premium Income Fund (ticker: JEPIX). The fund generates income through a combination of selling options (covered calls, a conservative options strategy) and investing in U.S. large-cap stocks, seeking to deliver a monthly income stream from associated option premiums and stock dividends. As shown in Figure 2, the fund aims to deliver 7%–9% in annual income from the options and dividends.

Figure 2: JEPIX Fund Aims for 7%–9% Annual Income

Source: JPMorgan Chase

The portfolio managers construct a diversified, low-volatility equity portfolio with the goal of delivering returns similar to the S&P 500 Index with less volatility, in addition to monthly income. This strategy has performed very well in the current environment, returning -0.4% year to date (S&P 500: -6.3%) and +13.8% over the past 12 months (S&P 500: +8.8%).

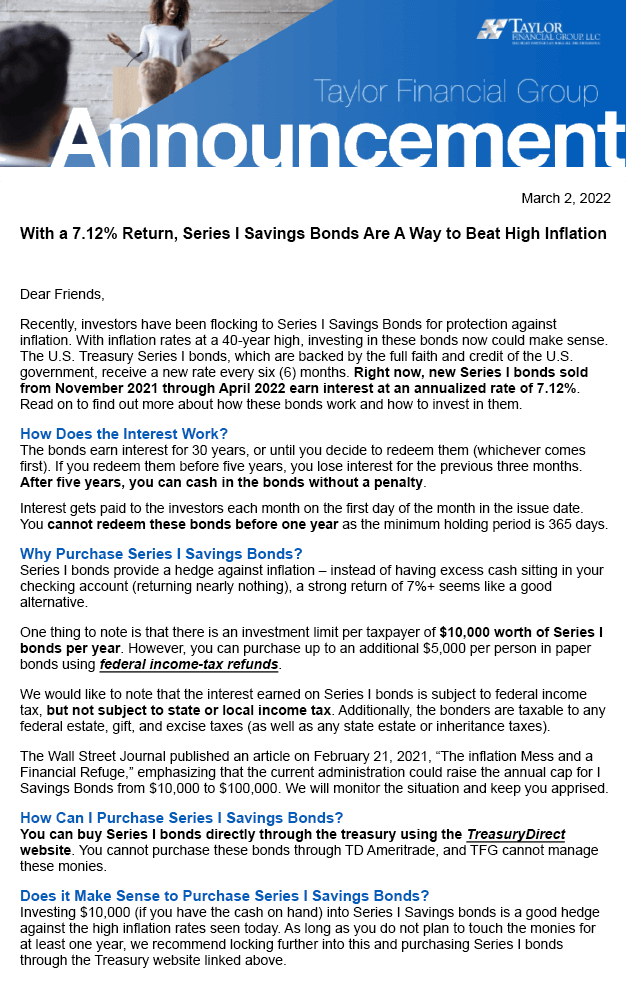

And as an aside, we recently reached out to clients with the iBond opportunity (see Figure 3), as they were yielding over 7%. Due to March’s CPI reading of 8.5%, iBonds will now offer annual interest payments of 9.6%.

Figure 3: TFG Alerting Clients to the iBond Opportunity

Source: Taylor Financial Group

2. Consider commodities and real assets

There are many ways to go here, so choose the real assets or commodities that can help protect against inflation, and start moving forward.

Commodities just had their best quarter in 30 years, rising 29%. These strong returns are a result of underinvestment, compounded by Covid and then the Ukraine war and Russian sanctions. Many of these forces will not subside soon, even if the war ends soon. Likewise, according to Barron’s, a shift towards electrification, digitalization and decarbonization adds to inflationary pressures.

At TFG, we own commodities now for the first time in over 10 years. We are using the Goldman Sachs Commodity Fund (ticker: GCCIX) as our primary commodity instrument. The fund invests in a basket of commodity futures that includes energy (oil & gas), metals (industrial & precious), and agriculture/livestock. We prefer to be diversified in this area as there is political/headline risk related to certain commodities that can be managed with diversification. The fund has returned +34% so far this year.

Other options you may want to consider are the DWS RREEF Real Assets Fund (AAAZX) and the PIMCO Inflation Response Multi-Asset Fund (PIRMX).

For others, they may prefer real assets or pipeline/MLPs, real estate or other tangible assets. That’s fine, as long as you have done your research and know what you are investing in. Make sure the investment does well in inflationary environments and that it makes sense for the client (older clients may require more inflation protection than younger clients, for example).

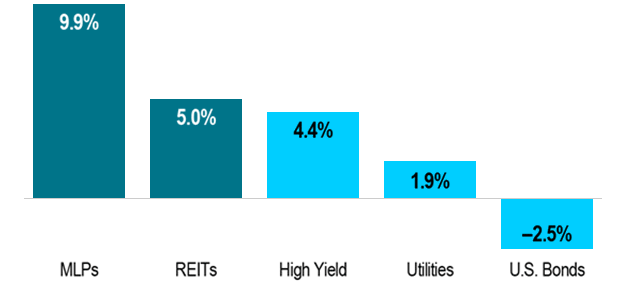

Figure 4 shows a chart from Prudential that illustrates how real assets have historically outperformed when treasury yields rise (increasing rate environments). This chart further demonstrates how real assets like MLP’s and real estate may be beneficial to consider for client portfolios.

Figure 4: Returns When 10-Year Treasury Yield Rose 50 Basis Points or More

Source: Prudential

3. Review stock portfolios to ensure holdings can perform well in an inflationary environment

And that downside protection exists for conservative clients

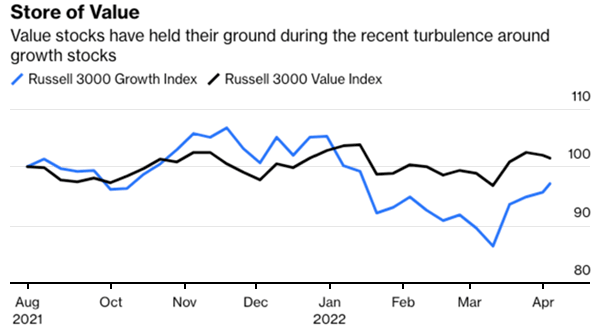

We recommend assessing every holding and asking yourself, “How will this investment perform under a high-inflation/high-interest rate environment?” For example, historical data indicates that value stocks often outperform growth in inflationary environments. Other data indicates that is not always the case, but that valuations are the most important factor regardless of classification. If the former is the case, is a rotation from high-flying technology companies in order?

Figure 5: Does Value Outperform in Inflationary Environments?

Source: Bloomberg

Note: Indexed to 100

What about the other holdings in the portfolio? Do they offer “wide moats” so that their revenue and profit margins are protected when the prices of inputs increase?

One strategy that we have used extensively for clients is the VanEck Morningstar Wide Moat ETF (ticker: MOAT). MOAT is a domestic equity ETF that leverages Morningstar Research to build a portfolio of quality companies trading at attractive valuations. About 50 wide-moat companies are selected for the ETF, and the holdings are reviewed and reconstructed quarterly, often to make room for companies whose prices have declined. Morningstar rates a wide moat to companies they deem to have a competitive advantage in their respective industry of 20+ years. Companies with wide moats are the pinnacle of quality and often have supreme network effects, brand recognition, and fortress balance sheets.

The ETF has outperformed the S&P 500 index over the year-to-date, 3-year and 5-year rolling periods, which is rare for an ETF that is so well-diversified (and not overweight in technology). MOAT also provides diversification by limiting the allocation to any single holding at 2.5% and limiting the allocation to any one sector at 20%.

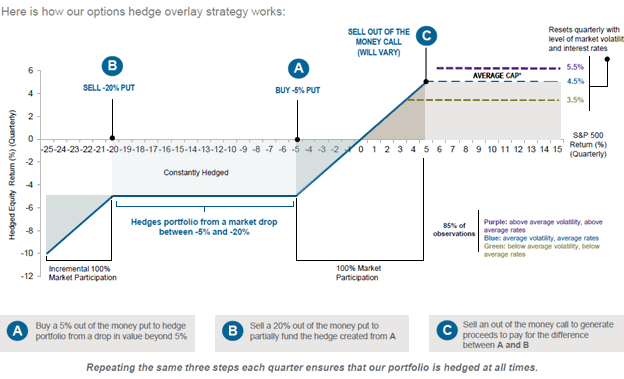

For your more conservative clients who are concerned about short-term volatility, how about some downside protection.After all, many clients are sitting on a decade of gains from the market and they don’t want all that money to be at risk, particularly if they are older or on a fixed income.

Hedged Equity is an excellent way to introduce downside protection into client portfolios while still participating in the equity market. The fund uses a low-volatility S&P 500 index as the equity base and then buys and sells options on top of the index in order to limit the downside.

Clients will participate in the first 5% of the market downside, but then clients are protected for the next 15% downside. Once there is a 20% fall, then clients are participating in 100% of the downside. These numbers reset every quarter.

To help fund the options set up to protect on the downside, the fund sells calls, which caps the upside performance to about +5% per quarter.

Figure 6 is a helpful chart showing the fund’s option strategy.

Figure 6: VanEck Wide Moat ETF Option Strategy

Source: Bloomberg

Note: Indexed to 100

Overall, we have found that hedged equity is an excellent alternative to the traditional “60/40” portfolio that provides long-only exposure and has also seen poor returns in fixed income due to the rising rate environment. There are other ways to potentially limit downside as well, such as structured products.

Whether you use some of these ideas or develop your own, the intention remains the same. With inflation at a 40-year high and likely to stick around for a while in some form or another, the savvy advisor needs to review all portfolios, considering how each investment can weather this most recent storm, and whether changes should be made.