The convenience of a single ticker has a price.

When investing in a prebuilt, multi-asset mutual fund the obvious advantage is convenience: exposure to a wide variety of asset classes with one purchase. But there is a serious drawback. There is no way to pull money out of the various asset classes within the single fund because there is only one NAV. Even though some of the components within the diversified mutual fund or ETF may be producing positive returns, the overall price (or NAV) may be in decline. If money needs to be withdrawn it may be at a loss even though some of the underlying ingredients of the fund were in positive territory.

There is a solution. Build a diversified, multi-asset portfolio à la carte (that is, using multiple funds and/or ETFs). By this method you achieve broad asset class exposure with multiple tickers—which translates to multiple “buckets” when money needs to be withdrawn. Each ticker has its own NAV. Money can be pulled out of a single fund or a couple of funds that comprise the overall portfolio. The fund or funds that are doing the best at that moment will be the ones that money is pulled from.

For the analysis that follows I’ve chosen three investments: Vanguard Balanced (VBIAX), Vanguard STAR (VGSTX) and the 7Twelve® model using 12 Vanguard funds. (I am the developer of the 7Twelve® Portfolio.) For sake of discussion I will refer to Vanguard Balanced and Vanguard STAR as comingled funds (meaning more than one asset class, but only one ticker) and the 7Twelve model using Vanguard funds as a separable model (meaning the funds used in the model are separate from each other).

3 approaches to diversification

- Two asset classes: Vanguard Balanced Index (VBIAX). The fund invests roughly 60% in stocks and 40% in bonds by tracking two indexes that represent broad barometers for the U.S. equity and U.S. taxable bond markets.

- Several asset classes: Vanguard STAR Fund (VGSTX). A balanced fund invested 60% in stocks and 40% in bonds. Exposure to 10 underlying actively managed Vanguard funds—including domestic and international stock funds and U.S. bond funds.

- 12 asset classes: 7Twelve® Portfolio using 12 separate Vanguard funds. Uses 8.33% allocation to 12 Vanguard funds covering the following asset classes: Large-cap U.S. stock, Mid-cap U.S. stock, Small-cap U.S. stock, Non-U.S. Developed stock, Non-U.S. Emerging stock, Real Estate, Natural Resources, Commodities, U.S. Aggregate Bonds, Inflation Protected Bonds, Non-U.S. Bonds, U.S. Money Market.

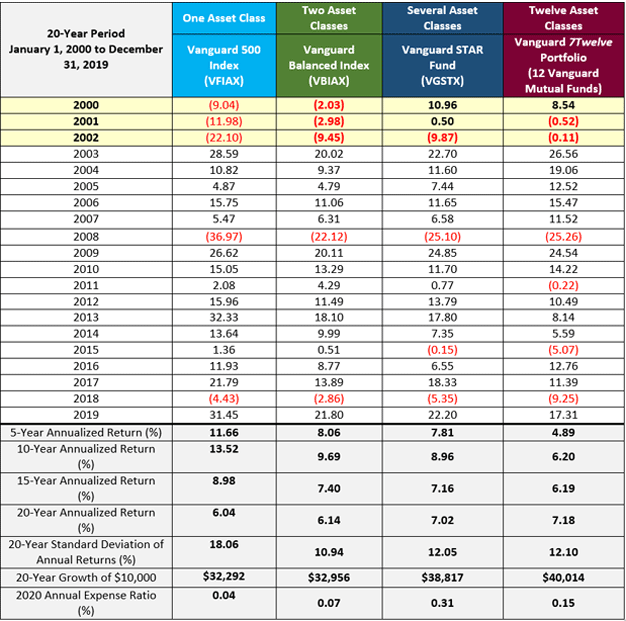

A summary of the year-to-year returns from 2000-2019 are provided in Table 1. Vanguard 500 Index (S&P 500 clone fund) is also included as a performance benchmark—even though it is a single asset-class investment.

The two comingled approaches (VBIAX and VGSTX) have produced better returns in recent years, but over the entire 20-year time frame the separable 7Twelve model produced the best performance. This is largely due to the performance in 2000, 2001 and 2002. These were years in which the U.S. equity experienced a protracted bear market. For example, the returns of Vanguard 500 Index (VFIAX) were grim. In 2000 it produced a return of -9.04%; 2001 was worse at -11.98%. Finally, 2002 saw a plunge of -22.10%.

Vanguard Balanced mirrored the losses of the U.S. equity market in all three years, though to a lesser degree. Vanguard STAR produced a positive return in 2000, a fractionally positive return in 2001, and a loss of almost 10% in 2002. The separable 7Twelve model also had a positive return in 2000, and then miniscule losses in 2001 and 2002. But this is only the macro view based on annual returns. The more interesting perspective is the monthly returns of the three investments during 2000, 2001 and 2002 (as shown in Table 2).

Table 1: 3 Approaches to Diversification (including Vanguard 500 Index as a performance benchmark)

Source: Craig Israelsen

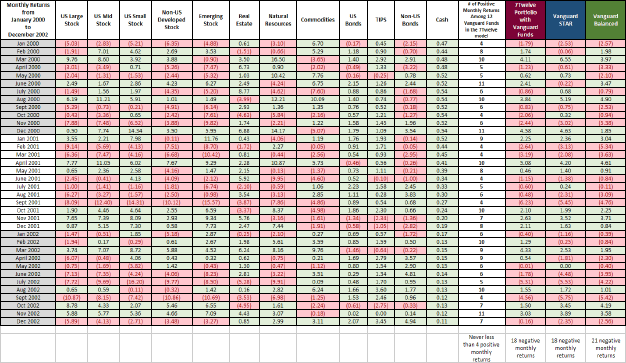

In Table 2 we observe that at least four of the 12 Vanguard funds in the 7Twelve model produced a positive monthly return over the 36 months from January 2000 to December 2002. On average, seven of the 12 funds had a positive return each month. Negative monthly returns are shaded in red, while positive monthly returns are in green. As an entire portfolio, the 7Twelve model produced positive returns in 18 of the 36 months from 2000-2002. The Vanguard STAR fund also produced 18 positive returns over the 36-month period. Vanguard Balanced had 21 negative monthly returns. (Click here to reach a larger version of Table 2.)

Table 2: Monthly Returns for the 12 funds in the Vanguard 7Twelve® Model (by asset class)

Source: Craig Israelsen

Look at January 2000. Among the 12 Vanguard funds in the 7Twelve model, four had a positive return for the month: real estate, commodities, TIPS, and cash even though the 7Twelve model as a whole had a return of -1.79%. In that same month, Vanguard STAR had a return of -2.53%, and Vanguard Balanced had a return of -2.57%.

If an investor needed to withdraw money from Vanguard STAR or Vanguard Balanced they would have done so at a loss for that particular month. By contrast, if the investor had their money invested across 12 different Vanguard funds in the 7Twelve model, they could have made withdrawals from any (or all) of the four funds that had a positive return that month. This “separability” is the distinct advantage of building a diversified portfolio using multiple mutual funds and/or ETFs.

Another example would be the month of April 2002. The 7Twelve model had a return of 0.54%, whereas the STAR fund and the Balanced fund both had losses. Nine of the 12 Vanguard funds in the 7Twelve model had positive returns, so if money needed to be withdrawn there were nine “buckets” of money that had positive returns that month.

Clearly, money would not have been withdrawn from large-cap U.S. stock, mid-cap stock, or natural resources (based on their negative returns during that month). Despite their level of diversification, there was no way to withdraw money from the portions of the Vanguard STAR fund or the Vanguard Balanced fund that had produced a positive return in April 2002 because of the comingled nature of their holdings.

Understandably, in a separable portfolio we may not withdraw money from a particular fund simply on the basis of a positive one-month return. The withdrawal may be based on the YTD return, 1-year return, etc. The point is simply that a portfolio with diverse—and separate—funds provides choices when money needs to be withdrawn. There will always be a best choice of where to withdraw money from in a separable portfolio, whereas with a single ticker fund there will only be one choice.

To support this point, I analyzed the monthly returns of the 7Twelve model using 12 Vanguard funds over a 22-year period from January 1998 to December 2019. That time frame represents 264 months. On average, eight out of the 12 funds produced a positive monthly return. Interestingly, the mode was nine funds with a positive monthly return. There was never a month where all 12 funds had a negative return.

As we build separable portfolios, we create the ability to withdraw money from (or add money to) the individual components. The convenience of a single-ticker is attractive, but the comingled nature of the one-ticker diversification is a serious drawback.