Baby boomers should be protecting their savings at this critical time in their lives, as they transition through the Risk Zone (the five to ten years before and after retirement). They can protect by holding a portfolio of protective assets or they can hire someone to provide an assured income stream in retirement, just as defined benefit pension plans deliver.

In other words, baby boomers can pay someone to take over the risk, to guarantee against losses, which is the role of an insurance company. But non-insurance companies also provide risk mitigation. In this article (and this video) we discuss annuities and other risk mitigation choices.

In the 1980s, a protection approach called “portfolio insurance” became very popular, with tens of billions invested. The idea is straightforward. We insure our cars and our homes, so why not our investments?

But this idea fell into disrepute in October 1987 when it caused a market crash. The implementation of portfolio insurance was to synthesize a put option. The problem in 1987 was that too many people were trying to sell at the same time in order to execute the replication. By contrast, those who actually owned put options did not lose money; they profited from the crash.

The moral of this story is that real portfolio insurance can be purchased, and it is easy—just buy put options. Most people are afraid of options because they don’t understand them, so here we will talk about handing over assets to others who will generally use options and other techniques to limit your risks.

Annuities

Annuities come in three forms: fixed, indexed and variable. A fixed annuity pays the promised amount over time; it is the benefit in a defined benefit pension plan. An indexed annuity makes variable payments based on the performance of a securities index. And variable annuity’s payments are based on the performance of the insurance company’s assets. The following discussion is primarily about fixed annuities. Annuities are provided by companies that sponsor defined benefit pension plans and by insurance companies. Many pension plans hire insurance companies to make their annuity payments.

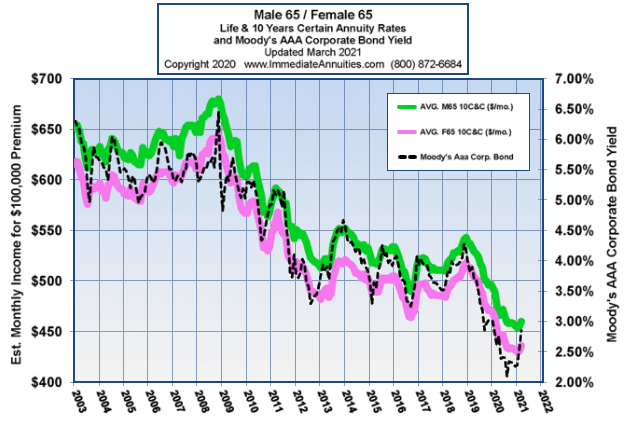

The common question about annuities is whether they are investments or insurance. They’re both. As an investment, annuities actually tend to pay more than a safe investment in high quality corporate bonds, as shown in the following:

Figure 1: History of Fixed Annuity Rates

Source: Ron Surz

As you can see, policies for males (in green) pay more than those for females (in pink), because males have a shorter life expectancy. The rates for males have always been above the return on AAA corporate bonds, while the rates for females have been roughly equal to the AAA rate. Insurance companies can pay more because they earn a “mortality credit” for pooling a lot of people together in a single policy—some will live long lives, and some will not.

The problem recently has been that interest rates are artificially low under the Fed’s Zero Interest Rate Policy (ZIRP), so most people do not want to lock in their savings at this time. There’s a good chance that annuity purchases will perk up when interest rates increase.

As insurance, annuities serve the beneficial purpose of diversifying mortality risk. They are similar to the tontines discussed below.

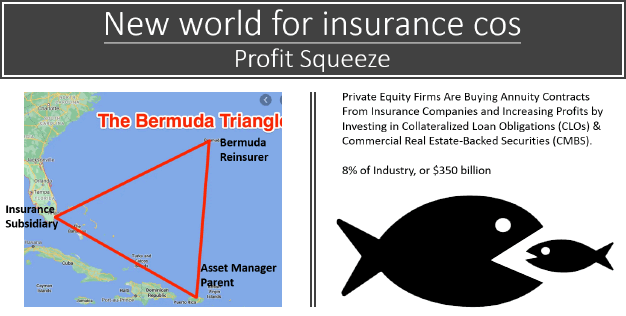

Low interest rates create challenges for insurance companies too: namely, it’s hard to make a profit. As a result, private equity companies are buying annuity contracts from insurance companies who want them off their books. These private equity firms are increasing profits by employing a strategy that Kerry Pechter, publisher of the Retirement Income Journal, calls the “Bermuda Triangle” for reasons shown in Figure 2 and explained below:

Figure 2: The Bermuda Triangle of Annuities

Source: Ron Surz

Private equity companies employ a two-pronged approach: operating efficiencies are gained by the triangle shown above, and investment returns are increased by taking more risk, investing in Collateralized Loan Obligations (CLOs) and Commercial Real-Estate-Backed Securities (CMBS). The “Triangle” works as follows:

- The private equity company manages the assets and creates an

- Insurance subsidiary that manages the insurance contracts and a

- Bermuda reinsurance company operates off-shore with less stringent requirements

Consequently, if you own an annuity, it would be good to know who is insuring your payouts currently.

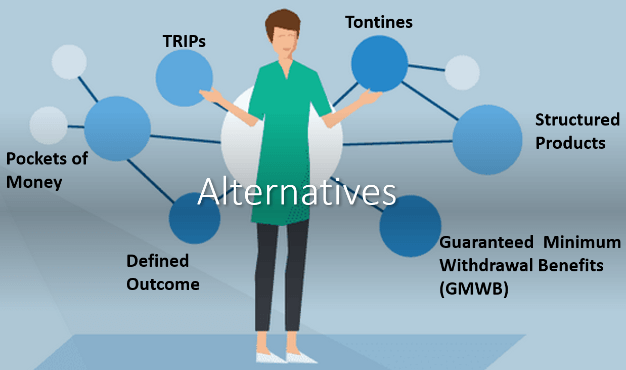

The rest of this article discusses risk mitigation that is provided by both insurance companies as well as non-insurance.

Figure 3: Risk Mitigation Options Through Insurance and Non-Insurance

Source: Ron Surz

Guarantees against loss

Insurance companies provide “guaranteed investment contracts” or GICs that compete with Treasury bills by providing income while guaranteeing that market value will not decline.

Non-insurance companies compete with what is called “stable value” that uses complex accounting and “wrappers” to maintain constant value.

These are generally available only to institutions like pension plans and 401(k) plans. In order to compete with Treasury bills they need to deliver higher returns that are sought by taking a little more risk.

Structured products

Creative uses of derivatives like options and futures are used to create attractive payoffs. A guaranteed equity management (GEM) is an example that promises 120% of the return on the S&P 500 or your money back if the S&P declines in value.

Most structured products only work when interest rates are reasonably high, so there aren’t many in the low interest environment of 2021.

Guaranteed minimum withdrawal benefit (GMWB)

Insurance companies sell riders to their variable annuities that allow the annuitant to withdraw a minimum amount each year even if it exceeds the normal variable payout.

Non-insurance companies financially engineer a similar structure that can be viewed as a promised payout with an occasional bonus when assets perform well.

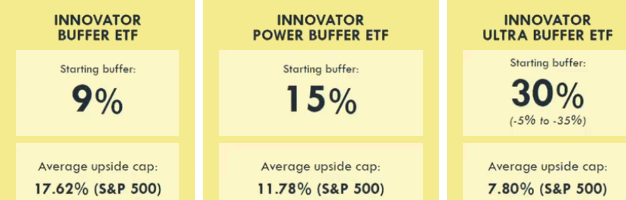

Defined outcome exchange traded funds

“Innovator exchange traded funds” (ETFs) have entered the field of “shape shifting” returning payoffs by using options. The following example places “guardrails” around annual return. The investor loses nothing if the S&P declines as much as the indicated “starting buffer” but participates in losses below that amount. Part of the cost of the protection is a limited upside, specified as “average upside cap.” The actual upside participation is unknown before the fact.

Figure 4: ETFs May Establish a Starter Buffer

Source: Ron Surz

Other variants include amplified ETFs that capture multiples of the upside and downside.

Tontines

Italian banker Lorenzo de Tonti created the first tontine in 1670, and it went on to become extremely popular among the rich in France in the 1700s and 1800s. Banks sponsored a “club” of investors who pooled their investments. As contributors died, their share of the assets and the income was credited to the survivors, with the last survivor taking all. That way, participants were guaranteed an income stream for life, solving the longevity challenge, and those who died didn’t care.

Formal tontines are unpopular today, but the structure lives on with people who move in together, like the T.V. series the Golden Girls, with the intention of lifetime support. Continuing Care Retirement Communities (CCRCs) are another example of a tontine-like structure. CCRCs bring residents from independent housing to on-site hospitalized nursing care to death, all paid by the community.

Pockets of money

For those who have more than they’ll spend in their lifetime, it is good to know that your money will do everything you want it to do. This approach starts with a forecast of what you want to spend and when you want to spend it. Then zero coupon Treasury Inflation-Protected Securities (TIPS) are purchased that will mature to satisfy each future payment. Whatever is left over can be reserved for future adjustments and whatever else you like. This is asset-liability matching, a technique sometimes used in defined benefit pension plans.

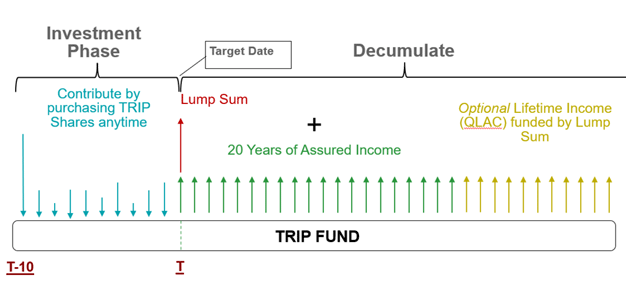

Target Retirement Income Plus (TRIP)

Another application of financial engineering generates a promised payment stream, like an annuity, but without locking in the contributed assets. It’s like pockets of money where each pocket is the same dollar amount. One unit of a TRIP provides one dollar of future payments per year for 20 years plus a kicker at the end of 20 years to create a sort of deferred annuity. The cost of a TRIP unit varies with the level of interest rates, becoming less expensive when interest rates rise. A unit cost $17 when 10-year Treasuries yielded 1.5%.

Figure 5: Target Retirement Income Plus 1 unit of a TRIP buys $1 per year in retirement

Source: Ron Surz

Conclusion

Many like the assurances of annuities but are waiting for interest rates to return to more normal levels. In the meantime, there are other risk mitigators that do not require locking up your investment, although these too will work better when interest rates return to normal.