With the equity markets at record highs, bond yields low, and the Fed signaling that it will raise rates, many experts predict that we will see lower returns in the years ahead. JPMorgan estimates that over the next decade, a traditional 60/40 stock/bond portfolio will only return around 4.2% per year.

Additionally, if the Fed decided to rapidly raise rates, large-cap growth stocks (which have contributed to a majority of the S&P 500’s returns this year and are highly represented in many client portfolios) could face an even greater headwind. When interest rates rise, growth stocks could be negatively affected because their future earnings are more heavily discounted to the present.

With stocks at all-time highs, some clients may be feeling nervous about 2022. Below, we will discuss how to position clients’ portfolios, and how to effectively communicate the reasoning for your asset allocation and market outlook to your clients during this uncertain time with helpful communication tips.

1. ‘Be active and diversify!’

In a recent announcement, Goldman Sachs stated that within U.S. equities, the average portfolio remains underallocated to U.S. small caps, and that daily liquid alternatives are heavily underutilized in portfolios. They estimate that allocations to liquid alternatives, which have similar characteristics to hedge funds, have been cut in half over the last five years making up just 2.5% of portfolio allocations on average in 2021.

In addition to this, they believe that core equity (defined as U.S. equities at all market cap levels, plus developed country large-caps) drives around 78% of portfolio risk, with the top five companies in the S&P 500 representing almost 25% of the index. (Goldman Sachs Asset Management)

In the face of these challenges, consider diversifying client portfolios beyond the typical 60/40 allocation by using liquid alternative investments with non-correlated returns in order to reduce risk and pick up returns in other areas.

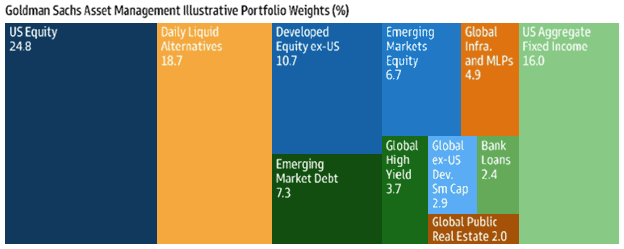

Figure 1 shows a graphic from Goldman Sachs that illustrates their latest thoughts on portfolio construction. Each colored panel below represents a different asset-class weighting. Goldman Sachs recommends that in the current low-interest rate environment, we need to be utilizing new alternatives to traditional 60/40 allocations such as private debt, hedged equity and bank loans.

Figure 1: Diversifying to Boost Yields

Source: Goldman Sachs Asset Management

Note that Goldman Sachs’ model portfolio includes an 18.7% allocation to daily liquid alternatives (like hedged equity), a combined 11% allocation to emerging market debt and global high-yield bonds, and a 2.4% allocation to bank loans. They also suggest diversifying equity exposure outside of the U.S. into regions such as developed Europe (10.7%) and emerging markets (6.7%), which have previously lagged domestic indexes. These equity and debt strategies could potentially boost returns in this current low-yield environment.

2. Position client portfolios for rising interest rates

At TFG, instead of relying on traditional fixed income and Treasuries, which have struggled in 2021 due to low interest rates, we have focused on private credit and distressed debt. One fund that has provided strong returns in our models has been the Lord Abbett Credit Opportunities Fund (LCRDX), returning +12.7% year-to-date through December 16, 2021. It is unique in that it is an interval fund that invests in a variety of high-yield corporate credit securities and corporate mortgage-backed securities. The interval structure enables this fund to take advantage of opportunities in the credit markets that daily-liquid funds would not be able to access. Some clients may object to this feature, but it enables the fund to garner strong returns.

Another strategy we employ in an attempt to limit downside is using daily liquid alternatives (DLA), such as hedged equity. Hedged equity employs some of the techniques used by hedge funds to provide investors downside protection while also participating in market gains. The fund we favor is the JPMorgan Hedged Equity I Fund (JHEQX), which returned +13% year-to-date (through 12/16/2021). The fund seeks to provide a majority of the S&P 500 Index’s returns with less volatility and less downside. It invests in a portfolio of U.S. large-cap stocks while employing a disciplined options strategy that resets every three months and seeks to reduce downside risk in falling markets by providing a consistent downside hedge.

The fund fully participates in the first -5% market drop, hedges the portfolio from a market drop of between -5% and -20%, and then has 100% market participation below a -20% market drop. For example, if the market dropped -22% during the quarterly period, the fund should be down approximately -7% at the end of the quarterly period. The average market upside per quarter is capped at about 4.5% as the proceeds of selling an option that caps the upside are used to purchase the options designed to provide downside protection.

And although international and emerging markets have been a disappointment compared to the domestic markets, JPM and GSAM both recommend Europe and selective emerging markets for 2022, as they are both generally trading at significant discounts relative to U.S. stocks. Both banks are particularly focused on Europe, where they see great opportunity. We use Goldman Sachs GQG Partners International Opportunities Fund (GSIMX), which has returned +9.9% year-to-date (as of 12/16/2021) and has the ability to go anywhere around the globe.

3. What are skyrocketing valuations telling us?

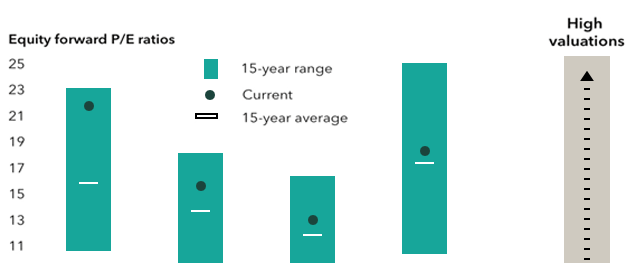

Figure 2 shows the relative valuations of U.S. stocks, as well as developed international and emerging markets stocks (as of November 30, 2021). As we can see, valuations (the blue dots) are above their 15-year averages for all five categories represented by the white lines. This is especially true of the S&P 500, where current valuations are nearing the top of the 15-year range at about 22 times forward earnings. The green bars represent the 15-year range of the forward P/E ratios—another reason to be open to equities outside of the S&P 500.

Figure 2: Stock Valuations Are Above Their 15-year Averages

Source: Bloomberg Index Services Ltd., IBES, JPMorgan, MSCI, Refinitiv Datastream, RIMES, Standard & Poor’s

But even the high overall valuation of the S&P 500 does not mean that there are no opportunities to exploit within the index. It is important to remember that there are a handful of mega-cap stocks that contribute to the above-valuation metric more than most, with 25% of the S&P 500 Index returns from 2021 attributed to just five companies. Some experts, like Dr. Jeremy Siegel, believe that there are many areas of the U.S. stock market that may even be undervalued and that this is where investors should look to in 2022.

According to Financial Advisor, Siegel notes that if you remove the FAANG stocks plus Microsoft from the U.S. Indexes, the P/E ratio of the S&P 500 falls from 22 to 19—much cheaper than with the big tech names. Siegel also notes that portfolios that are overweight with long-duration tech stocks could be hurt by rising interest rates and that investors should be switching their strategies toward dividend-paying value stocks. (Evan Simonoff, FA)

With growth possibly slowing going into 2022, putting “quality” first is more important now than ever. Another fund to consider in this post-peak growth environment is the VanEck Morningstar Wide Moat ETF (MOAT). Based on the concept of “moat” investing, a term coined by Warren Buffett, this ETF invests in 50 companies that are determined to possess sustainable competitive advantages, or “wide moats,” and that are also trading at attractive valuations. This fund is generally underweight some of the big FAANG stocks and is usually overweight toward health care. The fund managers use a proprietary discounted cash flow model in order to ensure that stocks selected for the fund represent “good value.” Year to date, through December 16, 2021, MOAT has returned 22.5%.

4. How to communicate with clients right now

With Fed policy and market conditions rapidly changing, it is crucial that your clients understand what is happening in the markets and what you are doing to ensure they are properly positioned. At Taylor Financial Group, we send out “Weekly Client Updates” and frequent “Client Announcements” detailing our latest views so clients know what to expect and to reassure them that we are tirelessly working on their behalf. Figure 3 shows a recent piece addressing portfolio construction in the wake of richly valued equity markets and the rising interest rate environment.

Figure 3: Keep in Touch With Clients to Demonstrate Your Value

Source: Taylor Financial Group

In addition to sending written updates, we also employ a variety of messaging strategies, such as short two-minute videos and our quarterly webinars. Figure 4 shows an invitation to our first quarterly webinar of the year, where we share our current market outlook and strategy. Offering this kind of ongoing communication keeps clients engaged. Of course, we also make sure to address these items in our regular review meetings, and we include talking points on our agendas.

Figure 4: Engaging Clients by Sharing Exclusive Content

Source: Taylor Financial Group

One thing we know for sure, easy money is a thing of the past. Only time will tell how the markets react to these unprecedented changes. In the meantime, your clients will appreciate your thoughtfulness and skills in navigating these choppy waters.