In today’s complex tax environment, tax-bracket management is a valuable tool for wealth enhancement. Bracket management relates to shifting income, where possible, into different tax years and different tax brackets, thereby reducing the client’s overall tax burden over a period of time.

Bracket management can have a significant impact for someone at or nearing retirement, or for a taxpayer with a significant change in income. Examples of items that can materially change income include starting Social Security, beginning IRA distributions, bonus payouts, severance payouts, exercising stock options, or sale of a business. The investment advisor who has ongoing communication with the client throughout the year often is in the best position to recognize these opportunities. This is especially important because by the time tax returns are completed, it’s likely too late to make meaningful shifts in taxable income.

Tax system overview

The tax system is multifaceted and complex. Aspects of the federal tax system include the following:

- Traditional income-tax brackets

- New in 2013, a 39.6% “supertax” income-tax bracket for high-income taxpayers (which also applies for short-term capital gains)

- The alternative minimum tax system (AMT)

- 0%, 15%, and now 20% long-term capital gains rates

- 3.8% tax on net investment income above certain thresholds

- 0.9% Medicare tax on wages and self-employment income above applicable thresholds

- Personal exemption phase-outs (“PEP” limitations)

- Limits on itemized deductions for high-income earners (“Pease” limitations, named after former U.S. Rep. Donald Pease)

- Various tax rates and deductions for trusts and estates

This layered system has created an environment where meaningful tax management is possible.

Knowing the rules

Before explaining the strategies, it is first necessary to know the rules. To effectively implement bracket management, the advisor must have a working knowledge of key concepts of the current tax system. Armed with this knowledge, the advisor can proceed to recommend strategies to help enhance the after-tax wealth of the client.

Five essential facets will be reviewed here. The intent is not to become an expert in each of these topics, but rather to have a basic knowledge of the applicable tax layers. At a minimum, this will enable the advisor to recognize when opportunities may exist for further exploration. The five facets of the tax system discussed are the following:

- Current ordinary income-tax brackets

- Capital gains tax rates

- The net investment income tax

- Personal exemption and itemized deduction phase-outs

- The alternative minimum tax

1. Current tax brackets

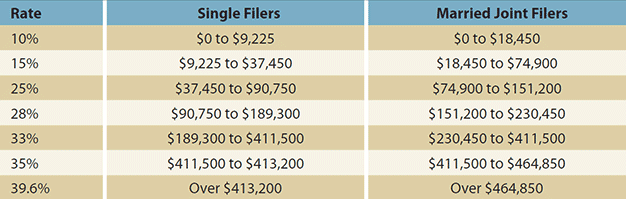

The first facet covers understanding current tax brackets and at what income levels they are triggered. These brackets are indexed each year for inflation. Table 1 shows the various rates and thresholds for 2015.

Table 1: 2015 Ordinary Income Tax Rates (Based on Taxable Income Levels)

Source: IMCA

2. Capital gains tax rates

The next important aspect is the capital gains tax rates and taxes on qualified dividends. Short-term capital gains are taxed at ordinary income-tax rates. Long-term capital gains are based on the taxpayer’s income level. If the taxpayer’s ordinary income rate falls in the 10% or 15% bracket, then the long-term capital gains rate is 0%. If income falls in either the 25%, 28%, or 35% brackets, then the long-term capital gains rate is 15%. If the taxpayer is in the 39.6% marginal bracket, the capital gains rate is 20%. Table 2 provides a summary of long-term capital gains rates.

Table 2: 2015 Capital Gains Tax Rates (Based on Taxable Income Levels)

Source: IMCA

Note that the long-term capital gains rates are graduated, meaning that if a recognized capital gain causes ordinary taxable income to cross into the next bracket, the portion of the gain below the higher bracket would be taxed at the lower capital gains rate.

3. Net investment income tax

The net investment income tax (NIIT) consists of a 3.8% surtax calculated as 3.8% of the lesser of (1) net investment income or (2) modified adjusted gross income above $200,000 for a single taxpayer ($250,000 for married filing jointly). Investment income for purposes of the surtax includes interest, dividends, capital gains, annuities, rents, royalties, and passive activity income.

As an example, suppose a single taxpayer has modified adjusted gross income of $300,000. Further, suppose the taxpayer’s net investment income is $50,000. In this example, the taxpayer would be subject to an additional $1,900 of tax. This is calculated as 3.8% of $50,000. In this case, $50,000 of net investment income is used because it is less than the modified adjusted gross income of $300,000 minus the threshold of $200,000 (in other words, compare $50,000 versus $100,000 to determine the base to apply the 3.8% tax).

4. Personal exemption and itemized deduction phase-outs

Taxpayers are also subject to an exemption and itemized deduction phase-out, commonly referred to as the PEP and Pease limitations, respectively. The threshold for which these phase-outs begin is $258,250 of adjusted gross income for a single taxpayer and $309,900 for married filing jointly.

The PEP phase-out reduces exemptions for both taxpayers and their dependents by 2% for each $2,500 that adjusted gross income exceeds the threshold. Note that for 2015, the personal exemption is $4,000 per individual.

The Pease phase-out causes certain itemized deductions to be lowered by 3% of the amount by which the taxpayer’s adjusted gross income exceeds the threshold amount, with the reduction not to exceed 80% of the otherwise allowable itemized deductions. Thus, a taxpayer who is subject to the full phase-out still gets to deduct 20% of the deductions subject to the phase-out.

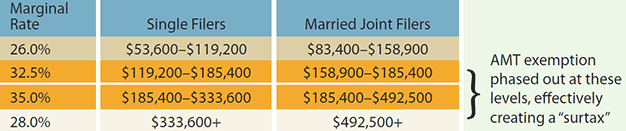

5. Alternative minimum tax

The alternative minimum tax (AMT) is essentially a simpler tax system that exists in addition to the regular tax system. The AMT is calculated by adding income, subtracting a few allowable deductions, subtracting one large AMT exemption amount, and applying one of two tax rates—26% on the first $185,400 and 28% on the remainder. The taxpayer compares regular tax to AMT tax and pays the higher amount.

Perhaps one of the most important nuances of the AMT is the phase-out of the large AMT exemption. For a single individual, the AMT exemption amount is $53,600 but is reduced once income reaches $119,200. For married filing jointly, the AMT exemption is $83,400 but begins to be phased-out at $158,900 of income. Once income reaches the phase-out levels, the AMT exemption is reduced by 25 cents for each additional dollar of income over the phase-out amount, until the exemption is completely eliminated.

For example, suppose a married couple has AMT income that is $20,000 higher than the phase-out of $158,900. The couple will then see their AMT exemption reduced by $5,000 (calculated as $20,000 x 0.25). Therefore, the AMT exemption would be reduced from $83,400 to $78,400.

Understanding AMT phase-out levels is important because they effectively create an additional tax and temporarily create two other marginal levels of AMT tax for each additional dollar of income—beyond the 26% or 28% to 32.5% and 35%, until returning back to the 28% AMT level once the exemption is totally phased-out.

This creates a unique situation in which each dollar of additional income in the middle of AMT is actually subject to a higher tax than each additional dollar of income at the end of AMT. Notice in Table 3 the effective marginal rates for taxpayers subject to AMT actually increase before declining back to 28% (see highlighted rows).

Table 3: 2015 AMT Effective Marginal Rates (Based on Income Levels)

Source: IMCA

If income continues to increase to very high levels, the taxpayer ultimately will return to the regular tax rates, which eventually become higher than AMT rates (for instance, the 39.6% regular tax rate).

Strategies

At this point, the reader is likely to acknowledge the complexity of the tax system. What is important for advisors to understand is that the federal tax system is multilayered and multidimensional. The key point is not the need to become an expert in each of these tax areas, but to recognize when planning opportunities may present themselves, especially when income changes dramatically from one year to the next. Retirees or near-retirees often are subject to changes in income and have opportunity for planning, and advisors need to be on the forefront of material changes in the client’s income situation.

Generally, the advisor wants to simply keep as many dollars as possible out of higher effective marginal tax rates. This can be accomplished by:

- Frontloading income

- Deferring income

- Frontloading credits and deductions

- Deferring credits and deductions

Some examples of items that can be frontloaded or deferred include retirement start date, Social Security start date, capital gains (or losses), exercise of employee stock options, gains from the sale of property, gains on the sale of a business, Roth conversions, state tax payments, and medical payments.

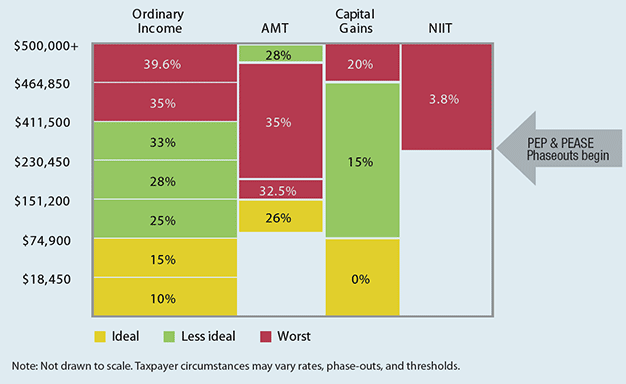

Table 4 shows the effective marginal rates and phase-out levels for a married taxpayer filing jointly. This is an important visualization because it provides a picture of how the various layers of tax coincide, based on income levels. The basic strategy is to avoid, to the extent possible, those areas of higher marginal tax rates. Those areas highlighted in red denote the rates that ideally should be avoided.

Table 4: Effective Marginal Rates of Various Tax Dimensions for Married Filing Jointly

Source: IMCA

Case studies

The following case studies are examples of real client situations. These provide a demonstration of the power of bracket management. The reader will notice that each of these situations arose from a client going through a transition—sale of a business, beginning IRA distributions, or retirement of a spouse. It is during transitions that the advisor must be keenly aware of tax savings opportunities.

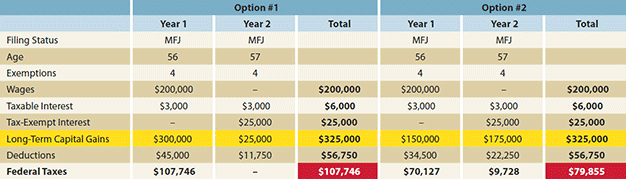

First case study: capital gains deferral

The client is 56 years old, married, with two dependent children, selling a business, recognizing $300,000 of capital gains from the sale, then living off his investment portfolio. Option one would have the taxpayer recognize the entire capital gain on the sale of the business in year one.

However, suppose it is late in the year and the client is able to structure a deal that would allow him to receive one-half of the payment in year one and one-half of the payment in year two. In essence, he has deferred the capital gain. Over the two-year period, his total income and deductions have not changed. Yet, by structuring the deal over two years, he is able to reduce his total taxes from $107,746 to $79,855 (see Table 5)—a savings of nearly $28,000.

Table 5: Example of Capital Gains Deferral

Source: IMCA

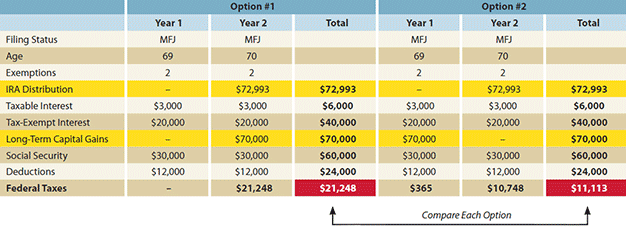

Second case study: capital gains recognition

Instead of deferring capital gains, it is sometimes worthwhile to recognize capital gains. This is especially true if the taxpayer is in the 0% capital-gains rate and may be entering a higher-tax-bracket at a later date. We often see this with someone who will be starting required minimum distributions (RMDs).

For instance, suppose a client has a $2 million IRA and will begin taking RMDs next year. The client is married, living primarily off Social Security and a municipal bond portfolio, has a large unrealized capital gain of $70,000 in a taxable account, and would like to begin unwinding the position. Often the inclination is to defer capital gains as long as possible. However, as shown in Table 6, this taxpayer is better off recognizing the gain before beginning the RMD. Total taxes over the two-year period are reduced from $21,248 to $11,113, for a 48% savings.

Table 6: Example of Capital Gains Harvesting

Source: IMCA

For those clients in the 0% capital gains bracket, recognizing gains is often a worthwhile strategy. In fact, the taxpayer could recognize a gain and immediately rebuy the security, thereby setting the cost basis at a higher level. (Wash-sale rules do not apply on the recognition of gains.)

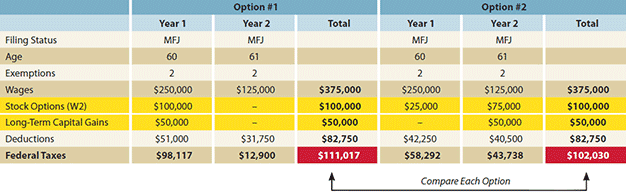

Third case study: income smoothing with stock options

Consider a couple with one spouse who wants to retire and the other spouse who would like to continue to work. Suppose each spouse earns $125,000. After one spouse retires, the couple’s wage income will be cut in half. In anticipation of the loss of income, the couple wanted to sell $100,000 of nonqualified stock options and also recognize $50,000 of capital gain, thereby locking in some cash reserves.

Table 7 shows this example as Option One, resulting in a total tax of $111,017. However, analysis reveals they would be better served by smoothing their income over the two years, exercising the majority of the nonqualified stock options in year two, and recognizing the $50,000 capital gain in the second year as well. This reduces their multiyear tax by $8,987 to $102,030 (Option Two), or an 8% savings. Timing the exercise of nonqualified stock options often can be a helpful tax strategy.

Table 7: Example of Income Smoothing with Stock Options

Source: IMCA

Other considerations

The above case studies are a few examples of possible bracket management. Other strategies include Roth IRA conversions, management of credits, and timing of deductions. Each situation presents a unique opportunity.

Also, it is important for the advisor to always keep in mind the current estate-planning rules. Especially noteworthy is the step-up in cost basis received at the death of a taxpayer. For taxpayers in failing health, it may not be worthwhile to advance income, especially capital gains. Those gains may be completely eliminated at the death of the taxpayer because they may qualify for a step-up in basis.

The federal tax code is very complex. Even the very best accountants can be challenged to keep abreast of the ever-evolving nuances within the tax system. Advisors should not feel overwhelmed by all the dimensions of taxes. The idea is not to focus on the trees but rather to see the entire forest—in other words, to recognize when a planning opportunity exists and either do further projections or work with a tax expert, if needed.

Most years for clients are relatively similar and will not provide for much bracket management. However, for those clients going through significant changes or transactions, such as beginning retirement, changing jobs, or selling a business, bracket management can provide significant and worthwhile tax savings.