Language regarding a new 10-year rule introduced under the 2019 SECURE Act led many to believe that there was no annual RMD during the first nine years of this 10-year period. However, it became clear that is not the case for some beneficiaries when the Treasury Department and the IRS published proposed RMD regulations in February 2022. In response to comments from beneficiaries who were unaware of their RMD obligations for 2021 and 2022 because of this confusing messaging, the IRS issued Notice 2022-53, which explained that the 50% excise tax on RMD shortfalls would not apply to affected designated beneficiaries and successor beneficiaries who failed to take annual RMDs for 2021 and 2022.

Key terminology

This waiver under Notice 2022-53 does not apply to all beneficiaries. And understanding the meanings of the following terminologies is essential to knowing which beneficiaries are impacted.

- RMD: A minimum amount that must be distributed from a retirement account for a year.

- RBD: April 1 of the year that follows the year in which the retirement account owner reaches age 72 (age 70½ for those who reached age 70½ by December 31, 2019). If the retirement account is under an employer plan, the RBD can be deferred past age 72 until retirement if permitted under the plan’s terms.

- Designated beneficiary: A beneficiary who is a person.

- Eligible designated beneficiary: A designated beneficiary who, at the time of the retirement account owner’s death, is:

- the surviving spouse of the retirement account owner

- a child of the retirement account owner who has not yet reached the age of 21,

- disabled,

- chronically ill, or

- not more than 10 years younger than the retirement account owner.

An eligible designated beneficiary is a new class of beneficiary introduced under the SECURE Act, effective for years after 2019.

- Successor beneficiary: a beneficiary that inherits a retirement account from an eligible designated beneficiary. For the purpose of determining the distribution options for a successor beneficiary, a designated beneficiary who inherited a retirement account before 2020 and died after 2019 is treated as an eligible designated beneficiary.

- Non-designated beneficiary: a beneficiary that does not qualify as a designated beneficiary. Examples include non-person beneficiaries such as estates and charities.

A beneficiary should consult with their tax advisor or estate planning attorney to determine if they are a designated beneficiary, eligible designated beneficiary, or a successor beneficiary.

The cause of the confusion

The Setting Every Community Up for Retirement Enhancement Act of 2019, or SECURE Act, introduced the new 10-year rule for designated beneficiaries and successor beneficiaries of eligible designated beneficiaries who inherit retirement accounts after 2019. Under this 10-year rule, a retirement account must be fully distributed no later than the end of the tenth year after it is inherited by the designated beneficiary (or successor beneficiary if it was inherited from an eligible designated beneficiary).

SECURE Act language regarding the 10-year rule led many to believe that there are no annual RMD obligations under the 10-year rule, and the only requirement is that the inherited account must be fully distributed by the end of the tenth year. But the proposed RMD regulations explained that the “no annual RMD” rule applies only if (a) the owner of the retirement account died before the RBD, and (b) the beneficiary is a designated beneficiary or an eligible designated beneficiary that is subject to the 10-year rule by election or under the terms of the plan document.

On the other hand, the following beneficiaries must take annual RMDs based on the beneficiary’s applicable life expectancy and satisfy the 10-year rule explained above.

- A designated beneficiary who inherits a retirement account from an owner who dies on or after the owner’s RBD, and the death occurred after 2019.

- Roth IRA exception: Because there are no RMDs for Roth IRA owners and therefore no RBD, this would not apply to Roth IRAs. It would apply to all other retirement accounts.

- A successor beneficiary of an eligible designated beneficiary who was taking distributions over their lifetime or applicable life expectancy.

For simplification, we will call them ‘qualifying beneficiaries.’

According to the proposed RMD regulations, qualifying beneficiaries who inherited retirement accounts in 2020 have RMD obligations for 2021 and every year after. And qualifying beneficiaries who inherited retirement accounts in 2021 have RMD obligations for 2022 and every year after. These RMDs must be taken over the applicable life expectancy—which is the life expectancy of the beneficiary when the beneficiary is a designated beneficiary or the longer of the life expectancy of the beneficiary or the remaining life expectancy of the decedent when the beneficiary is an eligible designated beneficiary. A qualifying beneficiary must ensure that an inherited account is fully distributed by the end of the tenth year after inheriting the IRA or earlier if the life expectancy ends earlier.

The 50% excise tax on an RMD shortfall

A 50% excise tax applies to any RMD that is not taken by the applicable deadline. The IRS will waive the excise tax if the deadline is missed due to reasonable error. Generally, Form 5329 must be filed to either pay the excise tax or request a waiver. However, the IRS provides a blanket waiver of the 50% excise tax for qualifying beneficiaries who failed to take lifetime RMDs for 2021 and 2022. It is unclear whether Form 5329 must be filed to report any 2021 or 2022 RMD shortfall for qualifying beneficiaries.

Case studies

The following case studies illustrate.

Case study 1

The owner of the retirement account died before the RBD, and the beneficiary is a designated beneficiary who is not an eligible designated beneficiary.

- Donald died in 2020 at age 55.

- Donald’s beneficiary is his 35-year-old brother, Jim.

- Jim is not an eligible designated beneficiary (he does not meet any of the five requirements to be an eligible designated beneficiary).

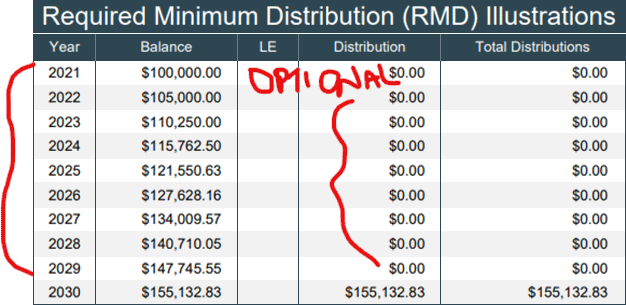

Because Donald died before his RBD, Jim must take RMDs from his inherited retirement account under the basic 10-year rule, where distributions are optional until December 31, 2030, when the entire balance must be distributed from the inherited retirement account.

Figure 1: RMD Under 10-Year Rule With Death Before RBD Assuming 5% return

Source: Denise Appleby

Case study 2

The owner of the retirement account died on or after the RBD, and the beneficiary is a designated beneficiary who is not an eligible designated beneficiary.

- William died in 2020 at age 74.

- William’s beneficiary is his 40-year-old son, Larry.

- Larry is not an eligible designated beneficiary (he does not meet any of the five requirements to be an eligible designated beneficiary).

Because William died after his RBD, Larry must take annual RMDs from his retirement account over his lifetime or life expectancy, beginning by December 31, 2021. In addition, the retirement account must be fully distributed by December 31, 2030.

Case study 3

The account was inherited from the original owner after 2019, and the beneficiary is an eligible designated beneficiary who died after the account owner.

- Sally died in 2020 at age 75.

- Sally’s beneficiary is her 70-year-old sister, Susie.

- Susie is an eligible designated beneficiary because she is not more than 10 years younger than Sally.

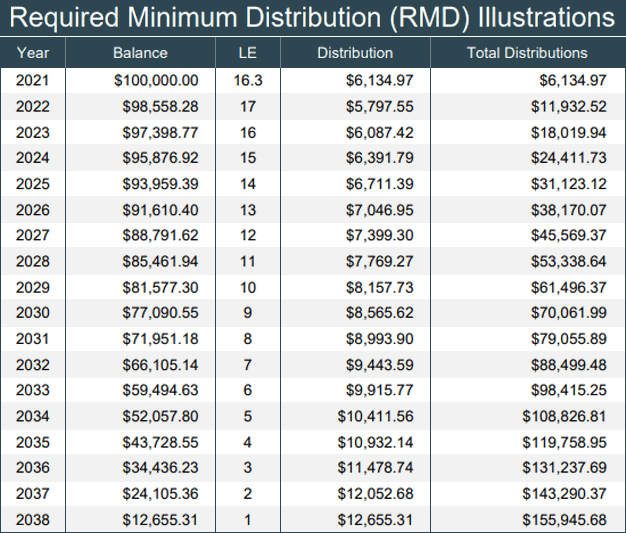

Susie must take annual beneficiary RMDs over her lifetime or life expectancy. Susie’s RMDs must begin by December 31, 2021, when she is 71. If she lives, she will have 18 years over which to take her annual distributions.

Figure 2: Susie’s RMDsAssuming 5% return and only RMDs

Source: Denise Appleby

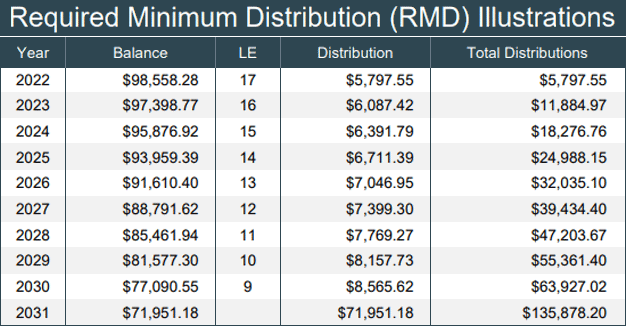

But assume that Susie died in 2021, and her beneficiary is Mark. Mark must continue taking annual RMDs over Susie’s life expectancy. However, he must fully distribute the account by December 31, 2031, 10 years after Susie’s death.

Figure 3: Susie Died in 2021—Payments Switched to the 10-Year Rule

Source: Denise Appleby

Case study 4

The account was inherited from the original owner before 2020, and the beneficiary is a designated beneficiary who died after 2019.

- Pauline died in 2015 at age 65.

- Pauline’s beneficiary is her 40-year-old daughter, Jackie.

- Jackie is a designated beneficiary.

- Jackie elects to take distributions over her life expectancy.

Jackie’s annual RMDs must begin by December 31, 2016, when she is 41, and her life expectancy is 42.7 years. Therefore, she will have 42 years to take her distributions if she lives.

But assume that Jackie died in 2021, and her beneficiary is Jill. Jill must continue taking annual RMDs over Jackie’s life expectancy. However, she must fully distribute the account by December 31, 2031, 10 years after Jackie’s death.

In the examples above, Larry, Mark, and Jill would otherwise owe the IRS a 50% excise tax on any RMD not taken for any year, starting with 2021. But Notice 2022-53 waives the excise tax for 2021 and 2022 because Larry, Mark, and Jill were unsure whether they were subject to RMDs for 2021 and 2022. Their reasonable error is the misleading guidance from the SECURE Act.

Next steps for beneficiaries

Notice 2022-53 clears the path for qualifying beneficiaries by ensuring they have no requirement to play catch-up or pay the excise tax for 2021 and 2022 RMDs. However, all other beneficiaries who fail to take their 2021 and 2022 RMDs must consult with their advisor regarding taking corrective steps. In addition, all beneficiaries with inherited retirement accounts should consult their tax advisors regarding their RMD obligations.