HackTalk is a long-running monthly podcast with Sean Bailey and Devin Kropp, co-authors of “Hack Proof Your Life Now!,” which covers cybersecurity threats and issues advisors need to know to protect themselves and their clients. You can listen to the full broadcast in the video below—in which Sean and Devin also talked about the importance of having your clients put freezes on their credit lines.

A wave of sophisticated cyberscams is preying upon one of society’s most vulnerable groups—the elderly. As a financial advisor, you are uniquely positioned to spot signs of fraud that can threaten the financial wellness of your clients. Simple actions you take can empower your clients to protect themselves.

You can maintain vigilance and prevent some common forms of cybertheft by watching for red flags—both in your clients’ accounts and in their behaviors—and by encouraging your clients to follow some simple safeguards.

The scope of the problem

Elder fraud is defined by the FBI as a form of older adult exploitation in which a perpetrator misuses or steals financial assets, savings, income or personal identifying information from an adult over the age of 60, often without their direct knowledge or consent.

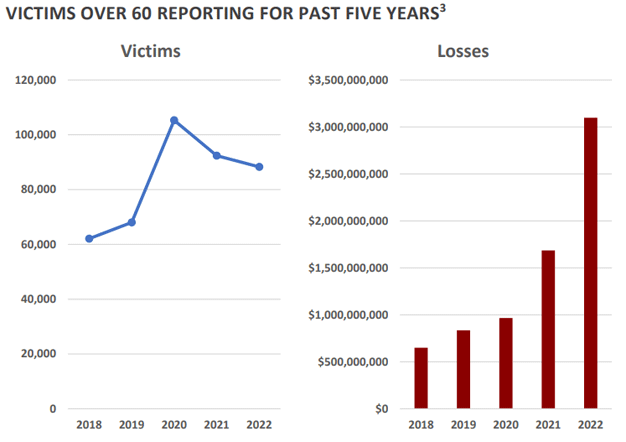

Elder fraud has become a growing epidemic. An estimated $28.3 billion is lost to elder fraud scams each year, according to a recent survey by AARP.

The FBI’s Internet Crime Complaint Center reported an 84% increase in elder fraud in 2022 over previous year figures. Tech and customer support schemes were the most common form of fraud, with 17,800 complaints. Investment fraud among those over age 60 increased more than 300%.

Take note: Many of the investment fraud cases involved the use of some type of cryptocurrency, a preferred payment method for many scams. Losses connected to those complaints totaled more than $1 billion.

Other elder fraud statistics from the report:

- Total losses: $3.1 billion.

- Average dollar loss per victim: $35,101.

- Victims losing more than $100k: 5,456.

Figure 1: Elder Fraud Losses Are Growing

Source: FBI, Elder Fraud Report 2022

William Webster, former director of the FBI and the CIA, was himself victimized by elder fraud, when he was targeted in a lottery scam in 2014. He published a video for the FBI in which he warned people about the dangers of elder fraud.

Devin Kropp: “Most agree that all the numbers you see reported out there are actually underestimating the number of victims and scams and frauds that we see among this age group because some people are embarrassed and don’t want to admit it.”

The biggest scams targeting seniors

As trusted professionals, financial advisors are in a prime position to both spot signs of elder abuse and help educate and empower older clients to avoid scams.

While cybercriminals attack people of all ages, some scams are aimed specifically at senior citizens. Three of the most prevalent:

Government imposter scams

Phishing scams pretending to be government entities like Medicare or Social Security are incredibly common.

Kropp: “Being aware of regular phishing principles, examine the message and inspect link email that we talk about in our program where you hover your mouse to uncover the true sender of an email or the URLs in it. It’s also important to be aware of what types of phishing scams we see here.”

These emails and phone calls try to trick victims into revealing personal information like Social Security or Medicare numbers by claiming the info is needed to verify accounts or continue receiving benefits.

No government agency will ever make these kinds of requests by phone or email.

Takeaway: Advise clients to ignore unsolicited contacts asking for sensitive details. If concerned an inquiry is legitimate, have them call the agency directly using an independently verified number.

Tech support scams

Scammers frequently contact seniors claiming their computer has a virus or other malware. They offer to “help” by accessing the device remotely. After being given access to the computer they either steal personal data or infect the machine with malware themselves.

Takeaway: Warn clients not to allow remote access or provide sensitive info to any unsolicited tech support contact. Have them confirm suspected issues with someone they trust before taking action.

Romance scams

Perpetrators build online relationships with seniors, gaining affection and trust over time. Eventually, they fabricate an emergency requiring funds.

Kropp: “I’ve read some really heartbreaking stories about elders who have sent thousands of dollars to these people thinking that it’s their partner and in reality it’s someone behind a computer that has no interest in them or just taking this money to do whatever with.”

These scams are emotionally devastating and tough to detect.

Kropp: “So this is a particularly tricky area to help someone in because there’s emotions involved. But especially for advisors, if you have one of your clients coming in and they’re talking about sending money overseas or they’ve met this person, you might want to ask some questions and try to be that professional which can shed some light on what might be going on. Keep a close eye on that because I’ve read stories too where the advisors are actually the people who discover these kinds of scams are happening. They see the money leaving, or the person asks to take money out of a retirement account and they start to ask questions. Often it might be the person’s kids missed that this was going on, but the advisor is the person who actually identified the problem.”

Takeaway: Look out for transfers, especially to overseas destinations, to questionable new partners. Check in sensitively with clients about new romantic interests.

3 steps to safeguarding finances

In addition to watching for red flags, advisors can help protect seniors against fraud by ensuring good financial security practices. Here are three simple steps:

- Set up account alerts to be notified of unusual transactions so action can be quickly taken. Review statements regularly as well. Teach healthy skepticism to verify unsolicited requests.

- Make sure devices are running updated software to fix vulnerabilities and prevent malware. Recommend security software and updates.

- Advise caution sharing personal information or funds unless verifying independently first, especially with government ID numbers.

Maintain vigilance

Ongoing education and monitoring are also key. Classes on cybersecurity and scams can empower seniors to identify and avoid fraud themselves. Addressing isolation that leads to loneliness can reduce vulnerability, too. Monitor clients with cognitive decline carefully, as impaired judgment increases susceptibility.

As trusted professionals, advisors should adopt practices to enhance protection. Ask questions about suspicious activity. Have a referral source for trustworthy technical assistance. Encourage discussing scams to reduce stigma and promote education. Report scams to help prevent further victimization.

For seniors, knowledge is power for defending against elder abuse. Awareness, verifying questionable requests, security measures, and monitoring for red flags allow financial advisors to play a crucial part in protecting elderly clients from elder abuse.