Late Wednesday, Silicon Valley Bank announced Treasury sales and had begun the process of raising capital. The stock cratered on Thursday, customers began to pull funds, and Friday morning regulators closed the bank.

Over the weekend, the government shuttered Signature Bank. Like SVB, Signature, which had a presence in the crypto space, had a very large share of uninsured deposits.

In the wake of the unexpected failures, regulators have raced to contain the crisis.

The bedrock of the financial system is confidence. We hold funds in banks and money markets because we are confident we can withdraw those funds at any time. If confidence turns to panic, the system collapses.

Early actions taken to guarantee all deposits at the failed firms and the Fed’s announcement of a safety net for banks holding Treasuries are controversial, but early indications suggest they are working.

But the environment remains uncertain. On Wednesday, Credit Suisse said, “Material weakness” its internal controls over financial reporting “could result in misstatements… that would result in a material misstatement to the annual financial statements.”

The Saudi National Bank, its largest shareholder, said it would not offer additional support to Credit Suisse, and its shares tanked.

Credit Suisse has been a slow-motion trainwreck for years. But the latest revelation is happening in the wake of SVB’s demise, exacerbating concerns.

Credit Suisse’s latest problems may bring the Swiss National Bank (Switzerland’s central bank), the Swiss government, and possibly the European Central Bank into play.

For now, the banking crisis has taken the “no landing” scenario off the table, as some banks will likely tighten up on lending in order to shore up balance sheets.

Crash landing? Doubtful. But the odds of a recession have risen.

1. Did the Fed just break something?

- The short answer is “Yes.” Its aggressive campaign turned bank bond portfolios upside down.

- Can a bank without loan-quality issues implode in less than 48 hours? Yes.

- Meteoric bank growth, rising interest rates, unfortunate decisions by management, a mismatch of duration among its extremely safe assets and liabilities, regulator missteps, and panic led to the demise of a 40-year-old institution.

- SVB was shuttered late Friday morning. Regulators likely were trying to salvage what was left of the bank, allowing for a possible sale or orderly liquidation of assets which would eventually (hopefully) return most deposits to uninsured depositors.

- A buyer of SVB didn’t surface, which led the government to extend insurance to all depositors.

What happened?

- Bank customers were losing access to new funds via fundraising and began burning through cash at the bank, what SVG called an “elevated cash burn level.”

- Late Wednesday in a mid-quarter update, the bank said it had sold $21 billion in highly liquid, ultra-safe Treasuries.

- Treasuries don’t have credit risk but are subject to interest rate risk. Rates have risen, bond values have fallen, and the bank took a $1.8 billion after-tax haircut on the sale.

- SVB had lined up new financing, but the stock cratered on Thursday, scuttling its attempt to shore up its balance sheet.

- Uninsured depositors, which accounted for almost 90% of its deposits (some estimates as high as 97%), began to flee the bank.

Well-capitalized banking system

- The banking system is in better shape today than in the 2000s.

- The speed of the failure was not the result of bad lending practices. Instead, it was a mismatch of duration coupled with falling bond prices (compliments of Fed rate policy).

- In the days and weeks to come, we’ll get a better picture, probably faulting regulators and bank management.

Contagion fears

- SVB isn’t the only bank that’s been challenged by falling bond values.

- The FDIC said banks had about $620 billion in unrealized losses as of the end of last year, according to the WSJ.

- If held to maturity, it’s not a big issue.

- If forced to sell, as SVB did, it could be catastrophic.

- Following SVB’s demise, might bank depositors ‘shoot first, ask questions later?’

The cavalry to the rescue

- All deposit accounts at SVB and Signature Bank are insured, according to a joint statement released by the Federal Reserve, the Department of the Treasury and the FDIC.

- Shareholders and certain unsecured debtholders will not be protected.

- Any losses to the Deposit Insurance Fund to support uninsured depositors will be recovered by a special assessment on banks, as required by law.

- In theory, taxpayers aren’t on the hook.

- The Fed will also lend out against the full value of eligible securities (par value).

- It has been crafted to prevent the forced sale of bonds.

- The loans will be collateralized by the bonds. The Fed should make money on the plan.

Final thoughts

- Bank runs are in no one’s interest.

- Investors need some space and breathing room—a cooling-off period in the hopes cooler heads prevail. The situation is fluid, but the government appears to be successfully ring-fencing the failed entities.

- Issues of a moral hazard are being thrown around. That’s not a surprise.

- SVB’s failure has exposed problems in the banking system that had been lurking under the surface.

- The Fed and regulators failed to foresee last week’s crisis.

-

Rate hike cycles typically end when the Fed breaks something, but inflation remains a problem.

2. Banking crisis complicates Fed’s inflation-fighting

- An upbeat start to the year, upward revisions to inflation late last year, and hotter-than-expected inflation in January forced Powell to abandon his more conciliatory tone and investors began pricing in a 50 bp rate hike in March—see Figure 1.

- Higher for longer took on new meaning.

- But the failure of SVB and the impact of further rate hikes on bank-bond portfolios may force the Fed to re-think or at least slow the pace of rate increases.

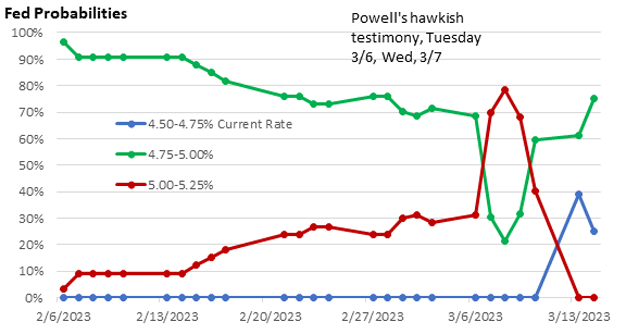

Figure 1: Place Your Bets

Source: CME Group 3/14/2023

Fed funds futures are a snapshot in time. Forecasts can quickly change amid changes in sentiment.

- As Monday came to a close, investors were pricing in a nearly 40% chance the Fed will forgo a rate hike next week.

- That was unthinkable last week

- Fed funds futures are closely watched by analysts and professional investors, but shifting economic winds can quickly change sentiment.

- A year ago, fed funds futures suggested that a fed funds rate of 2.00%–2.25% was the most likely outcome.

- The track record for outlying months is problematic at best.

- The Fed’s record isn’t all that promising either.

- In March 2021, the Fed was still projecting a zero fed funds rate by year-end 2023.

- Decisions are made based on rate forecasts, forecasts that turned out to be badly flawed.

| Table 1: Federal Reserve Fed Funds Rate Projections |

| Date of Fed meeting |

Year-end 2023 |

Year-end 2024 |

| March 2021 |

0.1% |

— |

| June 2021 |

0.6% |

— |

| September 2021 |

1.0% |

1.8% |

| December 2021 |

1.6% |

2.1% |

| March 2022 |

2.8% |

2.8% |

| June 2022 |

3.8% |

3.4% |

| September 2022 |

4.6% |

3.9% |

| December 2022 |

5.1% |

4.1% |

Source: Federal Reserve Summary of Economic Projections

- The Fed’s forecasting models are poorly calibrated in today’s post-pandemic world. There is little confidence in their economic, rate and inflation forecasts.

3. Is today’s fed funds rate still stimulative?

- That’s not the conventional wisdom, so let me explain.

- Included in its annual projections, the Fed releases what it calls the longer-run fed funds rate.

- The longer-run rate is simply an estimate of what the Fed believes is a fed funds rate that neither stimulates economic growth nor restricts growth.

- Lower than neutral is stimulative.

- Higher than neutral is restrictive.

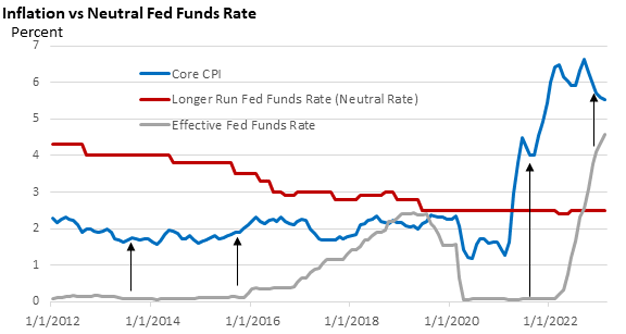

Figure 2: Changing Conditions

Source: St. Louis Federal Reserve Feb 2023

- For most of the 2010s, the neutral rate (red line) exceeded the inflation rate (blue line). In other words, the neutral rate that neither stimulated nor restricted economic growth was positive after adjusting for inflation.

- Today, the Fed’s neutral rate is far below the rate of inflation.

- Today’s fed funds rate is below the core CPI, though the gap has narrowed.

- In my view, the neutral rate might be in the 2.5% range if inflation were near 2%, as it was prior to the pandemic.

- With inflation running hot, coupled with rising wages, the Fed has been reluctant to raise the neutral rate. It’s still too low, in my view.

- Given higher inflation and rising wages, today’s fed funds rate might still be modestly stimulating growth. Inflation and wages are rising faster than the neutral rate.

- No question about it, Fed actions have hit the housing market hard, but lending rates in a number of industries, including autos, remain quite low versus today’s rate of inflation.

- If inflation proves to be sticky, today’s rates will continue to look attractive (outside of housing), and the terminal rate may turn out to be much higher than many investors currently anticipate.

- Final caveat—post-SVB, might we see a big contractionary shift in lending standards? That would be disinflationary.

4. Mostly in-line CPI

- The Consumer Price Index slowed from 0.5% in January to 0.4% in February, as food rose 0.4% and energy fell 0.6%. The headline matched expectations.

- The core CPI accelerated from 0.4% to 0.5%, ahead of the 0.4% consensus.

- Year-over-year, the CPI slowed from 6.4% to 6.0% and the core slowed from 5.6% to 5.5%.

- Aided by another decline in medical care services, services less housing (so-called super core), rose just 0.1%. It’s been volatile.

- Consumer goods less food, energy, and used autos (declined 2.8%) rose 0.4%. While Powell has hailed progress in goods, recent data suggest that core goods prices ex-used cars may be proving to be stickier than expected.

- Inflation has probably peaked but is well above the Fed’s 2% goal.

5. A peek ahead

The Fed’s delicate balancing act

- While the situation is still fluid, early signs suggest that the government actions taken in the wake of the bank failures are calming frazzled nerves.

- The Fed’s Bank Term Funding Program is designed to mitigate balance sheet risk, ring-fence the failed banks and prevent contagion, which allows the Fed to keep hiking.

- Early indications: on the surface it’s working.

- The Fed is acting in its primary role, as lender of last resort.

- A 50 bp rate hike next week is off the table. It was the likely path pre-SVB.

- But chatter early Monday that the Fed might go on hold appears to have been an overreaction—25 bp is the current bet. Assuming we have no banking or credit market surprises next week, the Fed appears set to cautiously raise the fed funds rate by 25 bp, at least according to fed funds futures.

- The Fed’s resolve to bring inflation down remains strong, but bank balance sheets are on the radar.

- There is an outside chance that the Fed will prioritize the financial system and temporarily go on hold.

- They will be monitoring bank flows up until the meeting.

- Is there enough stability in the financial system to move on rates next week? It’s uppermost on the minds of Fed officials.