The world has changed on many fronts since COVID-19 hijacked the global economy and unleashed a worldwide health crisis. The wealth management business isn’t immune, but financial services are among the better-positioned industries to weather the uncertainty by moving into digital and web-based resources.

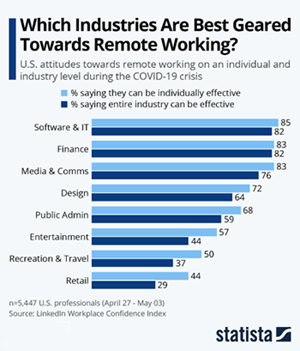

A survey conducted in early May of U.S. professionals ranked finance second after information technology as an industry that’s well-suited for remote working. More than 80% of respondents offered a positive view for conducting business outside of the traditional office setting, according to Statista, a research firm.

The good news for wealth management is that the embrace of tech has been accelerating in recent years, which lays the groundwork for navigating the current crisis—and beyond—with minimal disruption. For some firms, the transition has already been dramatic. Recognizing how much has changed, JPMorgan Chase—the investment bank—announced in 2016 that “we are a technology company.”

Consumers are on board with the ongoing and recently accelerated transition in finance, according to a recent survey. Blumberg Capital, a venture capital firm, reported in October that “73% of respondents said that they prefer to handle their financial dealings online—up from 68% in 2017.”

Some financial advisors have balked at the growing use of financial technology —fintech in the industry jargon. But due to the pandemic, reluctance has given way to necessity as technology offers a lifeline in a world where working from home has become standard procedure.

Not surprisingly, business models have evolved, sometimes dramatically and with record speed, although not always by choice. For some insight to what’s happening on the front lines, Horsesmouth asked several wealth managers how the coronavirus-triggered upheaval has altered their routines. Here are some of the highlights.

Virtual meetings

“My way of communicating with clients has absolutely changed,” says Janice Cackowski at Providence Wealth Partners. “There are now more phone calls and Zoom meetings.”

It’s not always the first choice for some clients, but it’s become a crucial link as coronavirus derails in-person meetings and conversations.

“Videoconferencing and screen sharing go a long way toward keeping a personal connection,” reports Sean O’Shea at Highpoint Planning Partners. It may not always be the first preference, but some clients are making the most of it, he says. “I had an older client get a kick out of changing their video background to a Hawaiian beach and the Sphinx while I rambled on about interest rates and unemployment numbers.”

Forced into a crash course on video conferencing, some advisors are taking advantage of the shift to refine and broaden their tech skills. “You learn to manage Zoom calls with five or six people,” says Brittain Prigge, president of Balentine LLC, an Atlanta-based wealth manager with a staff of 39.

Developing tech skills is important, especially as working at home has become the norm. But recent history also provides deeper lessons for managing client relationships and office staff, Prigge adds.

“I’m much more open-minded about flexibility,” she explains, adding that before the pandemic she didn’t fully appreciate the capabilities of Balentine’s staff to keep operations running smoothly. But after witnessing the company “run like clockwork” with a remote and scattered staff, her crew is “thriving” at home. It’s been a wake-up call, she admits.

Client communications are no longer face-to-face affairs, but the value of communicating has rarely been higher, observes Jon Ten Haagen, CEO of Ten Haagen Financial Services. “There are a lot more questions this time around,” he says.

His goal, however, remains unchanged: “Trying to get people to look long term and focus on why they are investing.” It’s a perennial battle, he adds, in part because he’s constantly “fighting the media” and its short-term focus.

Rita Cheng, CEO and co-founder of Blue Ocean Global Wealth, had already been transitioning to digital operations in recent years, using fintech applications such as Riskalyze and eMoney. But the critical factor remains communication with clients, she says, adding that the crisis has reinforced this point and inspired efforts at expanding the channels for reaching out.

“I’ve been coaching people on how to use Zoom,” she says. Offering guidance so that clients don’t get frustrated with technology is essential, Cheng notes. But first, make sure that you’re fluent with the technology, she recommends. “If you’re frustrated with it, the client will be frustrated.”

Business as usual?

Advisors who went independent long before the coronavirus crisis hit have, to some extent, been working remotely all along. Take Bill Nickles at Yellow Dog Financial, a boutique financial planning shop that he set up in 2008 in Bolton, Massachusetts.

“I routinely work from home and most of my meetings are held virtually using Zoom, so not much has changed in that respect,” he says. “I have clients throughout the country so face-to-face meetings are not expected.”

Independent-minded advisors may be rolling with the punches these days, but some clients are frazzled. “We’re experiencing a mass trauma across the United States, if not the world,” observes Brad Klontz, a psychologist and founder of the Financial Psychology Institute. “Our illusion that we’re safe has been shattered. It’s like a psychological earthquake,” he recently told the New York Times.

Managing wealth and client relationships isn’t getting any easier these days, but the crisis presents an opportunity to highlight the value of guidance beyond overseeing portfolio strategies and recommending how to navigate estate plans.

“If there’s one thing we can do as financial advisors it’s remove emotions from the process,” says Randy Bruns at Model Wealth. By that standard, financial planners have been a busy bunch lately. “I’d be lying if I said there weren’t a small number of people we’ve had to talk off the ledge,” he confides.

For Mark Berg at Timothy Financial Counsel, the means of delivery is secondary to the advice. “The financial planning part of what we do is really where our clients have gained the most peace amid the uncertainty,” he says. Working remotely has been a transition, although one that’s been “virtually seamless,” he says, thanks to tech investments prior to the coronavirus crisis.

What hasn’t changed, Berg continues, is the focus on educating clients on how to achieve their financial goals. In fact, the crisis helped provide real-world perspective on how factors can affect their lifestyle and legacy. In terms of day-to-day activities, he reports that there’s been more tax-loss harvesting, rebalancing and looking for lower-cost, more tax-efficient investments.

Is this the new normal?

One question that’s lurking in everyone’s mind as the virus continues its spread: Is the recent shift to virtual meetings and web-based communications permanent? Or is this just a passing fad that will fade once a vaccine is developed and something approximating the old normal returns? No one really knows, of course, although some advisors are ready to consider the possibility that regime shift may have arrived.

Jacqueline Schadeck at Sherrill and Hutchins in Atlanta says that while the basics of advising clients hasn’t changed, communication has evolved. “I’ve really leaned on the ability of e-communication tools by implementing video meetings or phone calls and sending more mass communications via email. According to client feedback, this is proving to be sufficient and possibly the new permanent way of operating,” she tells Horsesmouth.

In a possible sign of the new normal that’s approaching, a number of companies outside of finance have announced a shift to permanent work-at-home staffing. The CEO of Shopify, one of Canada’s most highly valued companies, in May outlined the end of “office centricity” and allowed its 5,000 employees to work remotely on a permanent basis.

Twitter, the social media firm, made a similar change. The company’s chief, Jack Dorsey, emailed the staff advising that working from home is fine for as long as employees decide that is viable.

Lifestyle flexibility is a key advantage of working remotely for some advisors. “I was operating at about 75% virtually when this whole thing started. Now I am happy to say that I am 100% virtual,” reports Michael Whitman, a managing partner at Millennium Planning Group. “I love being able to work and serve my clients from wherever I am and wherever they are.”

Rose Price at VLP Financial Advisors says the growing use of virtual communication with clients has created a need to evolve. “We have been holding webinars for clients and developing more virtual content.” Roughly one-third of clients were using remote meetings previously and the crisis has, of course, raised that level sharply.

The push toward normalizing virtual meetings may continue in the months and years ahead, but by some accounts the trend has a downside. Providence Wealth Partners’ Janice Cackowski says the transition to Zoom meetings and phone calls has worked reasonably well, but it’s “a bit painful for me because I enjoy seeing my clients. A virtual meeting is simply not the same as meeting in person, shaking hands or sharing a hug with the clients I care about.”

Balentine’s Brittain Prigge reports a different experience, explaining that “relationships have gotten stronger” during the crisis. She says she’s learned to listen on a deeper level. “People had a lot of fear,” she recalls. After one late-night phone call with a client, her children asked: “I thought you manage money?”

“No, I help people,” she responded.

Can you help people through Zoom meetings and web-based financial-planning presentations? Yes, advisors have found that you can. Yet many do miss being with their clients in person. And in terms of spending quality time with clients, Prigge says the crisis has been a revelation. Face-to-face meetings will always play an important role in wealth management, she says. “But we don’t need to fly to Houston to give a report. If you want to see a client, go have dinner.”