The year is coming to an end soon, and it’s time to focus on your clients’ year-end items. For Q4, there are several things that every advisor should be considering on behalf of their clients. Some are tax-related, others are planning items, yet others are investment-related, and some revolve around important messaging to clients. Either way now is the time to review this list to ensure that your clients are prepared for the upcoming year.

1. Scheduling appointments for year-end meetings

For anyone who believes year-end checkups can wait until December, think again. Now is the time to get started with your most valued client reviews. At Taylor Financial Group (TFG), we have scheduled four to five client appointments a week between October and the end of the year so that we can meet with all of our A+, A, and B clients during Q4.

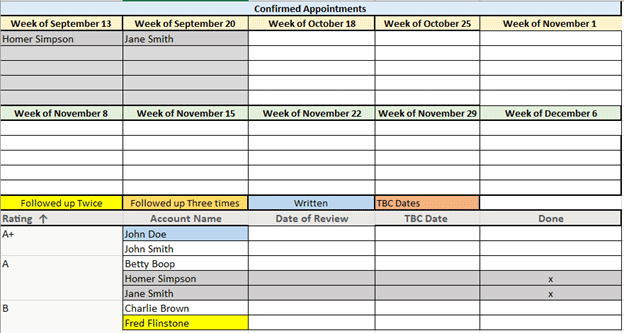

We created a spreadsheet (see Figure 1) of all the clients we wanted to meet with because, as you know, what gets measured gets done. We broke the spreadsheet into different categories: client rating (A+, A, B, C, D), client name, date of review (actual date confirmed with the client), TBC date (the dates we offered for the review), and a done column (meeting is complete).

Starting in 2022, we are changing our client meeting and call frequency to regain some extra time but still ensure each client is getting the proper attention. It is the difference between being always available and being accessible.

We decided to only take appointments from September to early December for year-end meetings and then again in mid-April to early July for mid-year reviews. This way, we create more time in January, February and March to focus on taxes. However, we will still be available for emergency appointments.

Figure 1: TGF Clients-to-Meet Spreadsheet

Source: Taylor Financial Group

2. Review and update your client meeting agendas

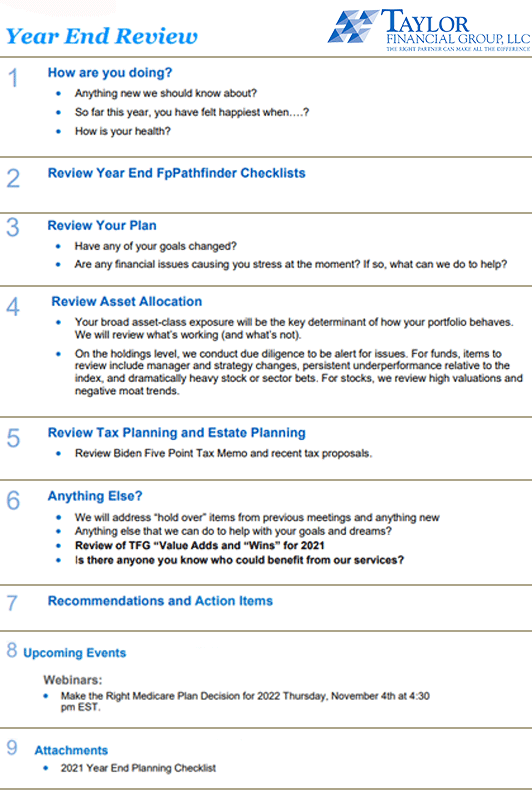

Every advisor should be updating their meeting agendas each quarter, but this is especially important for year-end (see Figure 2). Each agenda should be an overview of what the review should address, reflecting the critical needs of the client and what you plan to address, such as proposed tax law changes, year-end tax planning, and so on.

While all this may seem to be a lot, we always share the agenda with our clients before the meeting. This ensures that we are all on the same page and gets them thinking of questions they want to bring to the meeting.

Figure 2: TFG Year-End Review Agenda

Source: Taylor Financial Group

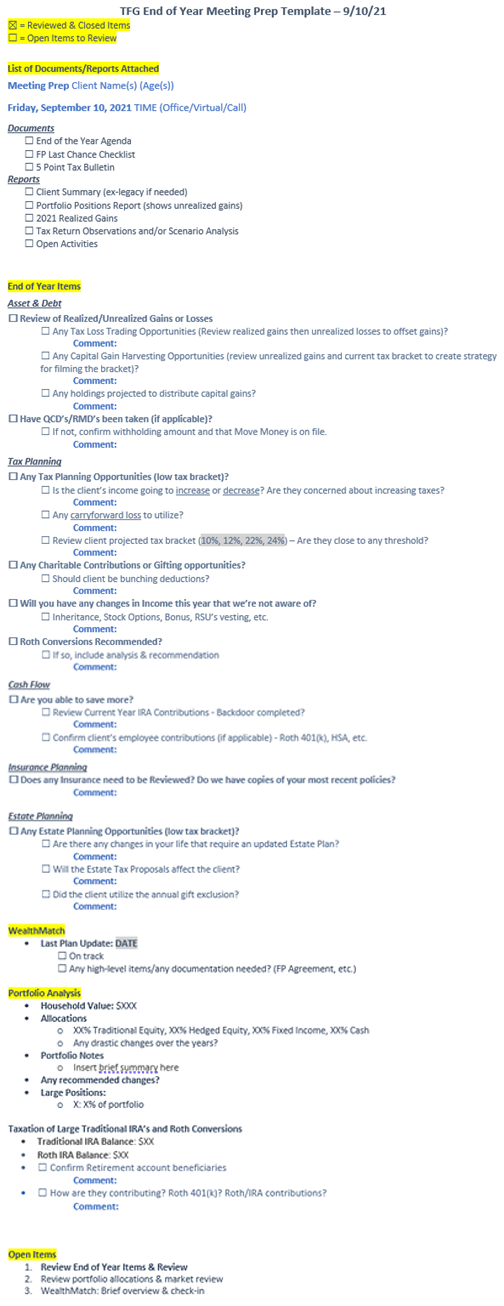

3. Update year-end meeting prep 2 biz days before meetings

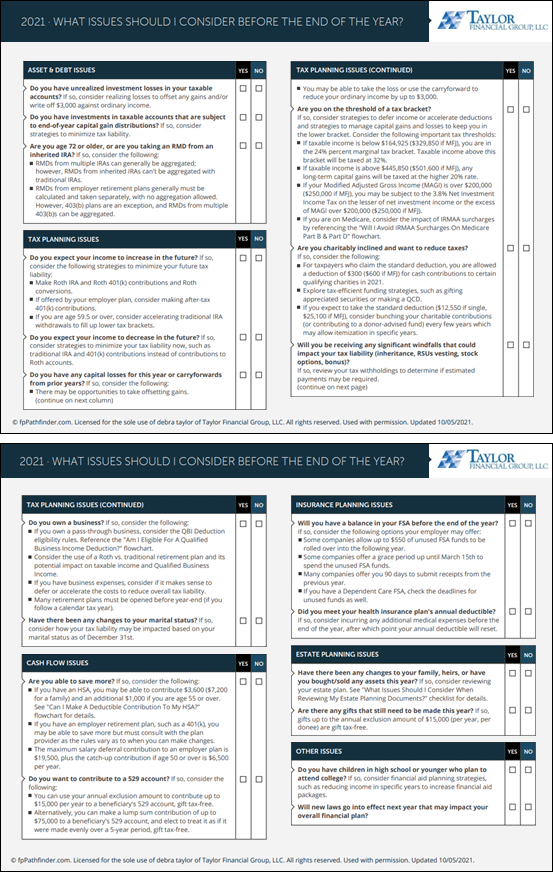

Unfortunately, it’s hard to remember everything that has to be done for every client for year-end without a client meeting prep checklist (see ours in Figure 3). While prepping for meetings we use the “What Issues Should I Consider Before the End of the Year” checklist from fpPathfinder. You will see in Figure 4 the fpPathfinder checklist. Note that the fpPathfinder checklist includes a lot of the year-end items such as tax-loss trading and gifting that we should discuss with the client.

This checklist provides us with a guide to many planning opportunities and issues to discuss with our clients. This is a comprehensive checklist of the types of year-end planning issues that advisors should be using to prep their client meetings to ensure their clients consider and take advantage of opportunities in the current year and beyond.

It is imperative to create a process to prepare for a client meeting and have your team stick to so that every client is treated properly. We require our junior employees to complete the meeting prep template two days before the meeting to be reviewed by a senior employee.

Figure 3: TFG End- of-Year Meeting Prep Template

Source: Taylor Financial Group

Figure 4: The fpPathfinder End-of-Year Checklist

Source: Taylor Financial Group

4. Using year-end checklists and flowcharts to engage clients

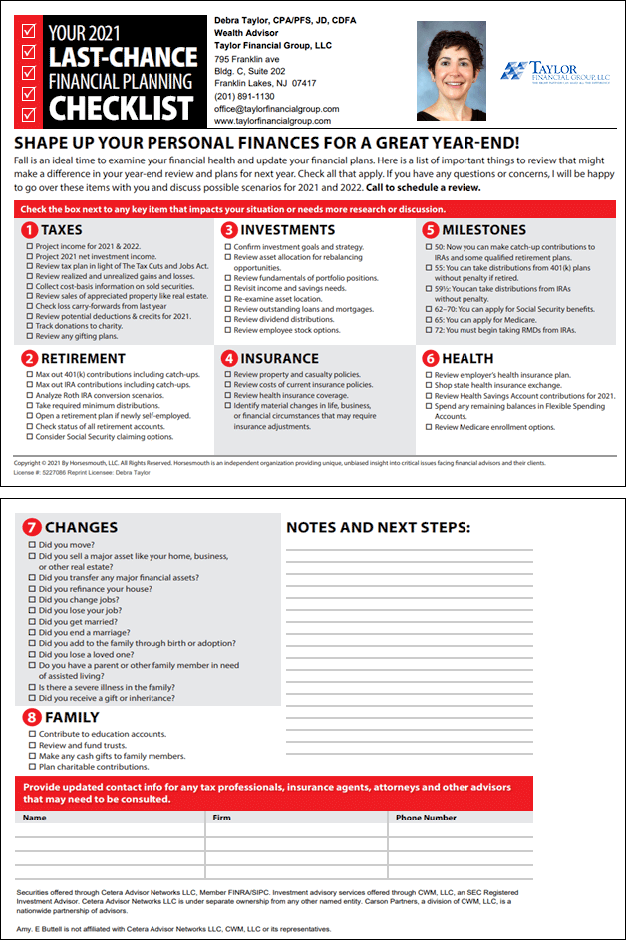

When confirming every client meeting from September to the end of the year, we send our clients the “Last Chance Financial Planning Checklist” from Horsesmouth. This year, it is especially important, since our clients have experienced a lot of change over the past year.

We send the checklist in advance of the meeting so our clients can take the time to review it. They then usually come back with specific things they want to talk to us about that affect their Financial Plan, from retiring early, selling or buying a house, having a grandchild, and so on.

The “Last Chance Financial Planning” checklist from Horsesmouth, shown below in Figure 5, features eight areas of focus: taxes, retirement, investments, insurance, milestones, health, changes and family. It’s important to note that this checklist is not meant to be all-inclusive—rather, it covers the areas most relevant for year-end.

Figure 5: Horsesmouth 2021 Last-Chance Financial Planning Checklist

Source: Taylor Financial Group

5. Gather your client’s tax returns

For advisors to do comprehensive financial planning for their clients, it is crucial to have their most recent tax returns. Advisors often hesitate to collect tax returns from their clients because they believe it is personal and sensitive information. They are not wrong—it is personal and sensitive information, but it is impossible to accurately plan for your client’s future without their tax return.

Not only does obtaining client tax returns give us the chance to provide additional value, but the returns also help us identify opportunities that we would otherwise not know about. For example, by having a client tax return, we can see if the client has a carryforward loss that we can take advantage of for the upcoming year.

Depending on the size of the loss, we know how much capital gain we can realize without creating an additional tax burden. These are the types of things we analyze for our clients, and they can only be appropriately planned for if the tax return is in our possession.

More critical, tax returns let us see the client’s previous tax year and assist us in creating projections for their current tax year. One of the essential items this helps us with is mapping out Roth conversions and whether or not the client should perform one. Of course, this all depends on their goals, age, size of their pre-tax retirement account balance and tax bracket.

Figure 6 shows our announcement to clients requesting their tax returns.

Figure 6: TFG Announcement Requesting Tax Returns

Source: Taylor Financial Group

6. Perform a Roth conversion analysis before the end of 2021

Q4 has always been an ideal time to consider Roth conversions for clients, but with potential tax law changes on the horizon, now is the time to consider converting traditional IRAs to Roth IRAs. Congress is seeking to eliminate these privileges for high-income earners in 2032. Congress could also do away with backdoor Roth conversions for everyone starting in 2022, eliminating the ability to contribute after-tax money to an IRA or 401(k) and immediately convert these contributions to Roth.

Conducting Roth conversion analysis for our clients has always been one of our most significant value-adds. We analyze our clients’ tax returns every year using Holistiplan to ensure that they take advantage of opportunities to do conversions and increase their Roth balances. This has been a critical time for us. We are constantly in contact with our clients about proposed tax changes and keep them up to date on what it might mean for their financial plans. With these potential changes looming on the horizon, our clients will have a big decision to make about performing Roth conversions.

Reviewing and taking action on the six items discussed above will ensure you address every potential issue with your client and set them up for a good year ahead.