Editor’s note: Across the gamut of our 2023 articles explaining tax law changes, the bewildering economy, and how to be a better advisor, these Members’ Choice runner-up articles equipped you for powerful performance. These just missed a spot in our annual Top 10 list, but were still among the most popular articles of the year.

Your discovery meeting may be the most important meeting that you attend. We all agree that regular reviews with clients are an important part of the client experience and aid in retention. But a firm that isn’t growing could develop a whole set of problems such as inability to recruit, declining profits and low morale.

Your ability to bring on new clients will start (and may end) with that all-important discovery meeting. We discuss below five critical things to be doing before, during or after each discovery meeting.

1. Prescreen so that you don’t waste your time

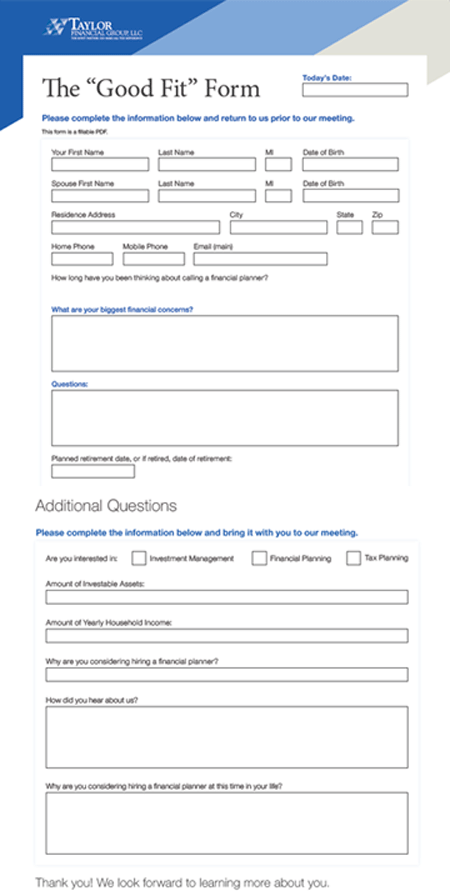

Before we schedule any prospect meetings at Taylor Financial Group (TFG), the prospect must complete our Good Fit Form (GFF). The GFF is a two-page form asking the most basic of questions. It is easy to complete, and we also use a fillable pdf to make it simpler for the prospect. We send the GFF as soon as we learn that the prospect wants to meet with us. We ask them to complete the GFF and say we will reach out to set up a 20-minute Good Fit Call.

The GFF (shown below) asks for name and address, but it also asks about investment assets and also whether the prospect is interested in investment management, financial planning, tax planning or all of the above.

Figure 1: Save Time and Effort by Prescreening

Source: Taylor Financial Group

Based on the prospects’ answers, I will have a better idea as to what they are interested in and whether we can be a good fit. I will sometimes decline the call if the investable assets are low (with no hope of increasing), or if the prospect is only looking for planning and not investment management. Of course, these are my particular criteria. There is no right or wrong answer here; you will be screening for clients that fit into your strategic objectives, the type of work you want to take on, and your workflow.

The point here is to know what you are getting yourself into, so that you can spend your time wisely.

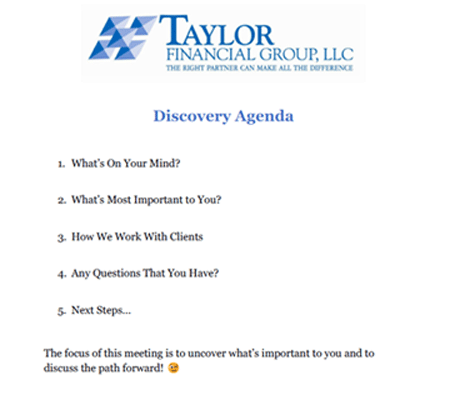

2. Create an agenda

I have two different agendas to potentially use for discovery meetings. One is simple and the other is more detailed. At this point, I like both agendas, and both could be used effectively. There are arguments to be made in favor of each approach, so I will submit both agendas to you and let you decide.

The shorter version (shown in Figure 2) is straight and to the point. It is easy to understand and not intimidating. It may make sense for a client who wants to keep things simple, and it allows you the flexibility to elaborate…or not. If you use the shorter agenda, make sure that you have a good command of your talking points, because you want to make sure that you cover all important topics, such as your services, client experience, investment philosophy and fees.

Figure 2: The Short Agenda

Source: Taylor Financial Group

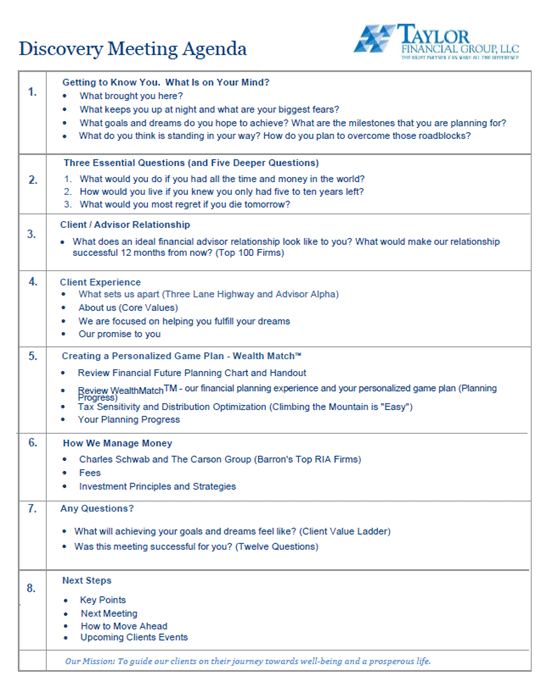

We also use a longer agenda, and this is the version I have used for years, with updates along the way. The nice thing about the longer agenda is that it is comprehensive by its very nature, so you and the prospect know that nothing will be omitted. It provides a nice road map for the meeting, albeit a rather detailed one.

Figure 3: The Comprehensive Agenda

Source: Taylor Financial Group

3. Be prepared with background research

Although our time is valuable, walking in cold to a prospect meeting may give the wrong impression and may cause you to waste your opportunity. You may only get one chance to impress your prospect, so you need to arrive at the meeting prepared to impress.

We have an entire discovery meeting checklist that includes pulling and analyzing investment statements (if we have them) using Riskalyze. We can also use YCharts to analyze the investments, and we share our thoughts with the prospect.

We also take a few minutes to research the prospect on social media, just to see the value of their home, their professional life and any other quick tidbits that we can pick up.

4. Have a documented client value proposition that goes beyond investment management

According to the Charles Schwab Benchmarking Study, over 60% of top-performing firms have a documented client value proposition. Justifying your value through visuals will assist with these approach talks.

Be prepared for every prospect meeting to demonstrate how you are different and why the prospect should hire you. Your value proposition must go beyond “We care about you.” And the value proposition must go beyond promises around investment management, as most clients cannot justify your fee based on those services only.

You must be prepared to discuss your planning services for these clients, whether that is core financial planning or additional services such as charitable planning, estate planning services or tax planning.

5. Don’t forget the all-important follow-up

Although we can sometimes close in that first meeting, we often don’t. That is where having a great follow-up procedure can be the difference between closing or not closing. Plan to follow up at least three times. And time is your enemy here, so don’t wait too long. In fact, at the end of your prospect meeting, you should peg the follow-up date, so that everyone knows what to expect. Make sure to monitor the pipeline with your team, to be sure that proper follow-up is occurring.

Closing new business requires effort, but it is a critial aspect of growing your firm. Don’t miss opportunities that could provide a big win for you and your firm.