Once your client decides to retire, their financial planning priorites change. It is time to create a new plan that addresses spending, taxes and legacy planning, among other things. Of course, often our clients don’t know what they don’t know; they may simply assume that management of their wealth during their next 30 years should be similar to what it was for the first 30 years. Nothing could be further from the truth. Below we discuss three topics to address with your client as they enter these uncharted waters of decumulation.

1. Consider your client’s long-term goals

Aside from the general financial risks and strategies to consider as a client approaches retirement, it is crucial to understand their personal goals and needs. These can play a big part in the final recommended strategy. That is why it is critical to have this conversation with your client and revisit their goals and strategies whenever you update their financial plan; situations and priorities can change.

Take the time to reacquaint yourself with your client and allow them the freedom to share their dreams with you. And when discussing their dreams, ask them, “If not now, then when?”

These questions can help clients think about their long-term goals:

- Do you want to save for any family milestones?

- Are you looking for professional advancement?

- Do you need help deciding when you want to retire?

- Do you plan to change your residency in retirement?

- Do you feel confident about your current financial situation?

After your clients answer these questions, you will understand how they want to spend their free time as retirees and accurately prepare them for the decumulation process. At TFG, we require all new clients to complete our Client Profile and Goals Checklist (sample forms shown below in Figures 1 and 2) which is included in our larger client onboarding packet. This provides information about the client’s financial goals and priorities, information that is critical to putting together a personalized financial plan.

Figure 1: The TFG Client Profile Includes Questions About Background History and Feelings About Money

Source: Taylor Financial Group

Figure 2: The TFG Client Profile Asks Extensively About Goals

Source: Taylor Financial Group

2. Understand guaranteed income

A large part of determining cash flow needed in retirement is looking at what percentage of income in retirement is coming from guaranteed income sources. Guaranteed income can include Social Security, pensions, annuities, or any income paid out that is not affected by external market conditions or factors. It is generally recommended that clients have 30%–50% on average in annual guaranteed income in retirement. This ultimately depends on each client’s situation, but this is a rule of thumb.

If we can estimate guaranteed income, we can determine what the client will need to take from their portfolio to fill the gap. From here, we can create our “liquidity” bucket with one to three years of cash or short-term bonds. We can also reallocate the portfolio into dividend-paying stocks, individual bonds when possible, and income-producing funds to create the desired level of income. We can also provide reassurance to the client when the market goes down, as we have the guaranteed income and we have already set aside funds to provide for cash flow.

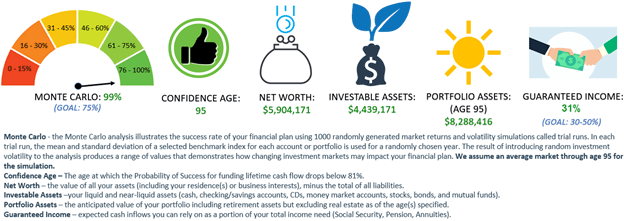

At TFG, we address guaranteed income within the financial plans we build and provide a Plan Snapshot within the meeting notes as a summary after the meeting. As you can see in Figure 3 below, the Plan Snapshot includes Monte Carlo success rate, confidence age (longevity risk), net worth, investable assets, remaining portfolio assets (at assumed age of passing), and average guaranteed income. We also include an explanation of each figure at the bottom of the Snapshot.

Figure 3: TFG Plan Snapshot Summarizes the Retirement Outlook

Source: Taylor Financial Group

According to a recent paper, “Guaranteed Income: A License to Spend” by David Blanchett of QMA and Michael S. Finke of the American College, retirees who have large annuities spend more of their nest egg and are happier. This is probably true, but it is difficult to convince a client with several million dollars to purchase an annuity to provide guaranteed income, given the many drawbacks of annuities: ordinary income tax treatment, no step-up in basis, limited access to funds, and so on. However, clients with smaller balances may be great candidates for annuities, as the guaranteed income provides a powerful benefit.

Pro tip: Are you reviewing guaranteed income with clients, so they understand what is really at risk from a cash flow perspective and what you are solving for every year?

3. Review accounts and create a tax-efficient withdrawal strategy

Another critical item to consider when developing a retirement drawdown strategy is the potential tax implications for withdrawing from each type of account. There are three types of investment accounts: taxable, tax-deferred and tax-free, and each of these accounts has different tax classifications.

- Taxable (brokerage account, capital gain on investment gains through each year)

- Tax-deferred (traditional IRA, ordinary income tax upon distribution)

- Tax-free (HSA or Roth IRA, no tax for qualified distributions)

Developing strategies to finesse these areas will be critical for proper tax efficiency. Ideally, we want the client to have some assets in each of the three buckets to create tax diversification and reduce risk.

Strategies will vary depending on income, desired retirement lifestyle, debts, savings and more. It also depends on what stage of retirement the client is in. For example, the pre-RMD stage will look different than the post-RMD stage. For the clients in a low tax bracket (10%–12%) and before Social Security benefits and RMDs kick in, Roth conversions are often a no-brainer (especially for those with large traditional IRA balances looking to build their tax-free assets for themselves or their heirs).

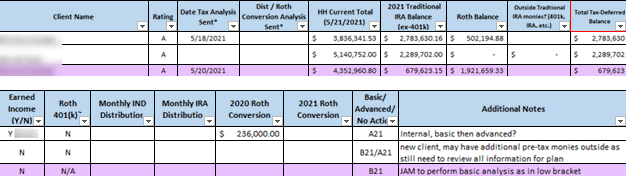

On the flip side, a Roth conversion may not make sense for a client in the post-RMD stage with high income and no heirs. Considering a Roth conversion relies on two things: your client’s current tax bracket and expected future tax brackets. And if your client is hesitant to do a Roth conversion, perhaps encourage withdrawals from a traditional IRA for monthly living expenses as another way to accomplish the goal of driving down the traditional IRA balance. The spreadsheet that we use to track these items is shown below.

Figure 4: TFG Spreadsheet Tracks Tax Withdrawal Strategies

Source: Taylor Financial Group

On this spreadsheet, we not only highlight clients with large pre-tax balances, but we also address other essential items, such as their current Roth balance, if they are working and contributing to a Roth 401(k), if they are taking distributions from their individual or traditional IRA accounts, and Roth conversions performed last year and any so far in the current year. With all this information in one place, we can determine the best way to proceed based on each client’s situation.

When a client is widowed, we must be aware of the widow’s penalty. The widow’s penalty occurs when the first spouse passes, and the living spouse will then be subject to single tax bracket rates (which are unfavorable). Therefore, changing from married filing jointly (MFJ) to single could cause a widow to be pushed into the next tax bracket or even two tax brackets higher. For example, per current tax rates, a client with taxable income of $210,000 and filing MFJ would be in the 24% tax bracket, whereas a person filing single with the same taxable income would be in the 35% bracket. Therefore, we encourage Roth conversions and recommend clients leave Roth monies to spouses so that distributions are tax-free.

Based on the above, at TFG, we encourage Roth conversions, building Roth accounts, and drawing down traditional IRA accounts to not only create a source of tax-free assets in a client’s lifetime but as a legacy planning tool to help minimize taxes for spouses and other heirs. We illustrate the power of Roth conversions by using either Holistiplan for a short-term analysis or Income Solver and eMoney for a multi-year analysis. With this, we can project two important figures: the projected difference in taxes and the value of their Roth accounts at the end of their life.

Pro tip: Are you running a Distribution Planning analysis for all valued clients, evaluating the benefits of a Roth Conversion, or taking additional IRA distributions?

Reviewing these three planning items with your clients as they enter this new chapter will adequately prepare them for this new stage in their life and ensure their heirs will be as protected as possible when Uncle Sam comes knocking.