|

Join by December 31st and Save $100!

For the Advisor Who Doesn't

Want to Do Seminars or Workshops…

Instant Social Security Expertise

|

2-Volume Set, Plus Calculators and Program

Updates… |

- Don't Get Caught Dumbfounded

When a Client or Prospect Asks About Social Security…

- Get "Financial Advisors Guide to Savvy Social

Security Planning"…

- Get "135 Social Security Questions Answered:

What Savvy Advisors Need to Know"…

- Use 4 Proprietary Calculators to Run Client

Scenarios (Download from Savvy Social Security website)…

Social Security Mastery Program Offers

Unparalleled Advisor Support for Your Tough Social Security

Cases…

Imagine Answering Clients' and Prospects'

Social Security Questions With Confidence

Deftly guide people through such thorny issue as:

- What's the best time to file for benefits and get the

highest monthly check?

- What if I file early and invest all of my benefits?

- Should I spend Social Security money or IRA money first?

- What if my wife wants to file now on my record, but

I want to keep working?

Dear Advisor:

Now you don't have to be doing

client workshops and seminars on Social Security in

order to have access to all the great expertise contained

inside Horsesmouth's Savvy Social Security Planning

for Boomers resource.

We've created a program that will

give you important insights and tools to help you help

your clients make the best Social Security decisions

possible when planning their retirement income strategy.

It's called

the

Social

Security Mastery Program.

And the program is designed for

advisors who want the best available resources to help

their clients make smart retirement income decisions—but

who don't want to put on client education workshops

and seminars as part of their business development strategy.

It's critical that you be able

to offer good analysis and insights for your clients

on this topic…It's amazing how many COSTLY, bad decisions

are being made by Boomers and many advisors…

"I Would Have Never Known

It Was Possible…"

In a minute, I'm going to tell you more about this

amazing new resource Elaine Floyd has developed to help

advisors master their understanding of Social Security.

But first I want to share an e-mail we received just

the other day. It's from an advisor in Rochester, Minnesota

named Dennis Bussian. Here's what he wrote to Elaine:

|

I want to share with you a personal experience

that I had just this past week. I have

a client where the wife is the primary bread

winner and is still working at age 66 and plans

to continue for another year or so. The husband

has been retired and drawing on his benefits.

Last week they were in and the wife just

turned 66 and I told her that she should begin

collecting a spousal benefit on him and continue

to earn delayed retirement credits on her benefits

at least until she retires and possibly to age

70.

This was almost identical to the situation

illustrated in the seminar on slide # 34. This

meant she would be entitled to about $550 [per

month] of spousal benefits.

They were surprised to learn they could do

this and obviously would never have known about

it unless I told them.

And even though I am a CFP and ChFC and have

been a financial planner for 17 years, I would

have never known it was possible either if I

had not purchased Savvy Social Security Planning.

When they called the local social security

office, they were shot down.

The local rep told them she was only entitled

to a spousal benefit if it was greater than

her own benefit. I called and got the

same answer and pushed back hard finally convincing

the representative to do a little research.

She came back and told me I was right.

This shocks me. Is this fairly common?

These clients almost lost out on $550 per month

for the next 4 years. Just wanted to let

you know that the clients are happy and the

Savvy Social Security Planning was money and

time well spent. Thank you. |

Dennis came to the rescue of his client in this case.

And that little action on his part earns them $26,500

over the next four years. Now that's the kind of thing

clients love to see from their advisors!

Sadly, of course, Dennis's experience is not uncommon

at all.

People at the Social Security office can be nice

and helpful and informed.

But it's not uncommon for them to be

misinformed about certain aspects of how

Social Security works. And that's what you have to be

on the lookout for. (It's the same reason you wouldn't

send your clients to the IRS to get an answer about

an IRA rollover question. Right?)

Clients need guidance when it comes to figuring out

exactly how Social Security fits into their retirement

income plans.

And you're the one who needs to prepare the best

analysis and options available to them.

We want advisors in the U.S. to be masters over the

ins and outs of Social Security because it's too important

to be left to your clients and unconcerned government

workers.

And that's why we've created this new resource for

advisors who are faced with answering this deceptively

simple question...

The

Ultimate Litmus Test: Here's how to Pass It

Here it is: "When should I file for Social Security

benefits? "It's the question every Boomer needs to answer.

Rich or poor. Whether they'll need Social Security to

make ends meet or whether they intend to use it to fund

an investment program for themselves or, say, their

grandkids' education. Or anything else in between.

And here's where you come in…The answer to that question

is complicated.

The distribution phase of retirement is a lot more complicated

than the accumulation phase.

As a professional financial advisor in good standing

in your community, people increasingly will turn to

you for expert help in figuring out Social Security's

role in their retirement mix.

The reason clients need your help is that there are

very few REAL rules of thumb that apply to everyone

when it comes to Social Security.

And the decisions clients make at this stage in life

depend on a multitude of factors including income, assets,

health status, life expectancy, family dynamics, life

goals, and a lot more.

Irreversible Decisions and Long-Term Effects

And unlike a lot of other decisions clients made earlier

in life,

some decisions they will be forced to make now are irreversible.

For instance:

- Starting Social Security at age

62 can cause a client to leave a lot money on the

table if they live well into their 90s.

- Failure to consider the impact

of marriage, divorce, remarriage, and widowhood

can severely pinch your clients' lifetime stream

of income…

- Failure to coordinate IRA RMDs

with Social Security taxation results in needless

diminishment of income that could be put to better

use for health care or just enjoying life.

And those are just a few key points. There are literally

millions of permutations. For every rule of thumb, there

are dozens of exceptions.

And here's the key: From the clients' perspective,

there really is no substitute for sitting down with

an advisor, spreading the papers around the table, and

talking about the clients' life and family, hopes and

fears, and developing a retirement plan that makes all

aspects of their financial and life goals work together.

But you've really go to know what you're talking about

when it comes to Social Security.

We're Not Talking Chicken Feed, Either

Social Security is a lot more valuable than most people

realize. Here are a few things to consider. First, it

is a lifetime annuity. Once you start getting it, it

keeps coming until you die.

Second, it's inflation-protected. A nice benefit, indeed,

thanks to annual cost-of-living adjustments (COLAs).

With the power of compounding, these annual bumps can

really start to add up over the years. This aspect is

often overlooked by individuals and advisors.

Third, there is right of survivorship. So when one spouse

dies, the other can continue to receive the higher of

the two benefits until they die, too.

Consider this example. In 2008, the maximum benefit

for a person turning full retirement age is $2,185 per

month. If that person lives for 30 more years, assuming

an annual cost-of-living adjustment of 2.8% (which is

what Social Security trustees project under their intermediate-cost

scenario), he or she will collect more than $1.2 million

in benefits.

As Elaine Floyd, Horsesmouth's Director of Retirement

and Life Planning says, "Given the great potential of

Social Security benefits over a person's lifetime,

it makes sense to treat this resource as a significant

asset and to make decisions that will maximize it to

the greatest possible extent."

In addition, "retirement," or whatever it may be called

in the future, will be different for the Boomers.

We already know that. Youth was different. Marriage

is different. Career paths are different. Recreation

is different. Health is different. Longevity is different.

Religiosity is different. It keeps going.

So when it comes to figuring out Social Security, that'll

be different, too. Unlike previous generations, they

won't just pad on down to the local Social Security

office and sign up.

They've got a lot of questions. Should they apply now?

What if they keep working? How will their decision affect

their spouse's benefits? A dissection of all things

Social Security is in the offing.

So how prepared are advisors to respond?

What Do Advisors Know About Social Security?

Not Enough…

Earlier this year we started thinking about the best

way to help advisors help their clients regarding Social

Security. We sensed advisors were lacking expertise

in this basic retirement income topic.

We knew anecdotally that clients often asked advisors

about Social Security. Some advisors admitted they didn't

know as much as they felt they should about the topic.

And that's a problem…

After all, when it comes to figuring retirement income

streams—regardless of your client's wealth—Social Security

is guaranteed and inflation protected. You can't disregard

it!

So we decided to conduct a survey to gauge the level

of advisor expertise and interest on this issue…The

results surprised and shocked us.

More than 85% of 1,110 advisors told us they talk with

their clients about how Social Security fits into their

retirement plans. That was good.

But when those advisors were asked to rate their knowledge

across key Social Security topics—and quizzed on fundamental

questions about Social Security—a troubling picture

emerged.

In only 1 of 8 categories did more than 50%

of the advisors rate their knowledge as "above average"

on common Social Security benefits issues!

Advisors admitted they lacked expertise in these

seven categories, saying their knowledge was average

or worse:

- How a person accumulates Social Security

benefits over their working career…

- How annual cost-of-living increases are

determined…

- How to do a breakeven analysis to determine

if a client should consider delaying benefits…

- The formula for determining how benefits

are taxed…

- How to estimate lifetime Social Security

benefits…

- How to coordinate spousal benefits for maximum

income and protection for the surviving spouse…

- How to optimize benefits taking into account

a client's age, current health status, life

expectancy, earned income, taxes, and overall

financial goals…

A brief multiple choice quiz we administered to

advisors also produced similar dismal results. We

asked:

- How much of a cut in benefits

will you take if you apply early instead of

the normal retirement age?

- If you decide to work after

starting retirement, how much can you earn before

your benefits are reduced?

- If a person begins receiving

the maximum benefit at full retirement age in

2008 and lives to age 95, how much will he receive

in total lifetime benefits, assuming an annual

COLA of 2.8%?

- True or false: Once a person

reaches full retirement age it is impossible

to accumulate higher benefits by working longer

and earning more.

- True or false: If a woman who

is receiving benefits under her former spouse's

earnings record remarries, she can choose which

spouse's record to base her benefits on.

- Which income sources are included

in provisional income to determine if Social

Security benefits are taxable?

Again, the results of the quiz were poor. In only

two of the six questions above did more than 50%

of the polled advisors answer the questions correctly…

Wow. That's a retirement knowledge crisis in my

book. And there's more…

The common questions about "When should I apply

for Social Security benefits?" is just the opening

salvo.

There are plenty of other follow-on questions, such

as these:

- Can it make sense for a spouse

to collect benefits on his/her own work record

at age 62 and then switch to a higher spousal

benefit at age 66?

- Does the fact that the spouse

starts collecting benefits on his/her own work

record at 62 negatively impact the spousal benefit

at age 66?

- If a spouse wants to wait to

collect benefits at 70, can he collect benefits

on his spouse's earnings record before then?

- If a married person who is

less than full retirement age is collecting

SS benefits and is also working, is it only

that person's earned income that determines

if benefits will be reduced or is it the joint

earned income that is compared against the earned

income limits?

- Can legitimate tax write-offs

be used against any Social Security income that

is deemed to be taxable?

- What if your client was a local

government employee, who didn't pay into Social

Security, retired early, and now is in a new

high-paying career contributing to Social Security?

You can see, it gets complex fairly quickly.

After all, clients and employers have been paying

into it for years and it's one the most successful

government programs around. And with the coming

Boomer retirement crisis, it will be even more important.

Boomers Need Advisors Now More Than Ever: And

What They Need is a Customized, Break-Even Analysis

So, where do you and your clients start?

What every person needs is a customized, break-even

analysis that takes into account their family situation,

their life goals, their other resources, and how

Social Security fits into their overall retirement

plan.

The media can't do that. And the Social Security

Administration can't do that, either. You are the

only one who can really do that because you know

your client.

Everyone wants to know how to get the most out of

their Social Security. It's a perfectly natural

response, especially when someone actually looks

at what they've paid in over the years.

Fair enough. But how do they do it?

Well, lots of people will do it on their own and

maintain a life-long pattern of making important

investment mistakes because they don't understand

the rules and how they apply to their own situation.

But for the advisor who understands the complexities

of the system and how to apply them to each client-specific

circumstance, their clients will benefit over the

remainder of their lifetime by having maximized

their monthly Social Security payments.

Simply put, Social Security represents an important

opportunity for advisors to provide advice to clients

and prospects—regardless of where they sit on the

retirement spectrum—on

an issue that affects nearly all of them, is very

complex, and yet is non-threatening because they

are not being "sold" anything.

You don't stand to gain a thing directly.

You just want them to have a more secure, comfortable

retirement….

For boomers with no advisor—affluent DIYers— Social Security is the question that will bring

them into your offices. The advisor who does

the bang-up job on this crucial question stands

a great chance of becoming the main advisor

for all their retirement planning needs.

Helping clients and prospects make the smartest

and most informed decision about Social Security

may prove to be the key that unlocks the door

to the big "IRA rollover" issue.

No advisor should be lacking for deep, up-to-date

knowledge of Social Security. That's not a super-tall

order, mind you.

Yes, at first blush, the formulas and calculations

and consequences of different options seem complicated.

But it's like anything else. You can gain mastery

of these topics in a short time and in a way

that will help your clients and build your reputation

around town as a retirement planning expert.

Introducing

the Social Security Mastery Program

When boomer prospects and clients come calling

with questions, we don't want you caught

behind the curve on this issue.

In fact, we want you to recognize the unique

role you play in clients' lives and get

ahead of the curve on the important issue

of Social Security and retirement income.

We want you, or folks on your team, to be

the "go-to" person for all your clients,

their friends, their colleagues and their

family members.

We want you to be able to lead people through

a complete and clear understanding of how

Social Security works, how it fits into

their own retirement needs, and what their

options are for when and how to collect

benefits.

It's an important leadership position for

you and your firm. And the best way

we know to do it is with Horsesmouth's

Social Security Mastery Program.

The heart of the program includes two major

resources:

The Financial Advisor's Guide to Savvy Social

Security Planning for Boomers

and

135 Social Security Questions Answered:

What Savvy Advisors Need to Know…

(And learn to run your own scenarios with four

special calculators: Simple Breakeven; Retirement

Spending Breakeven; Reinvestment Breakeven;

and Spousal Planning...)

The Financial

Advisor's Guide to Savvy Social Security

Planning for Boomers

|

|

175+ page action research report |

This 175+page action research report by Elaine

Floyd walks you through all the major aspects

of smart Social Security planning, equips you

both with business development insights for

how and why to engage clients and prospects

around Social Security, and a reference guide

that gives you mastery and competence over this

important, complicated topic. Topics include:

Chapter 1: What Financial Advisors Need

to Know About Social Security

- The retirement paradigm shift that caught

baby boomers off guard

- Why baby boomers are turning to financial

advisors for help with Social Security

- Why advisors with Social Security expertise

will be in demand

- 4 reasons why the financial services

industry has downplayed Social Security,

to its disadvantage.

- Why now is the time to gain Social Security

expertise

- How Social Security planning can help

build your business

- Why Social Security planning helps you

better serve existing clients

- How Social Security expertise will attract

new, unadvised (or poorly advised) baby

boomers to your practice

- 3 key benefits of being a Social Security

expert

- How to position yourself as an expert

on Social Security

- How to write your positioning statement

that focuses on Social Security

- How Social Security planning opens the

door to additional products and services

- The niche potential of being an expert

on Social Security

- Working with centers of influence, such

as CPAs and estate-planning attorneys

- Preparing for clients who are turning

62

- Understanding why the lifetime value

of Social Security is far greater than most

people realize

- Correcting boomer misimpressions about

Social Security

- Why each client's case must be analyzed

individually and coordinated with the rest

of a client's financial and life plan

- The reality of Social Security reform

and the opportunity it presents to advisors

- 4 keys to planning your initial consultation

Chapter 2: The Role of Social Security

in a Client's Overall Retirement Plan

- Why clients need your help with Social

Security before they can figure out the

rest of their retirement income plan

- Guidelines for developing a retirement

income plan

- What percentage of total retirement

income will Social Security represent

- How does the nature of Social Security

income inform the rest of a client's retirement

income portfolio

- Clients' and advisors' main concerns

about Social Security

- Setting insolvency fears aside and understanding

the program as it exists today

- 4 key points on why replacement ratios

oversimplify the retirement income planning

process

- 8 crucial items to consider when determining

retirement income needs

- 4 risks that will increase spending

needs in retirement

- The four-legged retirement stool

- Why planning for the longest life expectancy

makes sense

- Annuity income versus lump sum: common

misperceptions

- Why the annuity is worth more than a

lump sum for half of all people

- 4 key decisions clients need to make

at the onset of retirement

Chapter 3: How Social Security Works

- Social Security is not a giant pyramid

scheme; find out the crucial element that

makes it work through the generations.

- Understanding the math: How a high-earning

client could contribute $230K over a lifetime

and possibly collect $1.7 million in benefits.

- Why it's important for clients to understand

the essential nature of Social Security

regarding current benefits and current contributions.

- How to determine basic eligibility

- How wages are indexed for inflation

- How benefits are calculated based on

a formula that takes into account the highest-earning

35 years

- What the "drop out years" are (hint:

they have nothing to do with the hippie

movement).

- Computing the primary insurance amount

(PIA)

- Why the PIA isn't the actual amount

people receive. How to compute the actual

benefit from the PIA

- Maximizing benefits: The key objective

of Social Security planning.

- The compounding effect of COLAs on the

PIA

- Warning: The monthly benefit may be

higher or lower than the PIA depending on

when a person applies.

- Why taking benefits immediately upon

attaining eligibility is not always a good

idea

- Understanding the reduction in benefits

for baby boomers born between 1946 and 1954

- Spousal benefits: One of the most unappreciated

aspects of Social Security.

- What happens if a spouse lacks a 35-year

earnings history

- 10 key points about spousal benefits

- 4 tests for receiving spousal benefits

when you're divorced

- How working affects benefits

- What happens to withheld benefits for

retirees who work

- How to avoid "cash-flow shock" from

withheld benefits

- How to handle "special payments" for

work done prior to receiving Social Security

- Why benefit reductions due to the earnings

test are not truly lost

- How COLAs affect benefits

- Who is affected by the Windfall Eliminations

Provision—Help clients avoid a rude awakening.

Chapter 4: Boosting Benefits by Increasing

Current Earnings

- What everyone needs to know about getting

the highest Social Security benefits

- 3 groups of clients who especially need

to hear about how to boost benefits

- Why under-saved boomers need to understand

how Social Security benefits are computed

|

|

|

175+page action research

report |

- What the Social Security wage base means

for younger clients and the huge effects

slightly higher earnings have on Social

Security benefits

- Warning: Women who took time out of

the work force to raise children may have

set themselves up for dramatically lower

benefits. Here's how to fix it.

- Why some women need to focus on improving

their earnings now in order to substantially

increase their retirement income

- What clients who work during retirement

need to know about how and when their annual

benefits are recomputed

- Watch out: Self-employed clients who

incorporate their small businesses in order

to avoid paying the high SE tax may be setting

themselves up for drastically lower benefits

in retirement. Find out how to properly

analyze their situation.

Chapter 5: When to Apply: Strategies

for Maximizing Lifetime Benefits

- How delaying the onset of Social Security

results in a higher benefit for life

- Factors to consider when deciding when

to apply for Social Security

- Key elements of personalized, customized,

breakeven analysis

- Plus, simple breakeven analyses samples

that help clients easily grasp the concept

- Why considering spending needs is a

more realistic way to analyze the breakeven

issue

- Calculating a client's breakeven age

if benefits are spent

- Calculating the breakeven age if benefits

are invested

- Special advice for married couples

- The importance of incorporating annual

COLAs into your breakeven analysis

- The truth about early retirement: Why

the early eligibility age was lowered to

62 and what it means for the average retiree

- How the "wealth effect" has been influencing

early retirement decisions and why it should

be replaced with the "breakeven effect"

- Warning: Irrational fears and bad information

may be driving people to choose early retirement.

What they need from their advisors is a

rational "breakeven" analysis of their options.

- 4 key factors to review when conducting

a breakeven analysis

- Why baby boomers between 62-65 should

take the "earnings test" before deciding

to file for early benefits

- Longevity and the COLA compounding effect

- Why married couples need to carefully

coordinate their decisions about when to

file for benefits

- How long does a client have to live

to make it worth delaying benefits?

- Common wisdom is that you should retire

at 62 to take early benefits and delay drawing

down personal assets, right? Wrong! Find

out why.

- Taking early retirement and turning

Social Security benefits into an investment

program for wealthy clients only makes sense

under certain expected outcomes.

- What to consider if a client is considering

taking early benefits in order to leave

assets invested

- Once you start receiving early benefits,

you're stuck forever at the lower benefit,

right? Wrong! It is possible to reverse

your decision. See the details.

Chapter 6: Coordinating Spousal Benefits

- Understanding the challenge of coordinating

benefits for couples.

- Maximizing benefits for the survivor,

who may live 20, 30, or 40 more years

- Understanding the unique rules for spouses

- Estimating benefits for each spouse

- Determining when the husband and the

wife should each apply for their respective

benefits

- What happens when one spouse dies

- How survivor benefits affect decisions

that must be made now

- What happens when a surviving spouse

remarries

- Why spousal benefits may play a bigger

role for the clients of financial advisors

than for the average low- to moderate-earning

couple

- Why you must know the rules for spousal

benefits and become familiar with strategies

for maximizing spousal and survivor benefits

- Did you know that spousal benefits are

not restricted to the low-earning spouse?

Even a high-earning spouse planning to retire

at 70 can apply for his or her spousal benefit

at 66.

- Common strategies for coordinating benefits

for spouses

- Warning: When a person applies before

full retirement age, the actuarial reduction

will apply even if the person switches over

to a different benefit later (spousal benefit

to earned benefit or vice versa). Understand

why.

- Understand the playoff between filing

for a reduced spousal benefit versus applying

for one's own reduced benefit versus waiting

and filing for full benefits

- Did you know: If a husband wants to

earn delayed credits, he can file for benefits

at FRA but request that they be suspended

until he turns 70?

- Why it never pays to apply for a spousal

benefit after FRA

- Why a high-earning husband with a shorter

life expectancy should delay claiming benefits

until age 70

- Key: Remember that for married couples

the life expectancy of the second spouse

to die is what counts in planning.

- Learn how "file and suspend" works

- How to respond to Social Security personnel

who are not familiar with file and suspend

- Three key choices the lower-earning

spouse faces

- How to coordinate benefits when spouses

are different ages

- How to compare optimal benefits when

spouses are more than 10 years apart in

age

- How to plan for a possible gap in survivor

benefits

Chapter 7: Women and Social Security

- The triple whammy many women face in

retirement

- Why singling out women for Social Security

planning is important

- Why women really need Social Security

planning—and why men should care

- How Social Security benefits women

- What all women need to know about Social

Security

- How a husband's decisions affect a woman's

Social Security benefits

- How to claim benefits from a divorced

spouse

- How remarriage affects benefits

- What women can do now to increase their

Social Security benefits

- Essential Social Security planning for

women of all ages

- Why Social Security planning inspires

people to do comprehensive survivor planning,

including insurance, investments, and estate

planning

- Which is greater: earned benefit or

spousal benefit?

- 4 key questions to answer when projecting

benefits

- 6 possible scenarios to consider

- Understanding the rules for earned benefits,

spousal benefits, divorced-spouse benefits

and survivor benefits.

- What if you divorce in retirement

- Why it is important to report all marital

events to Social Security

Chapter 8: Taxes on Social Security

Benefits

- How taxes on Social Security benefits

are calculated

- The impact of these additional taxes

on a client's effective tax rate

- How taxes drive decisions on how much

other income a client may choose to receive

- Which types of income are exempt from

the formula

- How to plan ahead for IRA required minimum

distributions at age 70-1/2

- Clear disincentives not to earn more

income in retirement

- The marginal tax rate red zone

- Avoiding excess tax: One more reason

why it may pay to delay Social Security

benefits.

- Tax considerations for clients who plan

to work in their 60s

- Tax issues for clients who plan to retire

before age 70

- 6 keys for coordinating income and spending

needs

- Reduction in benefits vs. taxation of

benefits: helping clients understand the

difference.

Chapter 9: Other Social Security Programs

- Dependents' benefits: Why Donald Trump's

toddler son could even receive Social Security.

- Understanding the maximum family benefit

(MFB)

- How the MFB is computed

- Why you must always ask about grandchildren

- How the earnings test applies to dependents'

and survivors' benefits

- Remember: Taxation applies to dependents'

and survivors' benefits.

- How a person becomes eligible for disability

benefits

- Social Security's strict definition

of disability

- Understanding the lag time before benefits

begin

- 3 key planning issues

- Supplemental Social Security Income:

Rules for qualifying.

Chapter 10: Medicare and Long-Term Care

- Why every client will need a crash course

in Medicare sometime before turning 65

- Warning: If clients don't apply for

Medicare in a timely manner, penalties will

be applied to future Part B premiums.

- Understanding the alphabet soup that

is Medicare: Parts A, B, C, and D

- The 3 most important things to understand

about Medicare

- How Medigap policies work

- Medicare and the long-term care myth

- Options for long-term care

- What to consider when choosing a long-term

care policy

- 9 key points to consider when choosing

policy features

- Ways to protect against inflation in

long-term care costs

- How Social Security planning integrates

with Medicare and long-term care

- Warning: One of the most important services

an advisor can provide to baby boomers is

to help them avoid penalties and gaps in

health care coverage by enrolling in a timely

manner.

Chapter 11: Mechanics of the Social

Security Program

- How and when to apply for Social Security

benefits

- Know the exact month and day people

should apply in order for benefits to start

- How and when checks are received: automatic

deposits make it easy.

- 27 questions clients will need to answer

when applying in person or online

- Documents clients will need to produce

at the time of application

- When applying in person is productive

- What every widow needs to do when a

spouse dies

- What every widow should consider before

applying for survivor benefits

- What survivors need to bring to the

Social Security office

- Warning: Errors are not uncommon in

computing benefits. Overages will be collected

at a later date.

- What do with Social Security payments

made to a deceased spouse. Warning: Benefits

may be stopped for up to 24 months for intentional,

false statements

- What to do when changing bank accounts

and redirecting direct deposit.

- Watch out: Marrying and divorcing while

receiving benefits can change calculations.

- Death of a beneficiary and what to about

payments received after death

- How benefits are withheld if a client

earns more than the earning test amount

- What type of income counts toward the

earnings test

- Why self-employed people who retire

will be scrutinized to make sure they are

not just reporting a lower salary while

still working or receiving other compensation

- Figuring out taxes and Social Security

- How to get taxes withheld

- How to appeal a decision

- The four levels of appeal

- Special rules for clients living outside

the U.S.

Chapter 12: History

and Financing of the Social Security System

- Understanding the Social Security trust

fund

- The difference between the Social Security

trust fund and the assets of the U.S. government

- The future of Social Security

- Understanding how the Social Security

trustees make 75-year projections

- When expenses exceed revenue: what really

happens

- Three ways the actuarial balance is

expressed

- Building sufficient trust fund reserve

- Explaining the actuarial balance

- Why immediate cash infusions aren't

required

- The history of the actuarial deficit:

why Congress doesn't always need to act

immediately

- 14 ways Social Security could be reformed

in the future

- How Social Security reform is likely

to affect baby boomers approaching retirement

- How to incorporate possible Social Security

reform into your long-term planning with

clients

Don't miss this chance to get the Horsesmouth

Social Security Mastery Program.

Go ahead and learn more now!

135 Social Security

Questions Answered:

What Savvy Advisors Need to Know

Every day Elaine Floyd spends time researching

and answering tricky, perplexing, contradictory

and generally vexing Social Security questions.

It's the nature of the topic…

In case you didn't know, Elaine's the leading,

independent expert on Social Security payout

questions. Even the Wall Street Journal

turns to her for answers…

Now she's edited and sorted

a year's worth of the best questions. And they're

available to you now to boost your Social Security

mastery.

Here's the overview of what's covered and

some questions to give you an idea of what you'll

find.

- When to apply - questions 1 - 9

- How working affects benefits - questions

10 - 24

- Spousal benefits - questions 25 - 70

- Survivor benefits - questions 71 - 95

- Divorced-spouse benefits - questions

96 - 117

- Taxation of benefits - questions 118

- 123

- Miscellany - questions 124 - 135

Here's a peek at some of what's addressed

in this new report:

|

|

Answers to real-life questions…

|

When to Apply

The most fundamental question facing baby

boomers is when to apply for benefits. It's

not 65 anymore. Full retirement age for boomers

is 66.

But Social Security benefits may be claimed

anytime between the ages of 62 and 70. It is

crucial for boomers to understand how claiming

early benefits will reduce their benefit (for

life) and delaying benefits will increase it.

Most advisors understand this, so most of the

questions here relate to the "repay and reapply"

strategy (also known as the "do-over"), and

other miscellany…

Among the questions answered are:

- I presented a seminar last evening

and have a question relating to disability.

The wife has been disabled since age 50,

not sure of current age, but the husband

worked to age 68 and will be turning 70

this year. He has not yet applied for benefits.

His wife is getting $618 per month. When

he applies for his benefit at age 70, can

she receive or substitute the DI benefit

for the spousal benefit if larger? The husband

was a government employee so he was aware

of the offset. Any suggestions?—David P.

- When a parent is age 62 or older

and begins collecting Social Security

and still has minor age children, do they

receive any benefits at that time? Does

the adult have to file for and receive Social

Security for the benefits to start?—John

F.

- We may have run across a client

who never applied for Social Security

and is 80 years old. He owns

a successful business and didn't "need"

the extra cash. We are still gathering

facts. Can he apply for retroactive benefits?

If he applies now, will his benefit include

an adjustment to make up for the lost $$$?

Does he simply lose those benefits not taken

since age 70?

- Is it possible to do a "do-over"

for both survivor benefits and

spousal benefits?—Toby G.

How Working Affects Benefits

"What if I keep working?" is the most commonly

asked question by clients today. Everyone knows

there is some rule about Social Security benefits

being withheld if they work, but many clients

are unclear about the details. The basic earnings

test is pretty straightforward—for anyone under

full retirement age (FRA), $1 in benefits is

withheld for every $2 earned over $14,160 in

2009 and 2010—but as with anything related to

Social Security, there's more to it than that.

One area of confusion relates to the re-computation

of benefits at FRA…

Among the questions answered are:

- Client is age 62-1/2. Retires

July 2009 and begins receiving Social Security

benefits August 2009. Opportunity

comes along for independent contractor employment

from former employer. Monthly independent

contractor income will be about $2,200 a

month for remainder of year (4 months).

Will Social Security benefits be reduced

because monthly income (self-employment)

will be greater than $1,180/month ($14,160

/ 12 months)? Isn't the yearly maximum broken

down to a monthly maximum?—Linda

- Just to confirm, after a beneficiary

has reached FRA, the benefits will no longer

be subject to reduction due to other income,

but the benefits will forever be

subject to taxation, even into their 90s.—Andrew

- If someone reaches FRA and takes

SS but is still working and makes a lot

of money, can their present earnings

increase their benefit in the future, or

is the benefit frozen once they start taking

SS?—Debra

- I have a couple, both age 62,

where the husband plans to continue to work,

possibly to age 70. The wife is

considering going ahead and taking her Social

Security reduced benefit now. If she does

so, does the income limit before benefits

are reduced apply to just her income, or

to their joint income since they file jointly?

What other considerations do we need to

pay attention to?—Kevin J.

- Is non-passive income from an

S corp considered earned income

for SS taxation between age 62-66?—Michael

- I have a couple who received

conflicting advice from Social Security

(two different answers on two different

visits) and they came to me for

"the right answer." The issue is interpretation

of the working spouse drawing her benefits

at age 62 (husband continues to work until

NRA and they're the same birth year) and

taxation of those benefits because they

file jointly and there is earned income

pushing them over the earnings threshold.

One SS worker told them that she should

wait because her benefits would be subject

to the earning test because they file jointly.

She'd receive the benefit but it would be

reduced 3 to 1. Another SS worker told them

earning test only applies by Social Security

number and the joint filing doesn't matter.

They don't know which to believe and are

hesitant to file until they know which is

correct. I can't find a definitive answer

to this issue on SS website. Which one is

correct?—Larry F.

Spousal Planning

|

|

|

Answers to real-life questions… |

By far, the most complex area of Social Security

planning is spousal planning. The vast majority

of questions that come to us have to do with

this complicated area of Social Security planning…

Among the questions answered are:

- If the primary worker's benefit

at FRA is $2,000, the spousal benefit

would be $1,000. If the primary

worker delays benefits until age 70 and

his benefit is $2,600, would the spousal

benefit be $1,300? Or does it top out at

$1,000, which is half of FRA?—Andy U.

- The more I deal with Social

Security, the more I realize there is to

understand. Can I assume

a wife can take a spousal benefit at 62

if it is higher than her own benefit and

then switch to her own benefit at any time

after her FRA if her own benefit is higher

at that point? Is the alternative also possible

whereby she takes her work benefit at 62

(because it's higher) and then changes to

a spousal benefit sometime after FRA if

the latter benefit is higher? I guess the

key thing you're telling me is that a spouse

will receive the higher of either her spousal

or her own benefit before FRA, and if she

starts her own benefit early, she is stuck

with that unless her spousal benefit at

some time becomes higher.—John G.

- Let's say a wife starts to collect

on her husband's Social Security at age

62. He applies for his benefit

but doesn't actually take it. He starts

receiving his benefit at 66. When he passes

away, does she jump up to the amount he

is receiving, or will she always get a little

bit less because she started collecting

early at 62?—Joe C.

- If the wife is 66 and the husband

is 65, can the wife apply for spousal benefits

on the husband's record? Can he

file and suspend in order for his wife to

receive spousal benefits at her age 66 or

does she need to wait until her age 67 and

his age 66?—Ron C.

- I recently called the Social

Security office to inquire about drawing

my spousal benefits after I turn 66

in September of this year. My wife

is 64 and has already filed for her retirement

benefit based on her work record. It is

my intention to file and suspend and draw

spousal benefits based on her work record.

The person I talked to at the Social Security

office was familiar with the file-and-suspend

procedure but stated that my wife had to

be age 66 (FRA) before I could file for

spousal benefits on her work record. Is

it time to ask to speak to a Title 2 Technical

expert or a Title 2 Claims representative?—Sam

K.

- Can file-and-suspend be used

by the lower-earning spouse to enable the

higher-earning and older spouse to get extra

benefits? For example, the higher-earning

husband is 66 and will work to 70. The lower-earning

wife is 62 and will work to 66. Can the

lower-earning wife file-and-suspend and

the higher-earning husband take four years

of spousal benefits without impacting his

own benefit at age 70?—John E.

- If a person was a teacher before

retirement, and covered by a state teachers

retirement plan, she is not eligible

for Social Security. Does that regulation

apply for spousal benefits as well?

Survivor Benefits

Survivor benefits are one of the most valuable

and important aspects of Social Security. It

has been estimated that the average survivor

benefit is equivalent to a life insurance policy

with a face value of $433,000. Maximizing the

survivor benefit is a crucial aspect of Social

Security planning for married couples, and it

is important to stress to clients that the amount

that stands to be paid far in the future depends

on decisions made today….

Among the questions answered are:

- If a wife takes her retirement

benefit before FRA, does that reduce her

survivor benefit if he delays his benefit

to 70?—Alan

- A wife works and gets a small

Social Security benefit. Her husband is

retiring from the government as

a CSRS employee. When he dies, she will

get his government pension survivor benefits.

Will that reduce her SS benefit?—Steve R.

- I was hoping you might be able

to help me with a situation I have with

a client. She's 62 and works full time.

Her husband passed away and she is entitled

to his benefit, which is lower than her

expected benefits. My question is this:

Even though she's working and would be penalized

for receiving Social Security, doesn't it

still make sense to obtain the benefit from

her deceased husband? Doesn't that benefit

go away once she reaches her full retirement

age?—Peter S.

- Widows/widowers who do not remarry

are entitled to survivor benefits at age

60, but SS does not remind them

or clearly spell this out on the website.

Benefits not applied for on time are lost.

Must be a common oversight saving the system

lots of money. Thoughts?—Bill

- In a "file-and-suspend" where

the non-earning spouse takes her spousal

benefit and higher earning spouse dies

before filing at age 70, what will survivor

benefit be based on?—Rick

|

|

|

Answers to real-life questions… |

Divorced-Spouse Benefits

Financial advisors are going to have to start

prying into their clients' marital histories.

Why? Because it may not even occur to clients

who have been divorced for many years that they

could be entitled to divorced-spouse benefits

or divorced-spouse survivor benefits. When clients

apply for Social Security, they will be asked

about previous marriages…

Among the questions answered are:

- If a divorced spouse starts

drawing SS based on the ex-spouse's earnings,

does this reduce the ex-spouse's benefit?—Steve

- Does a former spouse drawing

benefits on an ex-husband's PIA affect his

current spouse's benefit?—Anonymous

- A divorcee age 65 plans to wait

until age 70 to collect SS benefits. Her

former husband is 67. He is still

working and she has no way of knowing if

he is collecting on his SS benefits. Can

she receive a spousal benefit now? Will

it interfere with her future SS benefit

at 70?—John

- If a woman is divorced and has

remarried, how is the PIA determined? Is

it based on the second husband's income

history, or a combination of the

first husband and second husband's income

history? Does the wife have the option to

choose between the two?—Paul

- I have lots of questions regarding

applying for benefits post divorce. Here

are a few that puzzle me.

The situation: Wife is 62, ex-husband is

65. Divorce is final 12/1/09. 2 years after

final decree would be 12/01/11. At that

time the unmarried wife will be 64 and the

ex-husband will be 67. He is still working

and doesn't plan to collect benefits until

age 70. Wife's full benefit at age 66 is

$785. Ex-husband's full benefit at age 66

is $2,341. Can the wife apply for her benefits

now (getting only 75%) and wait to apply

for her divorced-spouse benefit until her

husband applies? Or does applying for hers

now automatically lock in the % of what

she could get from his benefits?—Debbie

- If my divorced client waits

until FRA to take her divorced-spouse benefits

but her ex-husband claims his benefit at

62, is she forever locked into

50% of his reduced benefit? She's a teacher

making about $40,000 a year.—William D.

Taxation of Benefits

Taxation of benefits comes into play when

you are putting together an overall retirement

income plan that includes other sources of income.

Most clients of financial advisors will need

to be concerned about taxation of Social Security

benefits, since the income thresholds are so

low. Many clients will simply have to resign

themselves to having 50% or 85% of their Social

Security benefits subject to federal income

tax. Still, Savvy Social Security planning would

call for some degree of taxation analysis, especially

if clients' income is at or near the threshold…

Among the questions answered are:

- If the client goes over the

threshold for taxation, are they taxed on

the very first dollar of benefits received?—Josh

- I truly enjoyed your presentation

on Social Security! We have a client

that is currently 63 and collecting unemployment

income, severance pay until 8/31/09,

and then would be eligible to collect her

pension as well as receive a lump sum in

September 2009. Her FRA is 66. I realize

that you would need much more information

to advise when the client should begin Social

Security however I was hoping you could

confirm what income is counted toward the

maximum earnings in relation to taxation.

This is an excerpt from the Social Security

website: We do not count income such as

other government benefits, investment earnings,

interest, pensions, annuities and capital

gains—Jackie

- If you take a distribution from

a Roth IRA is the distribution included

to calculate the taxability of Social Security?—Barbara

Miscellany

Among the questions answered are:

- Are COLAs higher the longer

you wait to start SS?—Mark

- Many of my clients will receive

PERA benefits and this, I hear, reduces

SS benefits. Is there a formula

I can use in planning with these clients?—Carol

- If you take SS early, do they

prorate the amount by month (62 and 3 months)

or just by year (62, 63, etc.)?—Luella

- If an individual wants to reimburse

Social Security for the benefits he's received

in order to restart his benefit

at his current age, is he also responsible

for repaying benefits received by a dependent

under his Social Security number?—Laurie

- What can be done if people are

already taking SS benefits? Can they still

be helped?—Bob

Don't miss this chance to get the Horsesmouth

Social Security Mastery Program.

Go

ahead and learn more now!

Savvy Social Security

Calculators

Savvy Social Security

Calculators (Download from Savvy Social Security website):

Elaine Floyd has developed four proprietary

calculators that provide important flexibility

and insight into

Social Security planning scenarios on four

special topics: Simple Breakeven, Retirement

Spending, Reinvest Breakeven, and Spousal Planning

-

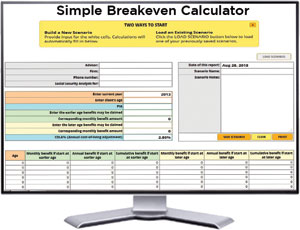

Simple Breakeven

Calculator—This basic calculator

helps you advise clients on when to apply

for

Social Security benefits. It allows

you to run two scenarios— apply earlier

and receive a smaller amount, or apply later

and receive a larger amount. The calculator

shows the age the client must live beyond

in order for delayed benefits to produce

a higher cumulative amount. This calculator

is designed for simplicity and does not

take into account investment returns if

benefits are invested.

- Retirement

Spending Breakeven Calculator—This

calculator assumes the client has personal

assets in addition to

Social Security. If the client retires

sometime between the ages of 62 and 70,

should he apply for

Social Security immediately and leave

the personal assets invested, or should

he draw from the personal assets first and

wait to apply for

Social Security in order to build delayed

credits? A year-by-year run shows how much

of each year's spending need is met by personal

assets vs.

Social Security. The objective is to

determine which strategy (early or later

filing) requires the least amount to be

drawn from personal assets to meet the same

spending need.

- Reinvest

Breakeven Calculator—This calculator

is designed for high-income clients who

will not need

Social Security to meet living expenses.

If their intent is to invest their monthly

benefits, should they apply early and get

those benefits invested as soon as possible,

or should they delay their application in

order to receive a higher benefit? At varying

return assumptions, the calculator shows

the year-by-year results and cumulative

totals so you can see the crossover point,

or breakeven age, at which delaying benefits

produces the higher total amount.

- Spousal Planning

Calculator—One of the most challenging

aspects of

Social Security planning is coordinating

spousal benefits, especially when the spouses

are of different ages. This simple calculator

allows you to enter each spouse's age and

respective benefit amount, along with the

projected COLA, and see a year-by-year run

of the couple's combined benefits and the

cumulative total. Five identical worksheets

allow you to try out several scenarios (wife

applies at 62, husband applies at 66; wife

applies at 66, husband applies at 70; and

so on), so you can see what their combined

benefit would be in 2013, 2014, 2015, etc.

Don't miss this chance to get the Horsesmouth

Social Security Mastery Program.

Go ahead and learn more now!

Stay Informed and Updated on Key

Social Security Issues

PRIVATE WEBSITE

ACCESS

-

SavvySocialSecurity.net website

gives you instant access to all the

program's materials, plus easy access to

asking questions.

WEBINAR AND

NEWSLETTERS

- Special, occasional webinars and

bi-weekly newsletter help you stay

abreast of new developments in Social

Security and stay informed about tricky

case filing issues.

Your Path to

Greater Expertise

In a perfect world, your clients wouldn't

be confused or concerned about Social Security.

They could just schedule an appointment

at the local Social Security office and

then pad on down there to easily resolve

any questions or issues.

But it's not that easy or simple. First,

Social Security is the epitome of a large,

unwieldy—some would say unresponsive—government

bureaucracy.

Second, Social Security should not be viewed

in isolation. The hard issue of retirement

income replacement needs to be analyzed

in a highly personalized, one-on-one manner,

one that takes into account all of a person's

sources of retirement income. Social Security

can't and won't do that.

Third, your clients will crave "Peace of

Mind" regarding their retirement. Having

received a personalized, break-even analysis

of their Social Security decision will go

a long way toward engendering that warm,

positive feeling clients seek.

Putting aside do-it-yourselfers, people

are going to need and seek out advice on

this crucial issue. Financial advisors are

the professionals best positioned and equipped

to address these issues for clients and

prospects.

That's why I urge you to purchase

Horsesmouth's Social Security Mastery Program

and get

The

Financial Advisor's Guide to Savvy Social

Security Planning for Boomers, 135 Social

Security Questions Answered, and 4 proprietary

calculators.

Why You Need The Social

Security Mastery Program

1) You Need to Master the Social Security

Debate Issues. Over the coming months and

years, Social Security will gain increased prominence

as an issue that transcends Washington politics

and takes root as a key, nitty-gritty issue among

many of your clients.

You'll be called upon to express a knowledgeable

and considered opinion on this key aspect of retirement

income replacement. It's no longer viable—indeed,

probably unwise—to subscribe to the notion that

Social Security is "broke" or won't be there for

clients.

Horsesmouth's

Social Security Mastery Program will

help you achieve and maintain mastery over this

crucial client retirement issue.

2) Your Clients Need Help. When

you lead your clients through the principles in

The

Financial Advisor's Guide to Savvy Social Security

Planning for Boomers both of you are

accomplishing important goals. Your clients

will have experienced a real sense of accomplishment

in reviewing their Social Security earnings record,

analyzing their potential benefit options, and seeing

how the replacement income fits with their other

resources. More than nearly all client events, knowing

and understanding how Social Security works and

fits into their lives will be concrete, real-life

information.

For you, the advisor, the activity of leading people

through the program confers "expertise by action."

You'll be demonstrating your professionalism, showing

people the value you add to the advisory relationship,

again, in a real-life scenario. It's a client meeting

with an important outcome.

3) It's a Retirement Income Opener:

Social Security, of course, is just one piece of

the retirement income puzzle. By getting clients

into a meeting or event to look at their personal

situation with Social Security, they're also getting

a real-world view of the total retirement income

picture. It all seems a lot more real and a lot

less abstract and theoretical. While focusing on

the "income replacement" aspect of Social Security,

it naturally begs the question of what specifically

the other pieces of their retirement income puzzle

will be?

The demonstration of your high interest and expertise

in the Social Security issue—and your position as

the person who has solutions to common retirement

income problems—means, naturally, that people will

see you as a good person to turn to and recommend

to others for the bigger retirement income issues,

as well.

4) It Will Elevate Your Position Within

Your Community: When you present the ideas

in " The

Financial Advisor's Guide to Savvy Social Security

Planning for Boomers" you'll actually

be doing a public service. People need this information.

They want to know more about the program that they've

contributed to through every paycheck they've ever

received throughout their entire lives. And they're

not going to find anywhere else—either online or

at the local Social Security office—the kind of

information that you'll be giving them.

Your status and reputation within your community

will be enhanced through your delivery and mastery

over the Savvy Social Security information.

People will be gratified and appreciative that you've

taken the time to learn this issue and make available

to them the opportunities to learn more.

5) You're the Expert. Stay That Way.

We already know that operational Social Security

knowledge is fairly low among advisors. Many indicated

they want to learn more because they see it as a

real need—they've had questions over the years and

answered them, perhaps, in fits and starts, not

with the kind of confidence they'd prefer and that

people should expect from a financial professional.

By committing to following

The

Financial Advisor's Guide to Savvy Social Security

Planning for Boomers, you're covering

yourself on an important topic.

As long as you remain in this business, people will

have questions about this topic and your wisdom

and insight will be sought for that reason. There

is no better way to ensure that you achieve a high

level of understanding about the key Social Security

issues your clients and prospects face than by following

the principles in

Social

Security Mastery Program.

Special Offer: Social

Security Mastery Program—Save $100

We are offering

The

Financial Advisor's Guide to Savvy Social Security

Planning for Boomers,

135

Social Security Questions Answered, four important calculators (download from Savvy Social Security website), and program updates

for only $397 (plus shipping)— a $100 savings.

I think that's an extraordinary value for the price

— considering the importance of the topic and the

amount of business you stand to gain from sharing

this essential information with clients and prospects.

It's been a difficult period for advisors all around

and I really want the good folks in this industry

to start looking ahead to the end of the recession

and start thinking about what good, positive things

can happen in 2014.

Normally, this complete program would cost you $497.

But now you can save $100 by ordering the today for

$397. Act now to gain mastery and expertise about

the crucial retirement income replacement issues

your clients will face in the coming days and weeks

and years.

What Your Colleagues

Say About Savvy Social Security Planning

Another Tool in

Advising Clients on Income Planning

"A 60-year-old prospect came to the office because

his 73-year-old wife had just been diagnosed with

cancer. He wanted to retire so he could stay home

with her. He wanted us to develop an income plan

which included his savings, her Social Security,

his company pension and what he could expect at

ages 62, 66 and 70 from his Social Security. The

analysis showed he could retire immediately, wait

until age 70 to maximize his Social Security and

have enough income until then from annuitizing two

of his annuities.

"Knowledge of Social Security provides another tool

in advising clients on income planning." —Darrill

Beebe, Arlington, TX

Changed My Clients' Lives

"A client who had been married twice was unaware

that she could receive spousal benefits on her first

husband. This knowledge helped her plan a better

retirement since her SS benefits were less than

half of his.

"Another divorcee who was dating someone on a small

SS benefit, did not realize that she could file

for a spousal benefit on her ex if she remained

unmarried.

"The information I was able to provide ended up

changing their lives." —Timothy C. Ebert, Winston-Salem,

NC

It Was A Great Idea

"I explained to a couple that she could take half

of her husband's SS for several years, postponing

her SS benefit and letting it increase in value

8% per year.

"They didn't know they could do this and thought

it was a great idea." — Lisa Winward, Salt Lake

City, UT

A Pleasant

Surprise

"I had a prospect who couldn't make it to any of

my seminars call me with a question. He said he

was 66 years old, his wife was 78 and collecting

Social Security. He was still working and wanted

to know if he could delay his SS benefits until

he stopped.

"I informed him that he could continue to work,

file for a spousal benefit now, and let his own

benefit accrue 8% credits until age 70, when he

could switch to this higher benefit.

"He was pleasantly surprised and grateful for the

reprive. Without Savvy Social Security, I would

not have been as well-versed in that prospect's

financial planning options." — Carl Janasiewicz,

Kingston, NY

Invaluable

Training

"I have found that a good percentage of clients

plan to take SS early as possible.

"This comes without any awareness or thought given

to some of the consequences and effects on beneficiaries

that may have.

"My training has helped me assess my clients overall

financial and family situation and advise them if

taking SS early is the best way to go. Consequently,

I have changed some of my clients' plans to take

SS early as a result. In many cases this has a significant

effect on their financial status." — Alfred Kulig,

Kettering, OH

Able To Make A Difference

"I have helped several widows who have lost their

husbands at a relatively young age, and had either

forgotten or simply did not know they could be eligible

for the spousal benefits.

"This has occurred multiple times.

"Is it disheartening to realize how many struggling

beneficiaries are unaware of their options. In this

case, thanks to Elaine's program, I was able to

make a difference."

— Philip Rongo, Lebanon, NJ

The Competitive

Edge

"Knowledge regarding Social Security definitely

creates an impression on prospects and differentiates

me from other advisors. I have heard the comment

‘My other advisor doesn't have a clue about this

stuff; I wonder what else he doesn't know?'" — David

Gentry, Richmond, VA

The Best Story Is My Own

"Probably the best story is my own. Until going

through your program, I was pretty much convinced

that I would take SS benefits this year, but after

going through scenarios based on my and my wife's

(who is 6 years younger) benefits it became clear

to me that waiting as long as possible is the wisest

move.

"Our combined SS income could reach over 80K a year.

And her survivor benefit increases more than 50%."

— John Tarr, Madison, Mississippi

Great Instant Credibility

"We had a client couple move to GA for retirement.

We gave them instructions on what to tell the SS

office in order to start benefits. The office's

recommended strategy was faulty.

"After several email exchanges between our office

and the local SS office they conceded that we were

right and gave the clients benefits and past due

checks. They were thankful for the information and

said they would be educating their staff as well

as doing supplementary training.

"None of this would have been possible without help

from Elaine in giving them backup data for the recommendations.

We were even able to quote the POMS manual. It gave

us great instant credibility to start a seminar

off." — Michael Egan, Vienna, VA

A Service In High Demand

"We do a weekly radio show to talk about the workshop

and the response has been overwhelming. Last night

there were 90 people in attendance. 25 sheets came

in that night requesting a review and the sheets'

assets total over 9 million dollars." —Robert

Stanlick, Hillsborough, NJ

Know What You're Talking About, And You

Can Help A Lot Of People

"A true story from my own life: while still employed,

I took my 62 year old non-working wife to the Social

Security office to begin her benefit only to learn

that since she did not have her own 40 quarters

she would have to wait until I retired.

"Three years later I went to get my wife on Medicare

and was told (erroneously) that a) she had to wait

for me to retire and/or start my own Medicare and

b) she would have to be covered by a true group

health plan for two years while waiting, forcing

me to purchase a $1100 per month Blue Cross Group

to replace my $400+ per month individual health

plan." When the "error" was discovered, it was impossible

to make retroactive changes.

"Conclusion: know what you're talking about, and

you can help a lot of people." — Victor Gadoury,

Stilwell, KS

A Great Way To Arouse Interest In Prospective

Clients

"I have been impressed with the quality of material

from Horsesmouth. As a Financial Planner focusing

on the 50+ crowd, presenting Social Security information

effectively is important. This is a great way to

garner interest from potential clients." — Ora Citron,

Alamo, CA

$25,000 Paid Retroactively—Thanks! "I love the materials that you have put together

on Social Security. I recently had a visit

with my father and stepmother in Florida and we

talked about Social Security planning.

"After educating them on their rights, my stepmother

called the local Social Security office and told

them that her spousal benefit was incorrect. They

have subsequently received a check for over $25,000

for a retroactive correction of her spousal benefit.

Thanks." —Gwen Vogt, Basking Ridge, New Jersey.

Dry and Boring Made Very User Friendly—Clients

and Prospects Eager "First of all, thank you for your work and the resource

you have become for advisors in the arena of Social

Security. I purchased the Horsesmouth curriculum

several months ago and have been a student of it

since. I am planning to hold my first workshops

in September and already have clients and prospects

eager to attend.

"I also want you to know that I enjoy reading

your material because it is so well done and friendly!

I say friendly because this stuff is so dry and

boring and unattractive in and of itself (unless

one is an actuary), and you have made it very user

friendly. Thank you again."—Susan Tackett, Visalia,

CA.

A Much Needed Resource "I'm most appreciative of the material you've put

together on Social Security. You've created a much

needed resource."—Madeline Noveck, New York, NY.

Clients' Jaws Drop—Even Hardened Ones

Open Up "Once again Horsesmouth hits a grand-slam. This

webinar is MUST SEE…Elaine made it simple to understand

yet very informative and brought tons of new issues

to the table that before might have been overlooked.

"Probably most importantly though, is the information

in this seminar I've been able to take to my clients

and you can see their jaws drop when we get knee

deep into discussing SS. "Just like Horsesmouth

has said, there is NO better way to show off your

skills than by having an elaborate discussion about

Social Security. Even the most hardened clients,

who've heard all the pitches before from brokers,

planners, insurance people, bankers, et al. will

open up and that leads to business. Way to go Horsesmouth!

Thanks!" —Joshua G. Scandlen CFP®, CRPS®, San Antonio,

TX

Future Benefits Review Led to New Client "I have enjoyed the Social Security program and

calculators very much. Although I am still learning

and educating myself on the many rules, I attribute

a recent close of a new prospective client to reviewing

their future benefits of their PIA from your calculator

to the close. Thank you."—Walt Powrozek, Novi, MI

We'd Be Lost Without It—CPAs Appreciate

It, Too "We did another Lunch and Learn on Social Security

this past Friday—it was our third—and I have to

tell you that the feedback has just been great.

I can think of at least 4 couples who have expressed

an interest in developing a Social Security strategy

with us and one has already come in.

"The calculators are great and all the ideas

you give in the book—"File and Suspend", "Do Over"

etc… have gone a long way towards convincing the

groups we've worked with that Social Security is

a not a cookie cutter govt. program where no planning

is needed. So, again, I applaud you on giving

us such a great resource in the "Savvy Social Security

Planning" book. We'd be lost without such

a guide.

"I can also tell you that we've already had two

CPAs agree to host a meeting for their clients where

we get to do our Social Security presentation.

Because we're keeping these to about 12 people per

lunch, each CPA has indicated they'd likely be willing