Help Your Clients Make Smart and Responsible Decisions about Long-Term Care Planning

Start by Sending Them the Long-Term Care (LTC) Planning Options: Smart Approaches for People at All Stages

-

Available in PDF or print version

-

Branded with photo and logo

-

Finra-Reviewed

Yes, I want to order my branded Long-Term Care Planning Options: Smart Approaches for People at All Stages reference card.

Dear Advisor,

It can be very hard to manage clients' retirement if they do not have a solid plan for covering their late-in-life care. Many are vastly misinformed about their own vulnerabilities and risks and it's important for clients to understand that there could be big, unintentional impacts on their family and their estate plan. Which is why you are the best person to ensure they have some Long-Term Care (LTC) plan.

You can start educating your clients about the realities of preparing for long-term care by sharing with them your custom copy of Horsesmouth's new Long-Term Care Planning Options card.

The problem in a nutshell

As we emphasize in our client education program, Savvy Long-Term Care Planning, the problems advisors are overlooking with their clients is this: Many clients have avoided seriously planning for long-term care which can be both a serious risk to their financial security and a growing opportunity for your practice.

First step solution

Because many clients are avoiding planning for long-term care, we have designed the Long-Term Care (LTC) Planning Options Card as a handy resource that you can share with clients and prospects. Many clients do not know where to turn for useful and helpful information about the process of preparing and saving for long-term care.

Clients often don’t think they will need long-term care and then they are faced with expensive bills that were unplanned for. That’s where the Long-Term Care (LTC) Planning Options Card comes in, available for all advisors. Families will appreciate your thoughtfulness in providing advice along the bumpy road of figuring out how to plan for long-term care.

Clients, prospects, and COIs will love the Long-Term Care (LTC) Planning Options Card because it’s packed with information in a clear, easy-to-comprehend format. It lays out different ways to pay for long-term care and considerations to take in for each option. Topics addressed on the card include:

Long-Term Care Planning Options: Smart Approaches for People of All Stages

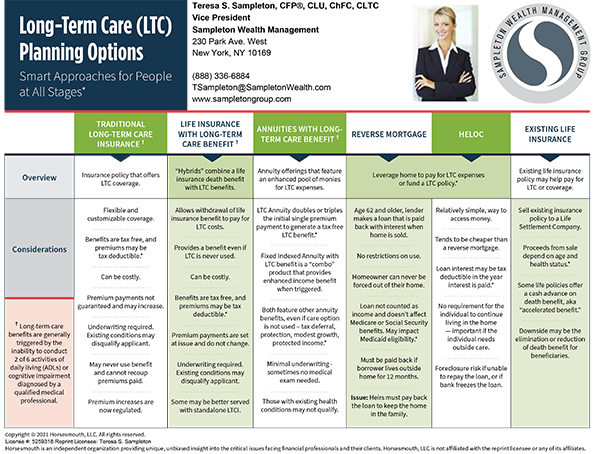

Traditional Long-Term Care Insurance

The first step is to make sure your clients are aware of what long-term care is and why it is necessary. It’s important for them to know that policies are flexible and have customizable coverage. There are many considerations that include the cost, flexibility, and benefits of long-term care. The policy will also help clients cover the cost of care in a person’s home or a facility due to a chronic medical or cognitive condition.

Life with Long-Term Care Benefit

These are also called “hybrids”. These hybrid policies combine a life insurance death benefit along with LTC benefits. If the LTC benefit goes unused, the death benefit will be available for the beneficiaries. However, it can be costly and if they have a chronic medical condition, they may benefit more with a standalone LTCI.

Annuities with Long-Term Care Benefit

There are two annuity categories that are worthy of reviewing with your clients – Long-Term Care Annuities and Fixed Indexed Annuities (FIAs) with LTC benefits. FIAs with LTC benefit is like a “combined” product that provides enhanced income benefit when triggered. Both feature other annuity benefits, even if care option is not used.

Reverse Mortgage or Home Equity Line of Credit (HELOC)

This is an option for individuals wishing to cover long-term care costs and can leverage their greatest asset, their home, to pay for LTC expenses or a LTCI policy.

-

Reverse Mortgage – For clients that are 62 years or older, the lender makes a loan in a lump sum, monthly installments, or as a line of credit for the homeowner. There is no restrictions on how the loan can be used and the homeowner can never be forced out of their home. This loan also is not counted as income and doesn’t affect Medicare or Social Security benefits, but it may affect Medicaid eligibility.

-

Home Equity Line of Credit (HELOC) – A HELOC can be a great alternative to a reverse mortgage and is a quick and easy way to access money for LTC or insurance. This option tends to be cheaper than a reverse mortgage and there is no requirement for the individual to continue living in the home – which can be crucially important if the individual needs outside care. However, there could be a foreclosure risk if unable to repay the loan or if the bank freezes it.

Existing Life Insurance

An existing life insurance policy can help fund a LTC plan in a few ways. Individuals may have traditional life insurance policies that could be sold to a Life Settlement Company – where proceeds will depend on the age and health status of the policy holder. Additionally, some life insurance policies offer “accelerated benefits” in the form of a cash advance against the death benefit. However, the downside may be the elimination or reduction of death benefit for beneficiaries.

Health Savings Accounts (HSAs)

An HSA can be a tax-advantage strategy for handling LTC expenses or paying LTC insurance premiums. Contributing to an HAS reduces annual taxable income and grow tax deferred until monies are used to cover eligible healthcare expenses. If your client is over the age of 65, then the money from an HSA may be used for anything without penalty. Additionally, HAS withdrawals for medical expenses and LTC insurance premiums may be tax free if they meet certain guidelines.

Self-Funding

This is an option for individuals that do not qualify for traditional long-term care insurance (LTCI) due to existing health issues. In a situation like this, the individual will have to use savings or investments to pay for care out of pocket and should set money aside for at least two to three years of LTC. Planning early is the key to success.

Medicaid

Medicaid will cover long-term care costs at home or in a skilled nursing facility. However, the biggest issue is that many people who need long-term care never qualify for assistance due to income thresholds and lookback periods.

Here for a Branded Sample of the Long-Term Care (LTC) Planning Options Card

Order Your Branded Long-Term Care (LTC) Planning Options Card for Just $297 and nd Get:

-

Instant, branded PDF – Share it right now.

-

Printed, branded cards – Mail/hand out all year.

How to Use the Long-Term Care (LTC) Planning Options Card with Clients

Whether you want to simply be an “information provider” or a full-blown “long-term care advisor” (a great niche), the Long-Term Care (LTC) Planning Options Card is an excellent resource to share with clients, prospects, and strategic allies. Here’s wat you could do with your custom version:

-

Send or hand out to all your clients.

-

Share on your website, allowing people to download a PDF copy.

-

Include the whole card with an e-newsletter or choose portions to share on a monthly basis.

-

Send copies to CPAs and other strategic allies who’ve got clients with questions about long-term care, too.

6 Reasons to Give Clients the Long-Term Care (LTC) Planning Options Card

-

Because you’re the trusted professional. People are looking for authoritative information about long-term care planning. This shows you know what you are talking about.

-

Because this differentiates you from competitors. Few financial advisors address long-term care planning. People are desperate for advice, but don’t know where to turn. You are demonstrating that you can handle their concerns.

-

Because each person’s case is different. This handout gives clients the basics to begin thinking about long-term care planning and funding but reinforces the idea that they need to come to you to thoroughly review their situations.

-

Because it’s a good “marketing touch.” Pop a copy of the card in the mail, along with a cover letter, to let your clients know you are thinking of them. They’ll be impressed with your thoughtfulness.

-

Because it’s a perfect handout. Share with clients and prospects at meetings, workshops, and other events where you need or want helpful material to share with others. They’ll pass it to friends, too.

-

Because it demonstrates your commitment to caring about your clients and the milestones in their lives. And when people know you’re committed to them and to your profession, it promotes loyalty and referrals.

So, go ahead and take your first, easy step to including Long-Term Care (LTC) Planning Options Card as part of your client communication program throughout the year.

*Additional custom personalization (including special characters, bolding, and additional text) is available for an additional fee. Call Member Support 888-336-6884 ext. 1 for further information.

The Long-Term Care (LTC) Planning Options Card fee will be charged directly to your credit card. Our online process is secure, and you can safely provide your credit card information in the form below.

About Horsesmouth

Since 1997, Horsesmouth has been helping financial professionals succeed by providing timely guidance on key topics such as business development, practice management, financial planning and investment strategies.

FOR INSTANT SERVICE Call Toll Free: (888) 336-6884 ext. 1 (Outside U.S.: 1-212-343-8760)