Social Security Helps You Capture More Assets from Retiring Boomers

Pre-retirees want professionals who can optimize Social Security benefits before they’ll even let you peek at the rest of their assets.

Savvy Social Security Planning is our industry’s only comprehensive suite that builds your expertise so you can educate and advise clients and prospects. You get:

-

Top-ranked software that produces custom client reports

-

Q/A Forum: Get answers from the experts

-

Six Finra-reviewed Social Security presentations

-

Marketing toolkit

-

Two comprehensive guides for learning Social Security

-

Twice monthly newsletter

-

Two client reference handouts

-

30+ client reprint articles

-

Social Security Audit Tool

-

12 CFP CE credits exam

A Tale of Two Financial Advisors: Don’t Be the Second One!

Dear Advisor:

Peter Murphy, a CFP® practicing in Santa Fe, NM, would like to apologize in advance for stealing your clients.

It’s not intentional. He’s very sorry for poaching, but your clients asked to open the account. What was he to do?

Take a case he closed shortly after deciding to make Social Security central to his marketing strategy.

It was his first meeting with a couple who attended one of his Social Security workshops. They came in for a free analysis plus a consult on their investment portfolio. They were managed by a professional Peter knows and respects.

Peter did a Social Security analysis for the couple and showed them their best options. He also reviewed the couple’s retirement portfolio and it looked fine. He’d recommend the very same investments, he told them. No changes.

The couple thanked Peter and asked to open an account. Peter was astounded. The couple’s professional was actually a good guy—Peter knew him! Why move?

He didn’t know much about Social Security and Medicare, they said. He had told them he didn’t know anything about Social Security and wouldn’t be able to offer any advice on that topic. They thought there was more to it than just signing up and Peter’s workshop confirmed it.

Peter signed a new $500,000 account in just one workshop and a meeting.

The other professional got the ACAT transfer form.

Social Security expertise attracts assets

As both Peter and the other professional discovered, Social Security is a critical issue for affluent boomers. It may be a tiny percentage of their overall funds, but it’s guaranteed income that can be optimized by professionals who know what they’re doing.

Professionals like Peter, who discovered he could better serve and protect his clients by learning everything he could about Social Security.

He’s now leveraged his new expertise into a state-wide education program that consistently brings in over 60 new AUM clients per year. He’s getting two to three referrals a week and averages about $1 million a month in AUM and another half million in additional fees per year.

Best of all, he acquired his in-demand skills quickly, he has expert support when client issues get messy and his virtual Social Security support team keeps him supplied with fresh, up-to-date presentations.

The key to Peter’s success was joining Horsesmouth's Savvy Social Security Planning program. It gave him the knowledge, tools, software, and resources to become the go-to Social Security expert in Santa Fe and throughout New Mexico.

Future Benefits Review Led to New Client

“I have enjoyed the Social Security program and software very much. Although I am still learning and educating myself on the many rules, I attribute a recent close of a new prospective client to reviewing their future benefits. Thank you.”

—Walt Powrozek, Novi, MI

Social Security is a game changer—here’s why

Peter was about to call it quits.

He had retired as a fighter pilot from the U.S. Navy, moved his family to Santa Fe, and set up shop as a financial professional specializing in retirement planning. He’d bought into a financial education franchise that promised him a roadmap for building a retirement business.

Only, the “proven” marketing strategy wasn’t working.

He ran the “can’t miss” ads in the newspaper. No response.

He gave his “standing room only” retirement seminars at the community center. Nobody came.

He made his “let me introduce myself” phone calls to business owners of a certain age. No interest.

After a year in business, Peter was washing out.

He wasn’t used to failure. He’d been a naval aviator for 27 years, rising through the ranks to Captain and ultimately working in the Pentagon for the Secretary of Defense.

Another Tool in Advising Clients on Income Planning

“A 60-year-old prospect came to the office because his 73-year-old wife had just been diagnosed with cancer. He wanted to retire so he could stay home with her. He wanted us to develop an income plan which included his savings, her Social Security, his company pension and what he could expect at ages 62, 66, and 70 from his Social Security. The analysis showed he could retire immediately, but wait until age 70 to maximize his Social Security and have enough income until then from annuitizing two of his annuities.

Knowledge of Social Security provides another tool in advising clients on income planning.”

—Darrill Beebe, Arlington, TX

He knew he needed three things to get his new business off the ground:

-

A pain point so intense it would bring new people into his office

-

A solution so compelling prospects would gratefully sign up

-

A marketing strategy so effective it would build his brand and keep his calendar full.

That’s when a friend – another professional – suggested Peter look at Horsesmouth’s Savvy Social Security Planning program. People have a lot of issues when it comes to their benefits, he said. They want and really need professional help.

That sounded too down-market for Peter. Yes, he got a lot of Social Security questions, but he was looking for bigger fish. He couldn’t make a living serving people who relied on Social Security.

You’re missing the big picture, the other professional said. Social Security wasn’t the end game, it was the opening conversation. It was the searing pain point Peter was looking for. Think about it…

-

96% of prospects qualify for some form of Social Security

-

Social Security is one of the "three legs" of the retirement stool, a source of guaranteed income

-

Everyone has a concern—even if they don't understand the system

-

Even wealthy people want their benefits, especially for the family

-

The Social Security conversation always leads to a bigger discussion of other assets

-

Social Security is an easy conversation to start

Peter latched on to that advice like a man overboard reaching for a life preserver.

Today, Peter is Santa Fe’s premier Social Security professional. He gives classes at the local community college and out of town at various University of New Mexico campuses. His workshops are so popular he’s had to limit attendance to 25 per session.

Killer follow-up

Best of all, he’s killing it on the follow-up. 80% of his attendees sign up for an initial consultation. 100% show up, eager to open an account. 50% become AUM clients with another 25% opting for hourly services.

He’s even opened a second office and hired a part-time professional.

How did Peter do it? He joined the Savvy Social Security Planning program. It was the secret sauce that juiced his retirement business and turned him into a successful professional, community builder and business owner.

Savvy Social Security Planning could do the same for you.

How to build a retirement business with Social Security

A Great Way To Arouse Interest In Prospective Clients

“I have been impressed with the quality of material from Horsesmouth. As a Financial Planner focusing on the 50+ crowd, presenting Social Security information effectively is important. This is a great way to garner interest from potential clients.”

—Ora Citron, Alamo, CA

The key to capturing more retirement assets is to lead with a strong Social Security approach that not only maximizes clients’ income but convinces them you are the only professional to manage the rest of their portfolio.

And boomers need help. Many have complicated situations due to divorce, death and blended families.

Think about how much money they leave on the table by making the wrong decisions:

-

Filing at the wrong time can cost clients tens of thousands of dollars over their lifetime, some of which may never be recovered.

-

Many elections are one-time only. The wrong decision can trap retirees for the rest of their lives with no do-overs.

-

People often lose guaranteed income by ignoring the earnings test, costing themselves and their family needed income later on.

-

Most Social Security recipients do not understand how taxes on their benefits are calculated.

-

Benefits may be smaller because Medicare actually shrinks their Social Security check.

-

Bad decisions can cost surviving spouses and dependents needed income at a time when they are most vulnerable.

-

Divorcees don’t understand how a previous marriage may boost their benefit.

When Peter was first exploring his options, he talked to everyone he knew about their Social Security needs. Everyone had a question… a complaint… a horror story.

He talked to CPAs and attorneys. They didn’t know much about it even though they were fielding questions daily. If he found someone, could he pass along their name?

Peter saw an opportunity. A big opportunity. He just needed some technical knowledge, a value proposition and a solution he could market.

It Was A Great Idea

“I explained to a couple that she could take half of her husband’s SS for several years, postponing her SS benefit and letting it increase in value 8% per year.

They didn’t know they could do this and thought it was a great idea.”

—Lisa Winward, Salt Lake City, UT

The Savvy Social Security Planning program was the game-changer he needed. Within six months, Peter was:

-

Giving Social Security presentations in workshops across New Mexico

-

Booking appointments by offering attendees a free Social Security Audit

-

Giving away multiple Break-Even and Maximization Analysis Reports

-

Offering married couples a Coordinated Spousal Planning Report

-

Helping pre-retirees understand how the earning test impacts benefits

-

Charting how COLA would affect people’s lifetime benefits

-

Delivering Personalized Retirement Spending Forecasts to very impressed prospects

The market went wild!

His workshops filled up. His appointment book was brimming. He was finally getting in front of prospects who had the assets to hire him.

Peter had found his calling in the Savvy Social Security Planning program.

How Savvy Social Security Planning works for you

There are four key areas to focus on in building a Social Security specialty. The Savvy Social Security Planning program steps you through each with field-tested training, materials, and expertise.

1– Master the Savvy Social Security Planning material

175+ page handbook

To help you gain technical knowledge quickly, Savvy Social Security Planning provides you with proven training and reference materials that get you up to speed in a hurry. You get:

-

The Financial Advisor’s Guide to Savvy Social Security Planning, a 175+ page handbook that walks you through all major aspects of Social Security planning. This became Peter’s bible, giving him the techniques and insights he needed to talk about Social Security with confidence. Just consider what’s covered in 12 chapters:

-

What Financial Professionals Need to Know About Social Security

-

The Role of Social Security in a Client’s Overall Retirement Plan

-

How Social Security Works

-

Boosting Benefits by Increasing Current Earnings

-

When to Apply: Strategies for Maximizing Lifetime Benefits

-

Coordinating Spousal Benefits

-

Women and Social Security

-

Taxes on Social Security Benefits

-

Other Social Security Programs

-

Medicare and Long-Term Care

-

Mechanics of the Social Security Program

-

History and Financing of the Social Security System

135 Questions—

Answered

-

135 Social Security Questions Answered: What Savvy Advisors Need to Know: Every day Elaine Floyd, CFP® spends time researching and answering tricky, perplexing, contradictory, and generally vexing Social Security questions. Here are the key ones you need to understand.

Elaine Floyd

-

Elaine Floyd, CFP®, the industry’s leading Social Security expert is your personal trainer. Elaine wrote the books (literally) on Social Security and Medicare for professionals. She has been quoted in the Wall Street Journal, The New York Times, U.S. News & World Report, Kiplinger’s Retirement Report, Robert Powell’s Retirement Weekly, and is a popular speaker at FPA, FPA NorCal and the AICPA.

Over 20k Q&A

-

The Savvy Social Security Planning Question & Answer Forum. This is the largest collection of Social Security questions you’ll find anywhere in the industry. It consists of more than 20,000 professional real-time questions and field-proven answers. We’re not talking a book here. We’re talking a forum or a database that grows every day as professionals ask new questions and our experts provide new answers.

2– Optimize client benefits and highlight your brand

As Peter discovered, it’s not enough to know all the Social Security rules. You need to turn that expertise into tangible deliverables that clients will value and act on.

The Savvy Social Security Planning Software is a powerful tool designed to help financial advisors analyze and optimize Social Security claiming strategies for their clients. Key features and benefits include:

1. Comprehensive Analysis:

Software

-

Evaluates retirement benefits, auxiliary benefits (spousal, divorced-spouse, survivor), and dependent benefits

-

Accounts for early claiming reductions and delayed retirement credits

-

Incorporates annual cost-of-living adjustments (COLAs)

2. Customizable Scenarios:

-

Offers suggested scenarios based on client situations

-

Allows creation of custom scenarios for unique client needs

-

Compares multiple scenarios to identify optimal claiming strategies

3. Flexible Client Profiles:

-

Supports various marital statuses: married, single, widowed, and divorced

-

Handles complex situations like government pensions (WEP/GPO) and disability benefits

4. Clear Visualization:

-

Generates graphs showing cumulative benefits under different scenarios

-

Illustrates first-year income for surviving spouses

5. Professional Reporting:

-

Creates customized PDF reports for client presentations

-

Highlights the financial impact of different claiming strategies

6. Value Proposition:

-

Demonstrates potential increase in lifetime benefits (often tens or hundreds of thousands of dollars)

-

Helps clients make informed decisions about when to claim Social Security

7. Marketing and Client Acquisition:

-

Positions you as Social Security experts

-

Provides a compelling reason to engage with prospects before they reach claiming age

With the Savvy Social Security Planning software, you’ll be equipped to help your clients maximize their retirement benefits and secure their financial future. This powerful, integrated program analyzes a wide range of claiming scenarios, including those for married couples, widows, divorced individuals, families with children, and single people.

By incorporating this software into your practice, you'll simplify the complexities of Social Security for your clients and showcase the immense value you bring to their retirement planning journey.

Expert Support

Becoming the expert and staying one takes support. Especially for professionals like Peter, a solo practitioner with just one full-time staffer.

As Peter soon discovered, he needed:

-

Expert guidance when cases got messy and he had questions

-

A way to stay on top of the rule changes that could start his phone ringing from worried clients

-

Alerts and analyses explaining new case law, strategies, and techniques working for other professionals

-

A simple process for managing meetings, handling paperwork and moving prospects toward signing.

Peter found it all in the Savvy Social Security Planning program. As a member, he learned firsthand what’s working for other professionals. He knew about rule changes almost before they were announced. He could alert clients to new developments and intelligently discuss their ramifications.

Peter became the primary source of Social Security news and information for a wide range of prospects, clients, and strategic allies. And he maintains his expertise through:

-

Savvy Social Security Planning’s twice-monthly newsletter covering the latest news, strategies, updates, and tools, written by Elaine Floyd

-

Breaking News legislative updates issued as rules change and developments arise

-

A twice-weekly blog covering new studies, trends, and events

-

Live webinars to review new developments

-

Live two-day Social Security trainings for professionals at selected locations across the country (additional)

-

Group coaching with other professionals pursuing Social Security (additional)

Within six months, Peter’s calendar was so full, he started charging for the free consultations, adding another new revenue stream that keeps his phone ringing and diversifies his income.

4- Promote your Social Security expertise

Peter didn’t have time to develop his own presentation.

But he liked to present. He came from a long line of teachers, and holding workshops seemed very natural to him. But he needed educational materials he could use online, in workshops, and in face-to-face meetings.

Savvy Social Security Planning has a vault of educational content. So much, in fact, Peter turned his office into a Social Security education center, open to anyone needing information on claiming strategies, spousal benefits, survivor benefits, and more.

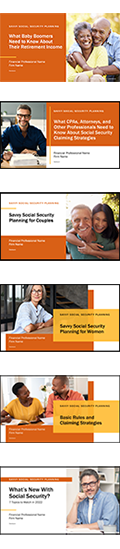

6 Presentations

The rest of his marketing kit is equally impressive. Peter can choose between six different PowerPoint presentations – with scripts – so he always has a fresh FINRA-Reviewed presentation for almost any audience (couples, women, CPAs, etc.).

He also has a library of FINRA-approved handouts and marketing materials he can customize and brand.

As Peter discovered, the Savvy Social Security Planning program acts as his virtual marketing support, producing a wide variety of FINRA-reviewed client-facing materials, as well as new and updated presentations every year or as rules change.

Take a look at Peter’s Social Security marketing resources:

-

6 FINRA-reviewed client presentations (PPT slides & scripts)

-

Social Security Planning: What Baby Boomers Need to Know About Their Retirement Income (65+ slides, 22-pg script)

-

Social Security Planning for CPAs, Attorneys and Other Professionals (45+ slides, 16-page script, plus you can award one CPE credit to all attending CPAs)

-

Social Security Planning for Couples (60+ slides, 18-page script)

-

Social Security Planning for Women (55+ slides, 19-page script)

-

Social Security Planning: Basic Rules and Claiming Strategies (40+ slides, 15-page script)

-

What’s New with Social Security: 8 Topics to Watch in 2026 (40+ slides, 12-page script).

-

Client-facing materials (FINRA reviewed)

Client Material

-

Social Security Client Presentation Notes (handout)

-

90-second embeddable video, easy to customize to promote workshops & events

-

Baby Boomer’s Guide to Social Security, a 4-panel, 2-sided, 8.5" x 11", brochure (50 hardcopies included with your membership)

-

Social Security Quick Reference Guide (handout)

-

Social Security educational articles (30+ reprints you can brand with your contact info and pictures)

-

Pre-written workshop descriptions

-

Customizable workshop posters and postcards

-

Invitations & confirmations

-

Press release template

Changed My Clients’ Lives

“A client who had been married twice was unaware that she could receive spousal benefits on her first husband. This knowledge helped her plan a better retirement since her SS benefits were less than half of his.

Another divorcee who was dating someone with a small SS benefit did not realize that she could file for a spousal benefit on her ex if she remained unmarried.

The information I was able to provide ended up changing their lives.”

—Timothy C. Ebert, Winston-Salem, NC

Peter’s business is booming! Thank you, Social Security.

Peter no longer thinks about quitting. Now he dreams about growing. And why shouldn’t he? He’s firing on all cylinders as his Social Security strategy takes off.

This year, he’s teaching 10 Social Security classes, holding two every semester at the local community college. Nearly every attendee comes in for a consultation, he says. His minimum for opening accounts is now $500,000, Social Security analysis included.

For non-AUM clients, he charges $500 for the initial analysis and $250 per hour. He’s also added a new line where he helps people sign up for Social Security for a flat $95 fee. He’s training his assistant to provide that service.

“In the past I did a lot of those analyses for free,” says Peter. “Now I get paid. That was one of the biggest changes I’ve made. It’s made a big difference in my income.”

As Peter will tell you, he owes it all to the Savvy Social Security Planning program.

“The advising business continues to get more competitive, and AUMs are being driven down to a lower percentage based on robos and other competitors out there. That’s why I believe professionals need to get involved in Social Security.

“People need the help, and professionals understand the process. You’ll bring in thousands more dollars a year for performing that service, and if you don’t want to do it, then you can teach someone in your office to do that. It’s not that hard. You can learn all you need to know from the Savvy Social Security Planning program. It’s just such a simple strategy,” says Peter.

5 reasons to master Social Security today!

25,000 Paid Retroactively—Thanks!

“I love the materials that you have put together on Social Security. I recently had a visit with my father and stepmother in Florida and we talked about Social Security planning.

After educating them on their rights, my stepmother called the local Social Security office and told them that her spousal benefit was incorrect. They have subsequently received a check for over $25,000 for a retroactive correction of her spousal benefit. Thanks.”

—Gwen Vogt, Basking Ridge, NJ

-

Boomers think you know Social Security already. Why wouldn’t you? It’s part of their asset mix… it’s guaranteed income... you’re the money guy. Boomers will use your expertise (or lack of it) to decide whether you’re competent to manage the rest of their assets.

-

Money is in motion as boomers start retiring. The Great Boomer Retirement Wave is underway with 36+ million MORE pre-retirees ready to file for Social Security. That pipeline should stay full until at least 2028, maybe longer as boomers continue to work.

-

Social Security is not a side hustle – it’s the main hustle. Social Security is too complicated not to give it your full attention and still avoid mistakes. Plus, it’s your door opener to the larger retirement conversation. Social Security can be your marketing strategy, your specialty niche and an entire service line, as Peter discovered.

-

You can’t learn Social Security just from a software program, but the Savvy Social Security Planning software actually teaches you when you make errors. It’s not enough just to give boomers a printout of their bend points. They need context, expert analysis, and personal insights to make sense of their decisions. You need to truly understand the ins and outs of Social Security to build your brand as an expert.

-

Your Social Security expertise can open doors to professional referrals. You’re not the only financial professional hit hard with Social Security questions. CPAs and attorneys hear them, too, but they usually don’t have the answers clients need.

You can become their referral partner with Social Security. The Savvy Social Security Planning program even has an exclusive one-hour workshop specifically for CPAs and attorneys where you can demonstrate your expertise, instead of pitching it.

Best of all, you can award any CPAs who attend your workshop one continuing education credit (CPE). That credit not only fills seats, it practically assures you’ll see more referrals from your professional partners.

Invaluable Training

“I have found that a good percentage of clients plan to take SS early as possible.

This comes without any awareness or thought given to some of the consequences and effects on beneficiaries that may have.

My training has helped me assess my clients’ overall financial and family situation and advise them if taking SS early is the best way to go. Consequently, I have changed some of my clients’ plans to take SS early as a result. In many cases this has a significant effect on their financial status.”

— Alfred Kulig, Kettering, OH

As a member, you get everything you need to master the material, produce deliverables, tap into expert support, and build a marketing program that will keep the Peter Murphys of the world from snatching your clients and prospects.

Client Material

All the materials are field-tested, FINRA-reviewed, and updated annually or as regulations change. They are yours for as long as you maintain your Savvy Social Security Planning license.

Your Savvy Social Security Planning for Boomers program includes:

Technical resources:

175+ page

handbook

-

Elaine Floyd, CFP®, the industry’s leading expert who wrote the book on Social Security and how to advise clients.

135 Questions

Answered

-

The Financial Advisor’s Guide to Savvy Social Security Planning, a 175+ page handbook that walks you through all major aspects of Social Security planning.

-

135 Social Security Questions Answered: What Savvy Advisors Need to Know: Every day Elaine Floyd, CFP® spends time researching and answering tricky, perplexing, contradictory, and generally vexing Social Security questions. Here are the key ones you need to understand.

-

The Savvy Social Security Planning Question & Answer Forum. 20,000 professional questions and expert-supplied solutions.

Over 20k Q&A

12 CE Credits

-

Earn CFP® Continuing Education Credits. Earn 12 CE credits once you take and pass the 120-question exam

Solutions & deliverables:

Software

-

Savvy Social Security Planning Software

Audit Tool

-

Social Security Audit Tool

-

Customs reports and analyses

-

Social Security Maximization Analysis

-

Customized Break-Even Analysis

-

Coordinated Spousal Planning Report

-

Custom Survivor Report

-

Custom WEP/GPO Report

-

Custom Divorce Report

Twice-Monthly

Newsletter

Expert support resources:

-

Elaine Floyd’s twice-monthly newsletter covering the latest news, strategies, updates, and tools

-

Breaking News legislative updates issued as rules change and developments arise

-

A twice-weekly blog covering new studies, trends, and events

-

Ongoing live webinars with Elaine Floyd as events warrant

Marketing materials:

6 Presentations

-

6 FINRA-reviewed client presentations (PPT slides & scripts)

-

Social Security Planning: What Baby Boomers Need to Know About Their Retirement Income (65+slides, 22-pg script)

-

Social Security Planning for CPAs, Attorneys and Other Professionals (45+ slides, 16-page script, plus you can award one CPE credit to all attending CPAs)

-

Social Security Planning for Couples (60+ slides, 18-page script)

-

Social Security Planning for Women (55+ slides, 19-page script)

Article Reprints

-

Social Security Planning: Basic Rules and Claiming Strategies (40+ slides, 15-page script)

-

What’s New with Social Security: 8 Topics to Watch in 2026 (40+ slides, 12-page script)

12 Month License

-

Client-facing materials (FINRA reviewed)

-

Social Security Client Presentation Notes (handout)

-

90-second embeddable video, easy to customize to promote workshops & events

-

Social Security Audit Tool (checklist)

-

Baby Boomer’s Guide to Social Security, a 4-panel, 2-sided, 8.5" x 11", brochure (50 hard copies included with your membership)

-

Social Security Quick Reference Guide (handout)

-

Social Security educational articles (over 30+ different reprints you can brand with your contact info and pictures)

-

Pre-written workshop descriptions

-

Customizable workshop posters and postcards

-

Invitations & confirmations

-

Press release template

-

Annual license – Your 12-month license entitles you to full access to the Savvy Social Security Planning material.

5 myths stopping professionals—and why they’re way wrong!

Some professionals don’t believe in the power of Social Security to build a business. They’ve bought into these myths that are keeping them out of the action:

Myth #1: I’m too late to the game! The guys across town have been doing this for a while and they’ve scooped up all the assets.

The Great Boomer Retirement Wave is just getting started! 36 million pre-retirees are now age 62-70 and ready to claim Social Security – whether they should or not. (And there’s still more behind them!)

Know What You’re Talking About, And You Can Help A Lot Of People

“A true story from my own life: while still employed, I took my 62 year old non-working wife to the Social Security office to begin her benefit only to learn that since she did not have her own 40 quarters she would have to wait until I retired.

Three years later I went to get my wife on Medicare and was told (erroneously) that a) she had to wait for me to retire and/or start my own Medicare and b) she would have to be covered by a true group health plan for two years while waiting, forcing me to purchase a $1100 per month Blue Cross Group to replace my $400+ per month individual health plan. When the ‘error’ was discovered, it was impossible to make retroactive changes.

Conclusion: know what you’re talking about, and you can help a lot of people.”

—Victor Gadoury, Stilwell, KS

That pipeline is going to stay packed for the next 10-20 years and demand for Social Security skills will only get more intense as boomers age and rules change. There’s plenty of business for you and the guys across town – although who says they’re doing it right?

The guys across town keep doing Social Security workshops because they work.

And remember, just because 1% or so respond to a Social Security marketing mailer doesn’t mean the other 99% aren’t interested. They just can’t make your workshop dates. But they’re still desperate for the guidance.

Myth #2: I don’t do presentations, so I don’t need a Social Security program.

No problem! Not everybody has to be like Peter. You can launch a very effective e-mail, direct mail, phone, or online marketing campaign with all the marketing resources available in the Savvy Social Security Planning program. For example:

-

Need leads? Mail the “Boomer’s Guide to Social Security.” It’s a 4-panel, 2-sided, 8.5" x 11", brochure you could send to your current list of clients and prospects. It prompts people to call you and talk about their Social Security concerns. You’ll pick off the low-hanging fruit.

-

Send out a series of 6-8 educational articles (you get 26), branded with your name and contact information. You’re educating prospects, sharing your expertise, and again, triggering people with Social Security issues, to call you.

-

Use one of the PowerPoint presentations in a one-to-one meeting with a prospect. It’s a great way to step them through your process and everyone loves to have a custom talk just for them.

-

Offer the “What’s New with Social Security” PowerPoint on your website. Set it up as a lead magnet where people have to give you their name and email before they can get the material. You’ll build your prospect list without ever stepping on stage.

Myth #3: Social Security information is everywhere online! They don’t need me.

Do you know how many rules there are for Social Security? Upwards of 2,700! Half the time Social Security employees give out wrong information that can cost your clients guaranteed income. With no do-overs!

And clients are often their own worst enemy. They file too early and lose money. They don’t consider how their claiming strategy might affect their spouse or the children. They pay more in taxes and health care than they need to.

Plus, if everybody “knows” Social Security, why are CPAs and attorneys referring their clients to Social Security professionals? Because every client's situation is unique and it takes an expert to determine what applies, what doesn’t, and how to work around the problems to get the results clients want.

Social Security is complicated and clients need professional help. Do they get it from you or someone else?

The Best Story Is My Own

“Probably the best story is my own. Until going through your program, I was pretty much convinced that I would take SS benefits this year, but after going through scenarios based on my and my wife’s (who is 6 years younger) benefits it became clear to me that waiting as long as possible is the wisest move.

Our combined SS income could reach over 80K a year. And her survivor benefit increases more than 50%.”

—John Tarr, Madison, MS

Myth #4: People who care about Social Security don’t have any money.

Yeah, that’s what Peter thought until he discovered that Social Security opens the door to the larger conversation about ALL of the client’s retirement assets.

For affluent boomers, Social Security is like a free trial – of professionals! They use it as a way to try you out and see if you can solve their “little” problem before they’ll let you tackle their bigger issues.

And boomers have issues. Often divorced, with multiple families, today’s pre-retirees have a large number of Social Security problems that only an expert could solve.

That expert could be you! Or it could be the guy across town who IS getting in front of all those “millionaires next door” who want the guaranteed income they’ve been promised for the last 40 years.

As you well know, wealthy people, in particular, like to see returns on their investments, and that includes Social Security. Don’t you want to show them how to make smart, profitable decisions about Social Security?

Myth #5: I have no time!

Producing a retirement plan without Social Security is like building a two-legged stool. The wrong claiming strategy could affect how much retirees pay in taxes and in health care. If they pay too much, they’ll have no choice but to draw down the other assets you’re managing.

That’s why the Savvy Social Security Planning program moves fast, covering only those issues that are relevant to professionals and their clients. You’ll get field-tested techniques and processes that streamline your analyses and your time.

Plus, we have the solution to almost any Social Security problem you can think of. We have a database of 20,000 professional questions – and answers – to get to the root of most problems quickly.

And if you’re really, truly at full capacity, let one of your staff or a junior professional manage your Social Security service. It’s great training ground for young staffers and you’ll reap all the benefits of adding an additional business line and revenues!

Our gift to you: Order today and receive The Happy Advisor

Hardcover—228pp

How Do You Build a Prosperous Business, Raise a Family, Support a Spouse, and Contribute to Your Community—All While Leading Your Clients Safely Into the Future?

It’s a sad truth that few in this world really understand how difficult your job is and how rewarding it can be when pursued with passion, drive, determination, intensity, devotion, and dedication.

Thankfully, one of our own totally understands you and your profession. His name is Bill Smith, CFP®, a 30-year veteran professional from San Francisco and a long-time Horsesmouth columnist.

Leadership can feel lonely. But rest assured that you’re not alone. And the world has successfully made its way through periods this difficult in the past. The Land of Milk and Honey is just over the horizon.

Bill Smith’s uncommon wisdom can provide the perspective you need to survive and thrive.

During more than 35 years as a successful professional, Bill has analyzed every challenge and obstacle one could possibly face in the pursuit of a successful business.

And he’s come up with fresh approaches for overcoming each one.

Thank You for a Wonderful New Marketing Program

“Your Savvy Social Security Planning program has been wonderful and I hope to become proficient enough with the material to be considered an expert myself one day. Nowadays, I read everything and anything that concerns Social Security. I have hosted two Social Security presentations for my clients so far and I am considering holding public seminars later this year. I am sure this will lead to new clients for me. Thank you for a wonderful new marketing program.”

—Sally Ng, Walnut Creek, CA

Join Savvy Social Security Planning today for $697

Join today and get all the technical materials, the 6 presentations, all the marketing content, and Elaine Floyd’s expert support for only $697 (plus shipping) (a $6,000+ value).

You’ll recoup the costs of the program quickly – maybe even in the first few months—if you follow Peter’s game plan.

And if you’re still undecided, think about how much it costs you if you DON’T advise clients on Social Security.

-

Your marketing is much, much harder as you solicit new business with the standard pitch. How many prospects do you close talking “sequence of returns” or buckets? Social Security is a much easier conversation.

-

Your clients will make irrecoverable mistakes that not only cost them future income but could draw down the other assets you’re managing.

-

You’re always scrambling for an effective marketing hook and materials. Peter can pick and choose from a library of field-tested marketing content. You’ll have deal with compliance on your own.

-

You’ll be blindsided by new developments. Do you have the time and the team to continually monitor the Social Security Administration, Congress and the IRS to stay current? Google alerts won’t cut it.

And the biggest cost of all: You leave your clients vulnerable. You’re leaving them exposed to bad decisions… a substandard retirement… and to Peter and his workshops.

Social Security may not amount to much as far as total net worth, but clients often see it as a debt they’re owed. And that’s where Peter finds his “in” – which could be your “out” – if you’re not helping clients maximize their benefits.

The Savvy Social Security Planning program is a small investment that pays off big in upgrading your skills and building your brand.

Best of all, that small investment is backed by a powerful promise…

100% Risk-Free Protection

Peter’s success is no one-hit wonder. The Savvy Social Security Planning program produces subject matter experts for professionals who are willing to put in a just a little bit of time.

But you don’t have to take our word for it. Discover the power of Social Security for yourself. Learn the program. Present your new expertise to clients and prospects. Host a client education workshop. Help people for 12 months.

If you don’t see relief on a young widow’s face when she discovers she’s eligible for survivor benefits… or the smile you’ll get when you find a $25,000 benefit error… or the sheer joy of a new retiree who learns he’s set for life...

We’ll give you your money back. 100% of the purchase price refunded back to you. Just call us and tell us you’re returning the materials at: Horsesmouth, 230 Park Avenue, 3rd Floor West, New York, NY 10169. Phone: 212-343-8760, Ext. 1.

Protect yourself from Peter!

Able To Make A Difference

“I have helped several widows who have lost their husbands at a relatively young age, and had either forgotten or simply did not know they could be eligible for the spousal benefits.

This has occurred multiple times.

It is disheartening to realize how many struggling beneficiaries are unaware of their options. In this case, thanks to Elaine’s program, I was able to make a difference.”

— Philip Rongo, Lebanon, NJ

Peter’s a good guy. He really is. He doesn’t want to steal your clients. That’s why he’s letting us tell his story.

But you need to act soon. Because, if your clients happen to pop into one of Peter’s workshops and take a meeting to review their benefits, Peter is going to walk them through some Maximization Analysis and give them a Coordinated Spousal Benefits report.

And it’s a fair bet they’ll discuss some of the other assets you are managing to determine how they can be optimized in accordance with Peter’s claiming strategy.

Don’t be surprised if your clients come back with changes they want made to their retirement plan.

In fact, be happy your clients come back at all. Usually, after one of Peter’s meetings, all the other professional sees is a very cold ACAT.

Why lose the business? You’ve got 10-20 years of opportunity ahead if you can talk to retiring boomers about Social Security. And you still have time – the wave is only starting to build. But it IS underway.

Become the Social Security professional your prospects want. Once you can answer their questions and give them a game plan, you’ll rarely worry about ACATs again! You’ll be well on your way to building a successful retirement business that will last until you retire.

A Pleasant Surprise

“I had a prospect who couldn’t make it to any of my seminars call me with a question. He said he was 66 years old, his wife was 78 and collecting Social Security. He was still working and wanted to know if he could delay his SS benefits until he stopped.

I informed him that he could continue to work, file for a spousal benefit now, and let his own benefit accrue 8% credits until age 70, when he could switch to this higher benefit.

He was pleasantly surprised and grateful for the repreve. Without Savvy Social Security Planning, I would not have been as well-versed in that prospect’s financial planning options.”

— Carl Janasiewicz, Kingston, NY

P.S. Last chance to capture boomer retirement assets

The retirement market is hot! Money is in motion. Labor force participation is shrinking. The Great Boomer Retirement Wave is underway, offering professionals a once-in-a-lifetime opportunity to build a retirement business that can last for the next 10-20 years.

Ride the wave and save your place on the professional ship of good fortune! Join Savvy Social Security Planning and get all the tools, marketing materials, expert support and resources you need to build a thriving retirement business.

Request a Desktop Demo for Savvy Social Security Planning:

Demo includes:

-

Software

-

Client workshop presentation and speaker notes

-

Financial Advisor’s Guide to Savvy Social Security Planning

-

135 Questions Answered

-

Marketing Toolkit

-

Article Reprints

-

Client Handouts

-

Newsletters

-

Savvy Social Security Planning subscriber website

Click here to sign up or call (888) 336-6884 ext. 1

About Horsesmouth

Since 1997, Horsesmouth has been helping financial professionals succeed by providing timely guidance on key topics such as business development, practice management, financial planning and investment strategies.

Best,

Sean M. Bailey

Editor in Chief

Horsesmouth

230 Park Avenue, 3rd Floor West

New York, NY, 10169

(888) 336-6884 ext.1

P.S. Guess what? We’ve still got a solid eight years of Boomers claiming Social Security. But the leading edge Gen Xers are starting to turn 55 and they’re interested in Social Security, too. So make joining Savvy Social Security Planning part of your long-term business development strategy. Join here!

FOR INSTANT SERVICE Call Toll Free: 1-888-336-6884 ext 1 (Outside U.S.: 1-212-343-8760)